Discover what you need to know about credit scores to buy a house. Help your clients qualify and breeze through the mortgage process with these tips

One of the most common questions homebuyers ask is about credit scores to buy a house. It’s one of the key elements that impact mortgage approval and interest rates. Many homebuyers, especially first timers, don’t fully understand how their credit score affects the process. They might think that they need perfect credit or might be unaware of what range puts them at risk. That is where your guidance matters.

In this article, Mortgage Professional America will talk about how you can help your clients improve their credit score to buy a house. We will discuss the minimum credit score requirements as well as how scores affect mortgage options. We will also explore how your clients should prepare their credit scores for a mortgage.

What is a good credit score to buy a house?

While the credit score requirements differ from one bank or mortgage lender to another, your clients should aim for a minimum of 620. Still, there are others that can help your clients secure a property loan with less.

For instance, your clients might be able to secure a mortgage with poor credit for an FHA loan. This is a mortgage option backed by the Federal Housing Administration. Interested clients only need a credit score of at least 580 to qualify.

As a mortgage broker, you must help your clients understand that not all financing options will require the same level of creditworthiness. Some mortgage products are more flexible, while others have stricter criteria due to the level of risk involved.

This means that even if your clients’ credit score falls below the standard threshold, they might still qualify for financing under the right mortgage structure.

A good credit score to buy a house also varies based on the type of mortgage that homebuyers are seeking. Different property loan structures come with their own risk assessments. As such, banks and mortgage lenders adjust their credit score expectations.

Learn more about credit scores when you watch this video:

Do you know that mortgage pre-approval can affect your clients’ credit scores? Read this guide to find out.

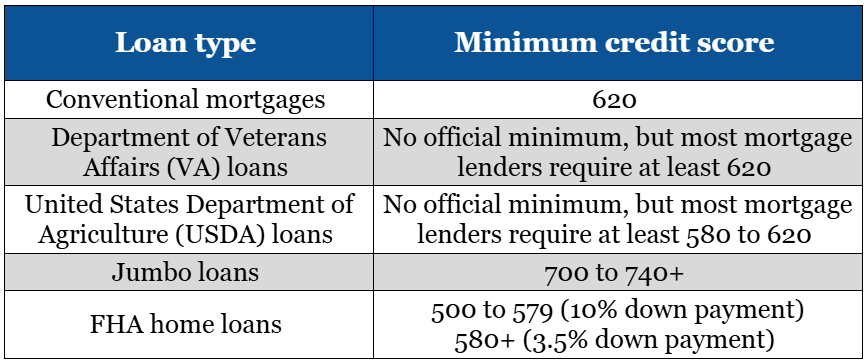

Credit score to buy a house depends on loan type

The minimum credit scores that your clients need will depend on the mortgage type that they apply for. Some property loans require higher scores because they’re not backed by the government. Others allow lower scores to make homeownership more accessible for first-time buyers or those with limited credit history.

Understanding these minimum requirements can guide you in directing your clients toward a realistic but smooth mortgage transaction.

Let’s say your clients have a bad credit score. It might make more sense to recommend a mortgage type that accepts scores under 620 rather than try to qualify them for something stricter.

This approach will save you time and improve your clients’ chances of approval. You can also check out this table on minimum credit scores to buy a house based on various property loan types:

How to raise credit score fast

To improve your clients’ credit scores to buy a house, ask them to review their credit report to learn what makes up credit scores. They can get this report for free from any major credit bureau. Getting mortgage pre-approval will also allow your clients to check their credit scores.

If your clients are interested in raising their credit score, here are some tips:

Pay bills promptly

Since payment history accounts for a large portion of the FICO score, this is the first place to focus on. Remind your clients that even one missed payment can cause setbacks during mortgage pre-approval or underwriting.

Let them know that setting up automatic payments or reminders can help avoid late payments.

Read next: Mortgage pre-approval advice to give to your new clients

Lower credit utilization

Advise your clients to reduce balances where possible. They can also ask for higher credit limits from their chosen bank or mortgage lender. A lower utilization rate can lead to better loan terms and smoother approvals.

Warn against new credit lines

Too many recent hard inquiries can lower your clients’ credit score for several months. Recommend that they avoid opening new accounts while preparing to apply for a mortgage. Explain that even store cards and financing offers can count as hard inquiries.

Keep old accounts open

Rather than closing old accounts, keep old credit lines open so that your clients can catch up on past delinquencies or payments. Let them know that low or occasional use keeps the account active without adding risk.

Stress the importance of patience

Improving credit takes time, especially when preparing for a mortgage. Help your clients stay focused on consistent habits rather than expecting fast results. Remind them that steady progress over a few months can lead to meaningful improvements.

To help your clients improve their credit scores to buy a house, watch this video for additional insights:

Having this knowledge builds your relationship with your clients, especially if they’re satisfied with your services. If you want to grow your business and become a top mortgage professional, knowing how credit impacts home loans is vital.

How do you prepare your credit score for a mortgage?

If your clients are planning to buy property soon, they’d want to prepare their credit scores to secure a mortgage. Here are some quick and easy ways for your clients to prepare their credit scores:

- check credit score and reports

- pay down debt

- give it time

Here is a deeper dive into preparing your credit score for a mortgage:

1. Check credit score and reports

The first step in preparing a client’s credit for a mortgage is helping them understand where they stand. Clients can access their credit score for free from major credit bureaus or through financial institutions. If their score is above 700, they may already qualify for favorable rates with little adjustment.

If the score is low enough to risk denial or trigger high rates, it's often better to delay the application until improvements can be made. After clients get their credit report, encourage them to review it for errors or unfamiliar items. If they find any, they should dispute these with the credit bureau or contact the reporting lender. Correcting these issues is one of the fastest ways to boost a score.

2. Pay down debt

Paying down existing debt, especially credit card balances, is one of the most effective ways to prepare for a mortgage. This not only helps improve credit scores but also lowers your clients’ debt-to-Income (DTI) ratio, which banks and mortgage lenders review closely.

Credit utilization, the amount of credit used compared to the limit, is updated monthly and plays a major role in scoring. A good rule of thumb is to keep utilization under 30 percent. If your clients have high revolving balances, they might see improvements quickly once those debts are reduced.

3. Give it time

Some credit issues require time to improve such as:

- bankruptcies

- repossessions

- Collections

- charge-offs

- late payments

The best strategy for your clients might be to wait and rebuild credit slowly. They should also avoid new negative marks. A stable payment history over time can eventually outweigh older derogatory items.

If they have flexibility and are not in a rush, waiting for better conditions or improved credit could result in better loan terms later. As their mortgage broker, you can help them weigh the financial pros and cons of timing.

What your clients gain by improving their credit score to buy a house

Remember, it can take some time for your clients to improve their credit scores to buy a house—it won’t happen overnight. However, they will reap the benefits once they start the journey of becoming property buyers. Helping them stay consistent and focused during this period can make the eventual approval process much smoother.

Even small improvements in your clients’ credit score can lower their interest rate and lead to long-term savings. Over the life of the mortgage, this could add up to tens of thousands of dollars. Framing it this way can make your clients see the real financial value in taking steps to improve their credit scores.

Do you have clients who are working on improving their credit scores to buy a house? Feel free to tell us about your experience in the comments below