Study pointed to slower premium growth in 2025 but wide state‑by‑state gaps

Homeowners in Newrez’s servicing book faced higher insurance costs over the past four years, but the pace of increase appeared to cool in 2025, according to a new internal study from the lender and servicer.

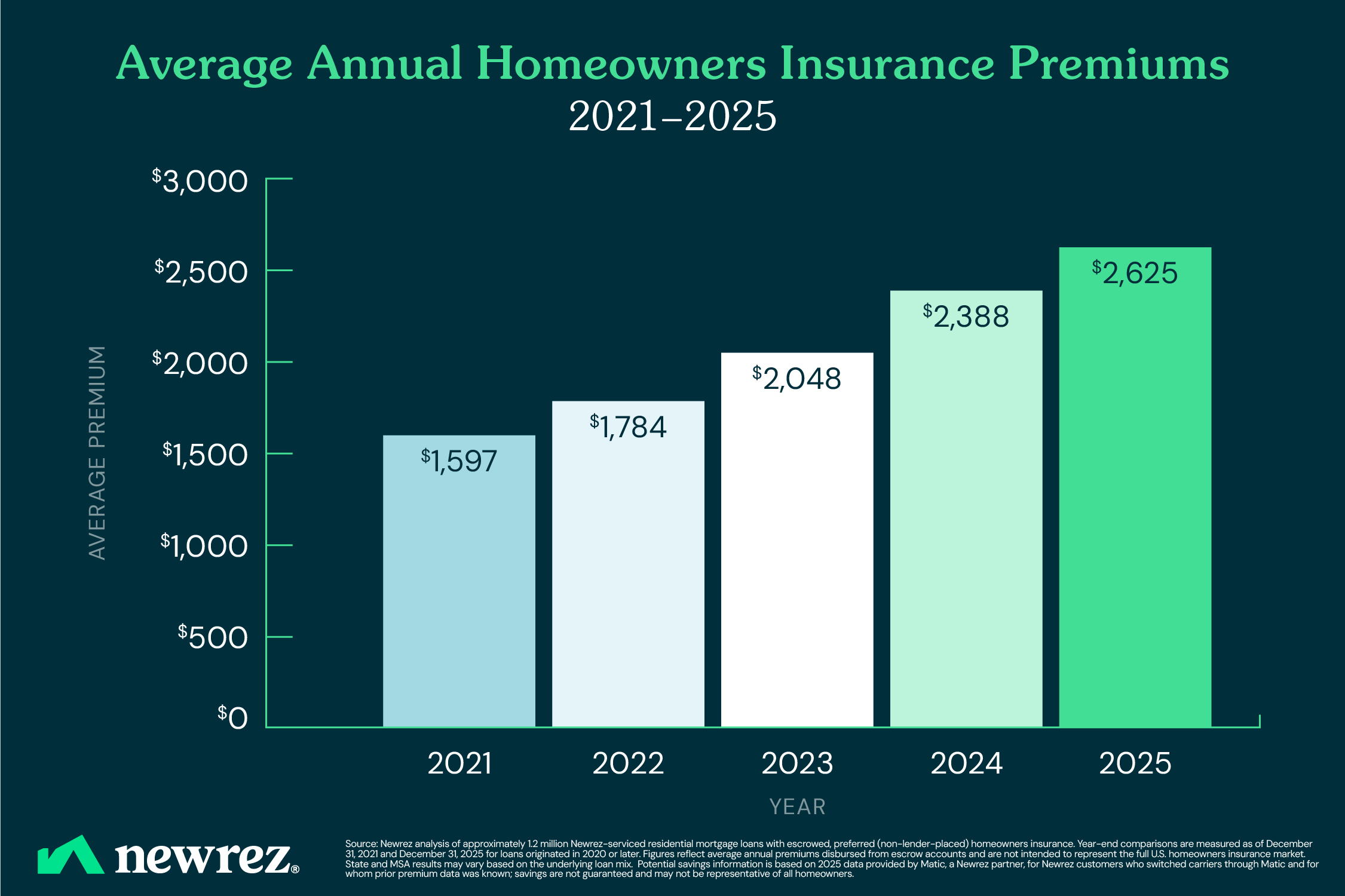

The analysis of roughly 1.2 million escrowed loans found the average annual homeowners insurance premium rose 64% between year‑end 2021 and year‑end 2025, climbing from $1,597 to $2,625.

The company said premium growth nevertheless slowed to 10% in 2025 – the lowest rate since 2021, after a run of double‑digit gains from 2022 through 2024.

It added that, over the same period, typical home values rose by about $50,000, citing the Zillow Home Value Index, which helped support borrower equity positions and household balance sheets.

State‑by‑state gaps and shopping for relief

Premiums “varied meaningfully by geography within the Newrez‑serviced portfolio,” the study said.

At year‑end 2025, Louisiana posted the highest average annual premium at $4,238, followed by Florida at $4,060 and Texas at $3,952.

Arizona registered the steepest increase from 2021 to 2025 at 94%, while Alaska recorded the smallest rise at 27%.

“For many Americans, their home is their largest and most important asset, and this is why it’s especially important for borrowers to understand how insurance fits into their overall cost of homeownership and to stay proactive about reviewing coverage,” Ross said.

Insurance squeeze met with borrower resilience

“Homeowners insurance has become a much larger component of housing costs for many homeowners since 2021, as more frequent severe weather events and higher rebuilding costs are putting pressure on insurers,” Newrez head of servicing Shane Ross said.

“At the same time, while certain borrower segments face more acute affordability pressures, overall mortgage delinquency rates remain below historical averages, suggesting a broader level of homeowner resilience even as insurance and other housing costs rise.”

Newrez reported that, even as premiums climbed, overall delinquencies in its portfolio remained below long‑run norms, a trend consistent with broader industry commentary that strong equity cushions and pandemic‑era refinancing continued to underpin performance.

Meanwhile, according to Matic's survey data, 64% of mortgage lenders reported experiencing issues with home insurance either frequently or somewhat frequently.

Elevated insurance costs are directly impacting borrowers' debt-to-income ratios, delaying closings, and in some cases preventing borrowers from qualifying altogether.

Thirty-seven percent of mortgage lenders reported clients who had to opt for a less expensive home because of insurance costs.

Many loan officers report walking away from one to two loans per month specifically because of insurance-driven DTI problems.

Stay updated with the freshest mortgage news. Get exclusive interviews, breaking news, and industry events in your inbox, and always be the first to know by subscribing to our FREE daily newsletter.