How will this affect mortgage rates?

The Bank of England has held the base rate at 3.75%, with the Monetary Policy Committee (MPC) voting 7-2 to maintain the current level at its June meeting.

Global energy prices have fallen since the last meeting but remain elevated and volatile, with the Bank focused on ensuring economic adjustment delivers the 2% inflation target sustainably. CPI inflation has eased to 2.8% but is expected to rise as energy effects pass through. Second-round wage and price pressures remain a risk, though a loosening labour market and above pre-conflict borrowing costs should contain inflation over time.

"Taking all the risks to the economic outlook into account, the Committee judges that it is appropriate to maintain Bank Rate at this meeting," the MPC stated.

The Monetary Policy Committee voted 7-2 to keep the interest rate at 3.75%.

— Bank of England (@bankofengland) June 18, 2026

Find out more:https://t.co/GHHt7QdrbF pic.twitter.com/eCoNh0Y7SL

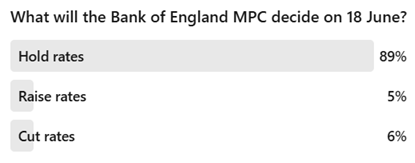

The decision to hold was widely anticipated. Every economist surveyed in a Reuters poll published a week ahead of the meeting forecast no change, and nearly nine in 10 brokers surveyed by Mortgage Introducer expected the same outcome.

Source: Mortgage Introducer survey results

The vote at April's meeting — the most recent prior to this week's decision — was 8–1 in favour of a hold, with one member voting for a 25 basis point increase to 4%. That dissenting vote marked the first call for a rise since the tightening cycle concluded in summer 2023.

"A hold was the expected outcome and should not be mistaken for the Bank turning decisively dovish," said Nicholas Mendes (pictured right), mortgage technical manager at London broker John Charcol. "Inflation at 2.8% is still well above the 2% target, the Ofgem cap is set to push energy bills higher in the coming months, and the Bank will want to see clear evidence that the recent improvement is durable before doing anything more."

"A hold was the expected outcome and should not be mistaken for the Bank turning decisively dovish," said Nicholas Mendes (pictured right), mortgage technical manager at London broker John Charcol. "Inflation at 2.8% is still well above the 2% target, the Ofgem cap is set to push energy bills higher in the coming months, and the Bank will want to see clear evidence that the recent improvement is durable before doing anything more."

Mendes cautioned against assuming the decision would translate directly into lower mortgage rates. "For mortgage borrowers, a hold does not automatically mean rates tumble from here," he stressed.

"Fixed pricing is driven by swap rates and lender funding expectations rather than Bank Rate alone, and those have already moved. The softer inflation print and the ceasefire should help swaps stay calmer, and that does open the door to further gentle reductions. There has even been talk of a mortgage price war as lenders compete for the large number of borrowers due to remortgage over the next year. I would treat that with some caution. The recent cuts have tended to be small and frequent rather than dramatic, and that is the more realistic shape of things to come."

On the outlook for rate cuts, Mendes was measured. "The bigger question is what it takes for the Bank to start cutting again, and that is unlikely to be answered quickly," he said.

"Inflation does not have to be back at target for a cut to happen, but the Bank will want to be confident that higher energy costs have not pushed up pay and prices more widely before it moves. For borrowers, the practical message is not to bank on a cut arriving in time to rescue a deal that is ending soon."

Mendes also advised borrowers against waiting for greater market clarity before acting. "The sensible approach has not changed. Do not try to time the market around a single MPC decision or one round of lender cuts," he said. "Pricing is still being pulled around by swaps, funding costs, and expectations for where rates head next, and the outlook can turn quickly on a fresh piece of news, as the last few months have shown."

"Anyone coming to the end of a fixed deal should look early, secure a rate where they can, and speak to a broker about the options. In this kind of market, it is usually better to lock in an affordable deal and keep it under review than to sit on the sidelines waiting for a clearer signal that may never quite arrive. A broker can hold the rate that is available now while still watching for a better one before completion, which matters when pricing is moving in small steps and the market is reacting to each new headline."

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.