At the final stages of your mortgage process comes estimated closing costs. What are they? How much do you need to pay them off? Read on to find out

Despite what the term may suggest, closing costs are anything but an afterthought. Often, you will end up paying thousands of dollars in closing costs in property-related fees, mortgage-related fees, and additional fees. But do not worry. If you do your due diligence during the pre-approval process of your home loan, there should be no significant price jumps or surprises.

Here is everything you need to know about estimated closing costs, including how to calculate closing costs and who pays at closing. Mortgage Professional will also discuss how to reduce these fees. For our usual readers of mortgage professionals, this is part of our client education series. As such, we encourage you to pass this along to your clients who have questions about their estimated closing costs.

What are closing costs?

Closing costs are fees that are paid to the professionals who helped you in finalizing the complex process of your mortgage application and real estate sale. As the term implies, you pay your closing costs at closing.

Watch this video to learn more about closing costs in the US:

You can also check out this article about what closing costs are for more information.

Here are the usual fees included in closing costs:

- property-related fees

- mortgage-related fees

- additional fees

To analyze what these fees are and what they include, let us break them down further below:

Property-related fees

Property-related fees are the costs associated with the home and the expenses that verify the home’s value and ownership. Since your property is the collateral for the mortgage, this is critical.

Here are some common property-related fees that are included in estimated closing costs:

- appraisal fee

- home inspection fee

- title search

- title insurance

- property tax

Let’s take a closer look at each property-related fee:

1. Appraisal fee

This will cover the licensed professional’s work in determining the worth of the property. You can expect to pay a higher appraisal fee for a larger home compared to a single-family home. You usually pay this fee well before closing day.

2. Home inspection fee

A home inspection fee is separate from your appraisal fee and is paid to the home inspector who evaluates the condition of the property. This fee usually costs a few hundred dollars on average.

Hiring a home inspector is optional, but we still recommend it for an accurate assessment of your property. It’s always better to know if there are any issues with your chosen home or property for sale.

3. Title search

Lenders often have a title company search property record to ensure there are no issues with the property title. So, unless you are buying your home brand new, you should prepare a decent amount for the title search.

4. Title insurance

Most mortgage lenders require that you get title insurance in case there are problems with ownership post-sale. This acts as an added protection for the lenders. Usually, title insurance costs between 0.5% and 1% of the amount you are borrowing.

If you want to pay more, you can buy your own title insurance policy to protect your financial interest in the property.

5. Property tax

At closing, you may also be required to pay from six months to one year’s worth of property taxes. This amount can fluctuate depending on the area you are in.

Mortgage-related fees

Mortgage-related fees are charges associated with the mortgage application with the bank or lender. Typically, these fees include:

- credit report fee

- origination fee

- application fee

- underwriting fee

- points

Here is a look at these common mortgage-related fees that come with closing costs:

1. Credit report fee

A credit report fee is paid to your lender to check your credit score when buying a house and credit report.

2. Origination fee

This is a fee that mortgage lenders or banks charge for the creation of the loan. Origination fees usually range from 0.5% to 1% of the loan. This fee is how lenders or banks get profit from mortgages.

3. Application fee

To process your loan application, lenders or banks may charge a fee of a few hundred dollars. This payment is known as an application fee.

4. Underwriting fee

An underwriting fee is also considered as a processing fee or an administrative fee. This pays for the evaluation and verification of your financial eligibility and qualification.

5. Points

You can pay an added charge known as discount points or mortgage points to lower the interest rate on your mortgage. For a lower rate, most lenders will let you pay points. This will have a big impact on the amount of interest you will pay over the life of your home loan. Be warned, however, that it will raise your closing costs.

Additional fees

Beyond paying property-related fees and mortgage-related fees, you may have to pay additional fees at closing. These might include prepaid items and miscellaneous charges, for example. You may also have to cover additional fees and taxes depending on the area where the property is in.

To avoid surprise and out-of-budget expenses, it is important to know beforehand where these extra fees might come from and how much they may cost you.

How much are closing costs in the US?

For an estimated amount of closing costs, the average figure for a single-family home is around $6,905, including taxes that get transferred. Without those taxes, buyers should be ready to shell out around $3,860, according to ClosingCorp’s data as reported on the financial website Bankrate.

Closing costs are also paid not only when you buy property but also when you refinance your mortgage. On average, they cost approximately $2,375.

What is a good formula for estimated closing costs?

On average, closing costs range from 3% to 6% of the home's purchase price in the US. For instance, if you purchase a property for $300,000, your estimated closing costs could be anywhere from $9,000 to $18,000. However, this amount can vary depending on significant factors such as:

- mortgage lender

- type of home loan

- area you live in

The basic formula that you can use to get an estimated closing cost is:

Home price ($300,000) x Loan amount percentage (0.03-0.06) = Closing costs ($9,000-$18,000)

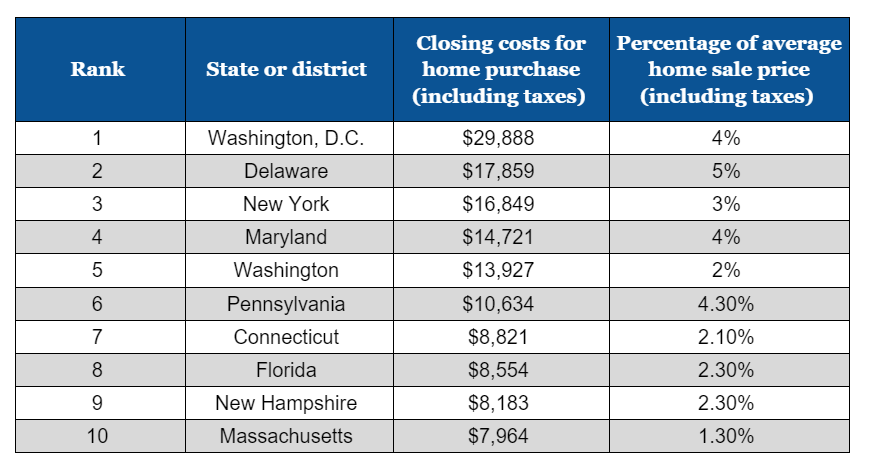

Closing costs are different in every US state

Closing costs tend to be different depending on what state or district you are in. In some places, they are less than 1% of the home's sale price. They can be 5% or even more in other areas. These percentages also differ from urban locations to rural areas.

Washington, D.C. has the highest average closing costs in the country at $29,888. Missouri lands the lowest spot with average closing costs amounting to $2,061. The good news is that homebuyers may be able to negotiate and lower some of these upfront fees when buying a home.

Below is a comparative table of states with the most expensive closing costs:

Who pays at closing: buyer or seller?

As a rule of thumb, both buyers and sellers pay closing costs. The price breakdown of payments will depend on what both parties negotiated beforehand.

Buyers’ closing costs

While estimated closing costs for buyers can include other charges, they usually include:

- loan fees

- credit report fees

- title search

- lender’s title insurance

- homeowner's insurance

- inspections

- appraisals

- surveys

- settlements

- attorney fees

Sellers’ closing costs

Just like the buyers, closing costs for sellers may also vary. The agreement prior determines the payments covered and the common ones are:

- real estate agent’s commission

- buyer’s title insurance

- mortgage pre-payment penalties

- outstanding debts on the property

- seller's attorney fees

- transfer taxes

- recording fees

Sellers can agree to pay some of the closing costs as determined by the negotiation. In general, sellers will do this to encourage buyers to buy slow-moving properties or if the seller is motivated to sell fast.

If you are purchasing property, you may ask the seller to pay closing costs instead of lowering the sales price. If you agree to a fast closing, sellers are more likely to be motivated to accept this offer. You can expect a similar outcome if you make fewer demands for changes to the home or repairs.

How soon after closing do I get the keys?

The short answer is that you will get the keys to your new home immediately after closing. To put it simply, homeownership becomes official on closing day.

The good news is that closing day will only take a few hours at most. This means that if you have everything wrapped up before 3 p.m. and it's not a Friday, you'll get your new keys that same day.

Get the bulk of your administration finished on closing day. This means transferring your downpayment to your lawyer. Aside from that, these are some of the other fees that you should transfer several days before closing day:

- state and local government fees

- prepaid insurance premiums (if applicable)

- underwriting and origination fees

- additional charges

Here is a quick checklist on closing day:

- mortgage lender providing the mortgage funds to your notary or lawyer

- you, as the buyer, transferring your downpayment (minus the deposit) to your notary or lawyer, along with other closing costs

- your notary or lawyer paying the previous owner

- your notary or lawyer registering the home in your name

- your notary or lawyer handing you the deed and keys to your new home

If you want an expert by your side at every step, visit our Best in Mortgage section for top names in the US mortgage industry.

How do you reduce closing costs?

Closing costs can feel overwhelming, especially after shelling out a big amount of money for downpayment, moving expenses, and home repairs (if any). There are some ways, however, for you to reduce your closing costs:

- shopping around

- scheduling the closing for the end of the month

- appealing to the seller for aid

- comparing loan estimates and losing disclosure forms

- including closing costs in your mortgage

Let us take a closer look at each to give you a better idea how they may help:

1. Shopping around

Getting a variety of estimated closing costs between lenders and third-party services—like homeowners' insurance and title companies—may save you a few dollars. Keep in mind as well that you are not obligated to use the title company or homeowners' insurance agent suggested by your lender.

Shopping around can also help you find competitive terms and rates for:

- underwriting fees

- application fees

- broker rebates

- loan processing fees

- rate lock fees

2. Scheduling the closing for the end of the month

If you want to limit pre-paid daily interest charges, you can schedule your closing date closer to the end of the month. That way, you will incur less interest expense since you will also incur debt more slowly. If you want to determine how much you stand to save, you can have a lender run this scenario for you.

3. Appealing to the seller for aid

By negotiating, you may be able to convince the seller to cover some of the estimated closing costs or lower the purchase price. If the seller is motivated and the home has been on the market for some time, appealing to the seller to lower the closing costs may be more likely.

4. Comparing loan estimates and losing disclosure forms

It is important to review your initial loan estimate. This can be done by requesting the bank or mortgage lender to clarify fees or charges that you are unsure of. Red flags should appear when lenders either cannot explain a fee or push back when asked.

You can also request that your lender walk you through details if you see fees or increases in closing costs. While fluctuations in closing costs are common, significant increases or surprise additions may affect your ability to close.

5. Including closing costs in your mortgage

Some lenders may offer to include your closing costs in your home loan or offer to pay them. This does not mean you can avoid the costs. Lenders charge higher interest rates to cover the costs of including closing costs in your mortgage.

This should be a last resort because you may ultimately end up paying interest on those closing costs and higher interest on your mortgage.

Can closing costs be included in a loan with FHA?

Yes. Closing costs can be included in the FHA loan amount if the lender provides a no-closing cost loan option. This allows the borrower to avoid paying the closing costs upfront, as they are instead rolled into the total loan balance.

While this may increase the total amount financed, it can be a convenient option for homebuyers who prefer to minimize their out-of-pocket expenses at the time of purchase.

What not to do after closing on a house

There are a few things that you should not do after closing on a house. One is that you should avoid changing jobs. You should wait at least until after you have finished the mortgage application process and closed on the home loan.

Switching jobs prior to closing might impact your loan approval process. If you do switch jobs, you could delay your closing. Worse, you might fail to qualify for the loan.

After closing on a house, do not:

- purchase or lease a new vehicle

- sign up for deferred loans

- forget to remind your lender of an influx of cash

- run up credit card debt

- open new credit card accounts

While the number of fees that come with closing costs may seem overwhelming, a good mortgage professional will help you navigate the process. It may sound complex, but you can get your estimated closing costs ahead of time. Perhaps you can even negotiate to reduce them.

Factoring in your estimated closing costs

When purchasing a home in the United States, property buyers should factor in more than just the home's sale price. For first time buyers, closing costs must not be overlooked. Remember, the various fees and charges associated with finalizing a mortgage can add thousands of dollars to the total cost of a home purchase.

Taking the time to understand what’s included in closing costs and how to potentially reduce them can go a long way. For mortgage professionals, this can help your clients avoid any unwelcome surprises when closing on their new home.

Finally, being proactive in budgeting for these expenses upfront is an important step in making your homebuying transaction smooth and worry-free.

What do you think about this guide on estimated closing costs for property buyers and sellers? Do you find it helpful? Let us know in the comments section below.