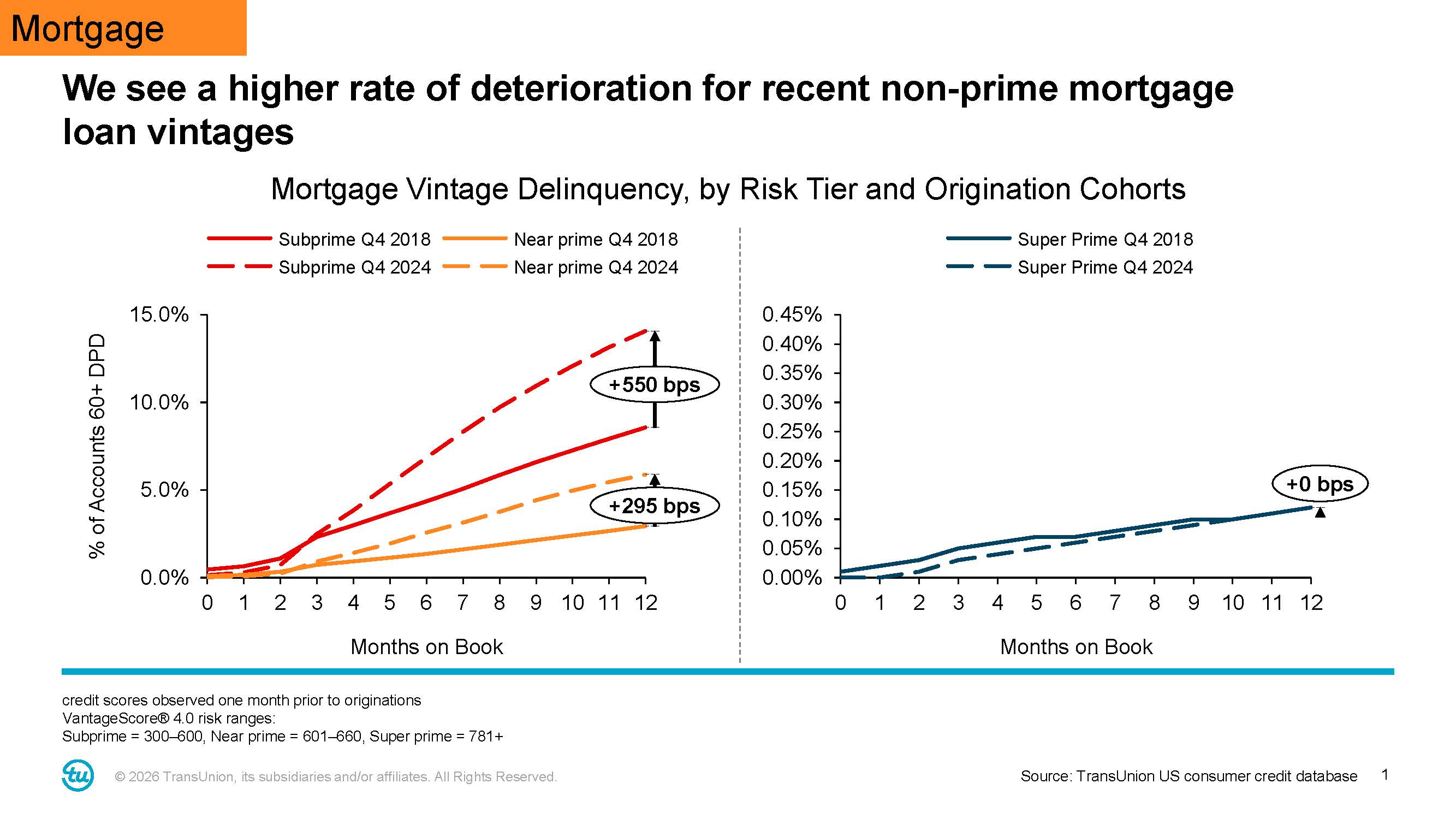

Recent subprime mortgages are deteriorating faster than pre-pandemic loans

A trend that has been discussed in the US economy is starting to show up in the credit market, and it involves high- and low-credit-score borrowers.

The term “K-shaped” economy has been used to reflect that high-income people are increasingly doing well while low-income people are doing worse, as the two demographics pull apart in a K-shape.

According to new data from TransUnion, this trend is showing up in recent credit reporting, with the highest and lowest credit score groups showing increases over the last three years.

Super prime borrowers, or those with credit scores above 781, and subprime borrowers with credit scores from 300 to 600, are the only two groups that have increased over the last three years.

More troubling for the mortgage industry is that borrowers in the subprime group are taking out mortgages that are performing worse than pre-pandemic and worse than any other credit score group.

Subprime mortgages taken out in Q4 2024, the most recent cohort, are more delinquent than those taken out in Q4 2018. In fact, the delinquency rate is 5.5% higher on those newer mortgages.

Super prime mortgages are not seeing the same deterioration. In fact, the mortgages taken out in Q4 2024 are at the same delinquency rate as the ones taken out in 2018.

Michele Raneri (pictured top), vice president and head of US research and consulting at TransUnion, said it is interesting to see how these more recent loans are generally performing worse, except among borrowers with the highest credit scores.

“We have this pre-pandemic time period to the current time period for subprime and near-prime,” Raneri told Mortgage Professional America. “The vintages are deteriorating for the current time period compared to 2018. So it means that now those are not performing as well. Delinquencies are higher. But for super prime in mortgage, it’s the only one where there wasn’t any deterioration in the vintage.”

Why subprime mortgages are struggling

To break down why the mortgages for the subprime borrowers are more delinquent, Raneri said it’s important to consider what those loans look like.

“They’re probably first-time homebuyers who are getting FHA loans,” she said. “So they’re getting loans that have programs that help people to get into the home with lower down payments. But within FHA loans, we’ve also seen that there are FHA loans that are prime and above, where they’re still getting that aid to be able to get into the home in the form of not having as high a down payment. But those are performing well.”

She said that because rates were higher when this most recent vintage of borrowers took out these loans, that factor is likely contributing to the increased delinquencies.

“I think that that’s part of the split is who’s actually getting a mortgage during this last year,” Raneri said. “Because the interest rates have been high. It’s less likely to be refinance customers until this last quarter anyway. It’s less likely to be a refinance, and it’s less likely that it’s going to be somebody who’s moving.

“It’s just people who have a real need to move or first-time homebuyers who are trying to get into the market, hoping that their home appreciation outpaces the interest rate that they had to get.”

Credit still available for subprime borrowers

Despite the increased delinquencies at the lower credit level, one encouraging sign to take away from this report is that there is still credit available for subprime borrowers.

“I think the surprising, shocking top line is that people who are subprime are still getting credit,” Raneri said. “So there is access to credit for people who are in the lowest tiers of the credit score, but they’re being kind of managed by lenders by not lending out too much. So there’s still access to credit even at the lower tiers. And risk is being mitigated both for the lender and for the consumer by moderating how much credit they get.”

This provides hope for potential first-time homebuyers that some credit issues in the past might not keep them from getting approval for a mortgage. Raneri said that overall that it was a good sign that credit was still flowing for subprime borrowers.

“We’re seeing this group expand, we’re seeing it take up more of their income, but they’re still able to get access to credit,” she said. “So they’re able to get that access to credit, which means that if they’re trying to rebuild their score, if they’ve had a hard time and they have had to charge off some credit cards, they’re finding that access to credit, which is different than previous times. I feel like it’s a positive that credit is still flowing at the bottom end.”

Stay updated with the freshest mortgage news. Get exclusive interviews, breaking news, and industry events in your inbox, and always be the first to know by subscribing to our FREE daily newsletter.