Lenders who dedicate resources to both the back- and front-end of their business enjoy the most benefits

Coming on the heels of Fannie Mae’s recent Mortgage Lender Sentiment Survey, the GSE on Wednesday released a new Special Topics Report, Impact of Digital Innovation on Lender Workforce Management.

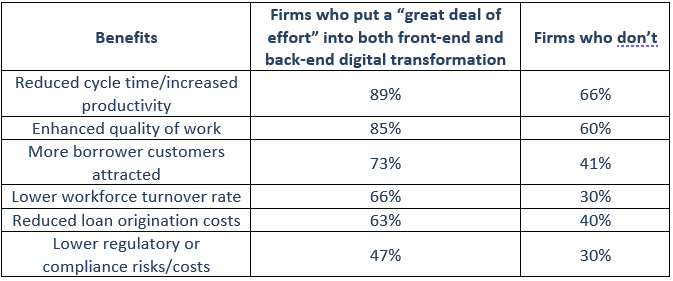

The report, based on responses from 195 senior executives, finds that lenders who dedicate a “great deal of effort into both the front-end and back-end digital transformation” experience far greater business benefits than those who do not – and it’s not even close.

The survey found that roughly half of respondents, 48 percent, are dedicating resources to improve both ends of their businesses. For Chris Boyle, who spent 30 years at Freddie Mac and is now an advisor at Roostify, it’s a trend that was long overdue.

“As other industries have moved along, the mortgage business really hasn’t. The cost to produce a loan has been exceedingly high,” Boyle says, adding that it still requires around 5,000 bits of paper to produce a mortgage loan. “It’s a journey that everyone has wanted to be on, both to give consumers a better experience by automating what is a really expensive, manual process, and to improve technology.”

While 58 percent of respondents said they are prioritizing back-end digital transformation, 68 percent said their focus is on front-end systems. Boyle says the discrepancy is less a sign of unbalanced priorities than it is an emphasis on modernizing what is arguably the most manual, time-consuming and costly side of the business.

“I think lenders focusing there, where they first meet a consumer, is really the right place to go,” she says.

Fannie also found that companies who invest in both front-end and back-end transformation have seen changes in the responsibilities of some of their key roles. Ten percent said their compliance/legal responsibilities have contracted in the last two to three years. Of the firms taking an alternate approach to digital transformation, 15 percent reported an increase in compliance/legal responsibilities.

The divergence does not surprise Boyle.

“You can put so many new rules and guidance into a digital solution that takes the human aspect – the judgement, if you will – out,” she says. “The compliance role goes down quite dramatically because you’re not looking for that human error. You’re relying on machine learning and data and analytics, which gives greater certainty.”

The survey also asked about lender sentiment around whether outsourcing the loan origination process would benefit the mortgage industry. The answer was a resounding ‘no’: 81 percent of respondents are not in favor of outsourcing. But that still means almost 20 percent are either in favor or unsure of outsourcing’s future role in originations.

Boyle feels the client experience is too important for most mortgage firms to trust to a third-party. After decades in the industry, she has yet to see a groundswell of support for outsourcing origination work.

“That client experience is something you really don’t want to outsource,” she says, adding that the accessibility, information and feeling of importance a client gets when dealing directly with a lender are hard to guarantee when a third-party is involved.

“They want to manage those clients, serve them well and really create a client for life.”