Wondering how much down payment on a house you need to secure your home purchase? Read this article to find out

The down payment you make on your mortgage depends on various factors, including how much you can afford in the short term versus how much you are willing to pay throughout the life of the loan.

What’s a typical down payment on a house? In this article, we’ll talk about what down payment options are available. We’ll go over the pros and cons of making a 20% down payment on a house, along with other points to consider when buying property.

To our audience of mortgage professionals, this article can serve as a valuable tool for any of your clients who are asking how much they will need for a down payment on a house.

How much down payment on a house do you need?

There is no one-size-fits-all answer to how much money you should put toward a down payment when buying a house. There is also no rule as to the minimum down payment on a house. It is, however, important to know how it could impact on your finances in the long term, especially since it is one of the largest upfront expenses that you will make.

If you make a lower down payment on a house, you will likely be on the hook for higher fees and interest over the life of the loan. On the flip side, the more money you pay up front, the lower your fees and interest over the life of the loan.

Saving enough money to make a sizeable down payment will usually take time, meaning that a government-backed 0% down payment, or a conventional loan offering a low down payment (sometimes as low as 3%) may help you to speed up your home purchase.

To figure out which down payment option will best suit your financial situation, use our free mortgage calculator.

What to consider when making a down payment on a house

Here are some considerations you should make when thinking about the down payment:

- Interest rates

- Home equity

- Monthly mortgage payments

- Upfront and ongoing fees

Here is a closer look at those factors:

1. Interest rates

If you make a smaller down payment, lenders may add a few fractions of a percentage point onto your interest rate throughout the life of the loan. The same is true if you make a larger down payment; lenders will shave a few fractions of a percentage point off your interest rate.

If you pay more up front, you are less of a risk—and lenders tend to reward this with lower interest rates.

2. Home equity

Home equity is the value of your home minus whatever you owe on your mortgage. Put another way, it is the difference between your property becoming an asset rather than a debt.

When you make a larger down payment on a property, you immediately have more equity. And the more equity you have, the more wealth you have. The less equity you have, the less wealth you have.

3. Monthly mortgage payments

Your principal is lower if you borrow less of the price of your property (and means you will pay less in interest, as mentioned). Paying more toward the principal will help reduce your monthly mortgage payments throughout the life of the home loan.

4. Upfront and ongoing fees

By guaranteeing a part of a mortgage, government-backed mortgage programs or low-down-payment conventional loans reduce risk for mortgage lenders. In other words, mortgage lenders are reimbursed by the associated government agency if you default on either of these loans.

To offset a portion of the costs, these loans often carry with them significant one-time costs. Depending on what you decide, you may be on the hook for either high upfront fees or high ongoing fees.

The pros and cons of making 20% down payment on a house

For many potential homeowners, making a 20% down payment on a home can seem next to impossible. After all, for a house that costs $400,000, that means you would have to pay $80,000 up front.

On the plus side, there are not that many lenders that require 20% at closing. While it may not be required in many cases, if it makes financial sense, you should consider it.

But before committing to anything, it is important to weigh the pros and cons of making a 20% down payment. Here is a breakdown of both:

Let’s take a more in-depth look at the benefits of making a 20% down payment on a house:

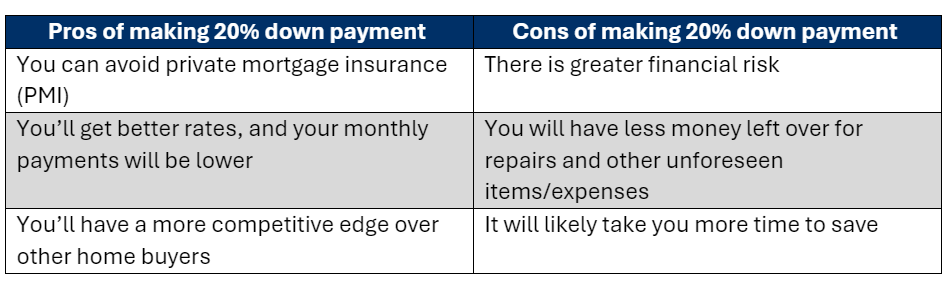

The pros of making 20% down payment

1. You can avoid Private Mortgage Insurance (PMI)

If you want to avoid paying private mortgage insurance—which protects the mortgage lender if you default on your loan—you will have to make a 20% down payment. Keep in mind that, when you reach 20% equity in your house, you can ask the lender to remove the PMI, even if you did not put 20% down initially.

Equity is the amount of the property’s value that you own. Among the various ways that you can gain equity are:

- the value of your property increases

- you make enough mortgage payments to pay off the principal

Mortgage lenders typically cancel your PMI after you have built at minimum 22% equity in your home.

2. Better interest rate

Your interest rate is what your lender will charge you every month for borrowing money. It is the outstanding balance on your mortgage or the percentage of the principal.

Essentially, lenders will view you as less risky if you make a higher down payment. Toward that end, putting down at least 20% on your mortgage at closing may allow you to access better/lower interest rates.

An interest rate that is even one or two points less can save you thousands of dollars during the life of your loan.

3. Lower monthly payments

You will end up needing to borrow less money if you make a larger down payment. The less you borrow, the lower your monthly payments will be. This should free up money for unforeseen expenses that may arise every month.

Read more: Average down payment on a house: Everything you need to know

4. Competitive edge over other home buyers

Most home sellers would usually rather work with home buyers who have made a 20% down payment since it shows the buyer’s finances are in order. This means that if you are the buyer, you will likely have less issue finding a lender and will therefore give you an edge over other home buyers.

Now, let’s look at the drawbacks of making a 20% down payment:

The cons of a 20% down payment

1. Greater financial risk

After you put down a larger sum of money, it can be difficult to get it back if necessary. Depending on your financial situation, you may want to put that extra money toward an emergency fund, or if you feel you may need to pay for some important and unforeseen expenses later.

2. Less money for repairs

New home buyers usually see homes that need minor repairs as a bargain. But the bigger your down payment, the less you will have left over for additional repairs.

3. Saving takes more time

Saving for a 20% down payment can take a long time, spanning decades in some cases. Trying to save for that many years can be especially costly if you are paying rent at the same time. You may be better off purchasing a property now with a lower down payment than you would be saving for a 20% down payment while also paying rent.

What is the lowest down payment on a house?

For certain government-backed loans, you can make a 0% down payment. The average down payment is 20%, if it makes financial sense for you. However, there are some conventional loans or mortgages that require as little as 3% down payment.

Here is a look at the lowest down payments you can make on a house, depending on the mortgage you want to apply for:

0% down payment

VA loans for mortgages, which are guaranteed by the US Department of Veterans Affairs, do not usually require a down payment. These types of loans are for acting veteran military service members and spouses who are eligible.

Another government-backed loan that often requires no down payment is a USDA loan. These are backed by the US Department of Agriculture’s Rural Development program and are for suburban and rural home buyers that meet the income limits of the program.

3% down payment

There are conventional mortgages out there that require as little as 3% down payment. Some examples of this type of loan include Home Possible and HomeReady.

Unlike VA loans and USDA loans, conventional mortgages are not backed by the government, instead following down payment guidelines set by government-sponsored enterprises (GSEs).

3.5% down payment

Federal Housing Administration loans (FHA loans) require as little as 3.5% down payment, but your credit score must be at least 580. FHA loans require a 10% down payment if your credit score falls between 500 and 579.

10% down payment

Jumbo loans typically require a 10% minimum down payment. These types of loans, which are outside of Federal Housing Finance Agency conforming loan limits, cannot be guaranteed by GSEs. Lenders often require higher down payments to mitigate some of the risks.

In this video, the presenter suggests making a 5% down payment on a house. Find out why:

To help you decide how much down payment to make on a house, seek the advice of experts in the mortgage industry. Check out our Best in Mortgage page for the top brokers and mortgage professionals across the US.

How much are closing costs?

Closing costs are the fees for services that helped to officially close the deal on the property. Typically, home buyers will pay between 3% and 4% of the sales price in closing costs.

Closing costs for home buyers often include:

- a home inspection paid prior to closing day

- a home appraisal

- title insurance

- origination fees

- homeowners’ insurance and taxes

The cost of home inspection—which is usually about the same as the home appraisal—is for a professional to examine the property to spot any issues or damages prior to buying.

The home inspection and the home appraisal can cost anywhere from $280 to $400. Both these costs are essentially the lender’s assurances that the home is worth the money you are being lent.

Read more: Closing costs: What are they and how are they estimated?

Other closing costs such as taxes, title fees, and loan origination fees are typically much higher than inspection and appraisal costs. However, those higher closing costs are more difficult to calculate since they vary depending on where you are purchasing the property. They may cost 1% of the sales price of the property.

Use our home affordability calculator to find what your clients can afford!

How much should a down payment on a house be?

Twenty percent is the standard rate that most realtors or direct home sellers are willing to work with.

You can always pay a larger initial down payment to bring down your monthly mortgage payments and make it less of a financial burden. Paying a bigger down payment than the standard 20% can also signify to the home seller that your finances are stable. This can give you an edge over other buyers interested in the same home.

Do you have to put a 20% down payment on a house?

Although 20 percent is the widely accepted standard for a down payment on a home, this is not mandatory. It is possible to make a smaller down payment, as there are no minimum requirements for a down payment on a house.

In fact, a report by the National Association of Realtors revealed that the average down payment made in the US for a home was 14% in 2023, and not 20%.

Private mortgage insurance (PMI) is probably the only real requirement when you make a down payment on a house below the standard 20%. Also, if you are struggling with the down payment costs, there are down payment assistance programs offered by state and local governments that can aid you.

Can I buy a house without a down payment?

The short answer is yes, you can buy a house without a down payment. If you are in the market for a conventional mortgage, however, you will have to make a down payment. To get a zero-down conventional mortgage, you would need to get a government-backed loan.

Government-backed loans are exactly what they imply. These are mortgages that the government insures, presenting less of a risk to lenders since the government will cover the financial loss in the case of a default. It also means that most lenders will offer more lenient down payment requirements and interest rates that are below average.

If you qualify for a VA loan or a USDA loan, you can currently purchase a property with no money down. If you are a former or current spouse of a member of the Armed Forces, you may also qualify for a VA loan.

While both government-backed loans offer zero-down payment guarantees, you must meet the minimum requirements set by the Department of Veteran Affairs (VA) and the USDA.

Is it worth putting down 50% on a home?

That depends on your finances and individual needs. The benefits of paying half down on a house are quite clear, as you can significantly reduce your monthly mortgage payments. You’ll have less to pay every month and have more money in your pocket for other expenses.

You’ll be paying less on the mortgage’s interest if you pay 50% up front. You can save hundreds of thousands of dollars in interest payments if you make that big a down payment.

There are downsides and risks to making a 50% down payment. For one, you’d be tying up more of your cash in an asset that isn’t very liquid and takes time to appreciate. This may pose a problem, especially if you find yourself in need of quick cash down the line.

For example, what if you or a family member sustains an injury and must take time off work to recover? What if your home is damaged in a hurricane or other unforeseen event and needs repairs? If you had made a 20% down payment instead of a 50% down payment, you would have had some more money to cover these unforeseen expenses.

In these cases, you may find yourself needing to borrow money from friends and relatives, or worse, taking out a loan on your home’s equity. This may have you spending more to pay for the mortgage and repaying the loan.

Here’s another drawback: the stock market has been giving an average return of 10% per year for the past 50 years. Investing your down payment in the stock market could have yielded a significant return.

Here’s a video that provides some good food for thought about the size of your initial down payment on a house. Another angle about making a smaller down payment as opposed to, say, 50% down is that you can use the money to invest in other rental properties. Check out what the video presenter has to say here:

A 50% down payment on your home may not always be financially sound, so perhaps it would be best to consult a financial planner on how much to put down and what to do with the rest of your money.

The average down payment on a house for first-time buyers is pegged at around 20%, but it’s clear that this is not a rule set in stone. A good strategy is to consult a financial planner or advisor to determine which is a good percentage of your home’s purchase price to make as a down payment. Consider all the risks, benefits, and disadvantages to help you make an informed financial decision, then go for it.

Do you have prior experience with making a down payment on a house? Share your thoughts in the comments.