Use our home affordability calculator to show your clients the best home options for their budget. Give it a shot and build more trust with property buyers

- Free home affordability calculator

- What is a home affordability calculator?

- Why mortgage brokers should offer a home affordability calculator

- Working better with a home affordability calculator

- Mistakes to avoid when using a home affordability calculator

- How to calculate home affordability

- Help clients beyond using a home affordability calculator

As a mortgage broker, one of the most common questions that pop up from homebuyers is how much they can afford. That's where a home affordability calculator becomes your best ally. With a reliable calculator, you can set realistic expectations and avoid misunderstandings later.

In this article, Mortgage Professional America will explore all you need to know about using a home affordability calculator. We will talk about how to calculate affordability based on your clients’ monthly expenses and strategies to lower their mortgage payments.

Free home affordability calculator

To help make it easier for you to calculate your clients’ home affordability, you can use this free home affordability calculator:

Home Affordability Calculator

This calculator will determine your clients' home affordability. It will also show which expenses they need to keep in mind when budgeting their mortgage payments. The faster you help your clients understand their buying power, the quicker they can make their choices—and the easier you can close deals.

What is a home affordability calculator?

It's a tool that can estimate how much your clients can realistically afford based on factors like:

- income

- debts

- down payment

- other expenses

This calculator can give a price range by looking at what a monthly mortgage payment would be for their situation. It helps your clients see what fits their budget before they start shopping for homes.

How it works

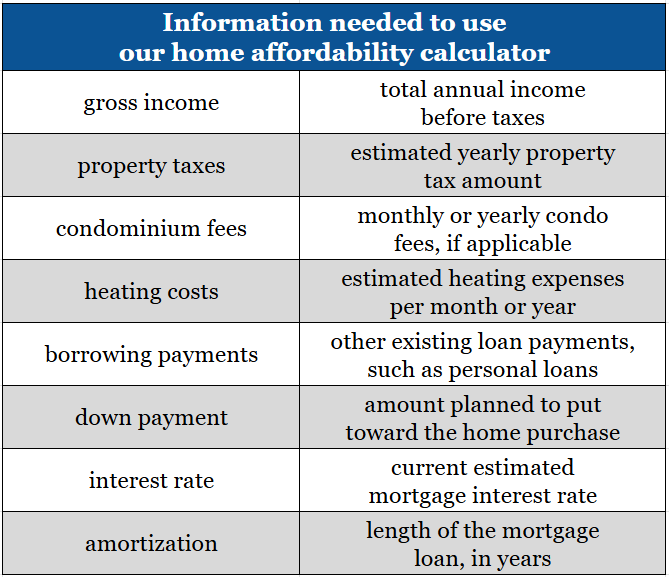

To use our free home affordability calculator, you need to ask for some information from your clients. Then, it will provide you with a price range that fits your clients’ situation. You’ll also see a mortgage vs. down payment pie chart. As for their details, you can use this table as reference:

After entering these details, the calculator will give you an overview of what your clients can afford through these variables:

- maximum purchase price

- monthly payment amount

- maximum affordable mortgage amount

Take note, it's not a full pre-approval. Still, it’ll help your clients understand what they might comfortably afford. Other home affordability calculators might need the following details from property buyers:

- preferred loan term

- homeowners' insurance estimates

- estimated monthly debts (e.g., car payments, credit cards, student loans)

Aside from our free home affordability calculator, we also have another useful tool. Want to help your clients get an estimate on what their monthly mortgage payment would be for a specific loan amount? Go ahead and try our mortgage calculator for free!

Why mortgage brokers should offer a home affordability calculator

It’s not surprising for your clients to expect immediate answers. Some might be feeling excited or anxious while they’re browsing homes online and calculating mortgage payments. They also could’ve been researching rates long before they speak with a mortgage broker.

If you can help them while taking advantage of useful tools like a home affordability calculator, you can gain leverage. This is especially true if you’re aiming to be one of the best in the mortgage industry.

Using a home affordability calculator can also:

- attract more committed homebuyers

- make a good first impression with prospects

- keep the search limited to realistic home options

- establish clear expectations with clients from the get-go

Instead of giving vague estimates, you’ll be able to give your clients a starting point grounded in real numbers. That can make your advice more valuable and your service much harder to replace.

Working better with a home affordability calculator

Every hour you spend working with a client who isn’t financially ready is an hour you lose for a client who’s ready to buy property. A home affordability calculator can help you identify serious homebuyers easily. This is by giving both you and your clients a good idea of the home price that they can manage. It saves you from spending a lot of time with prospects who might not be ready to move forward yet.

Instead of fixing misunderstandings later, you kick things off with solid information that sets the right expectations from the beginning. You can even have more direct discussions about pre-qualification because your clients already have a general idea of their buying power.

When your clients know their budget and what options are available to them, your workflow becomes simpler yet more organized.

Mistakes to avoid when using a home affordability calculator

While home affordability calculators are powerful tools, they’re not perfect. If you rely on them too much or fail to explain their limits, your clients might get the wrong impression. Just like any other mortgage tool, you must treat a home affordability calculator as a guide, not the final answer.

Remember to use it wisely and let your clients be aware of how its results fit into the whole financial picture. Here are some mistakes to avoid when using a home affordability calculator:

- treating the result like an official pre-approval

- overlooking future income changes

- assuming monthly payments are the only affordability measure

Let's discuss them one by one further below:

1. Treating the result like an official pre-approval

Your clients might think that once they see a number from the home affordability calculator, they’re ready to start bidding on properties. You can remind them that these tools only offer estimates based on basic inputs. A full mortgage pre-approval requires verifying income and checking credit history.

Encourage your clients to treat the home affordability calculator’s result as a starting point, not a guarantee.

2. Overlooking future income changes

For clients who are first-time homebuyers, they might plan based on their current earnings without considering income changes in the long run. Their finances can shift due to factors like career moves and family matters. These can affect what they can afford.

So, be sure to advise your clients to build a little breathing room into their budget.

3. Assuming monthly payments are the only affordability measure

Some calculators focus mainly on monthly mortgage payments. However, your clients need to consider the full cost of homeownership that involves the following expenses:

- utilities

- maintenance

- property taxes

- home improvements

- unexpected expenses

- homeowners' insurance

How to calculate home affordability

Calculating an estimate of the home loan that your clients might qualify for is a critical step in determining their budget. When you’re calculating home affordability for your clients, there are many factors that you need to consider such as:

- location

- living costs

- debt payments

- down payment

- gross annual income

Once you have a better understanding of these factors, you can recommend the most suitable kind of property that your clients should be looking for. To calculate their home affordability, you can look at their:

Credit score

Be sure to review your clients’ credit scores early in the process. A higher score can help them qualify for lower interest rates. On the other hand, lower credit scores can lead to higher monthly payments.

Discover what you need to know about credit scores to buy a house. Help your clients qualify and breeze through the mortgage process with these tips.

Income

Gather information about your clients’ monthly earnings from their sources of income. It’ll be beneficial if you have both their gross income (before taxes) and net income (after taxes) ready. These details can be found on their most recent pay stubs.

If your clients are self-employed and looking for mortgages, you can use their latest tax return as a guide.

Debt

List all current debts that your clients are responsible for. It’ll be in your clients’ best interests to pay down debts before applying for a mortgage. This is especially true if they have high-interest debts that could affect their affordability.

Down payment

Find out how much your clients plan to put down upfront for their home purchase. A larger down payment lowers the monthly mortgage payment. Tell your clients that doing so can also remove the need for private mortgage insurance (PMI) if it reaches at least 20 percent of the property price.

Help clients beyond using a home affordability calculator

A home affordability calculator is a powerful starting point, but it’s only part of the bigger picture. While it can provide your clients quick estimates and reassurance about their options, it doesn’t replace careful financial planning.

As a mortgage broker, your job goes beyond just showing numbers. You can help clients understand what their monetary situation means for their homeownership journey. If you use a home affordability calculator alongside real conversations about your clients’ finances, you’re giving them top-notch service.

When you combine useful tools with guidance and experience, you become more than just the average mortgage broker. You can become one of the reasons why your clients feel confident when buying their first home. Plus, you’ll be the first person they recommend to family and friends who want to start their homeownership journey.

Did you use our free home affordability calculator? If you haven’t, give it a try and tell us how it helped you in the comments below.