Borrowers hoping for rate relief may have to wait as lenders remain cautious on pricing

The Bank of England has decided to keep the base interest rate at 3.75%, giving policymakers more time to assess inflation risks linked to higher energy costs and weaker domestic conditions.

The Monetary Policy Committee (MPC) had been expected to leave rates unchanged after governor Andrew Bailey signalled that an immediate increase was unlikely. The central bank also left the base rate unchanged at its last meeting, when the MPC voted unanimously to maintain it.

The latest 8–1 decision comes as the Bank faces the prospect of inflation staying above target for the remainder of 2026. Higher energy-related costs, stronger than expected business activity in April and uncertainty over oil and gas markets have left policymakers balancing inflation risks against signs of softness in the labour market.

The Bank had unsettled financial markets after its March meeting, when its language was taken by some traders as pointing to a possible April rate rise. Bailey later pushed back against those expectations, saying markets were moving too quickly in pricing in an increase.

He has argued that weak labour market conditions and limited company pricing power reduce the need for an immediate policy change. However, new Bank scenarios linked to the energy crisis could still show the risk of a longer disruption to oil and gas supplies, leaving the possibility of higher rates later in the year.

An adverse case published by the International Monetary Fund last month showed that oil prices of $100 a barrel throughout 2026 could lift global inflation to 5.4%, compared with 4.4% under a short-lived disruption scenario.

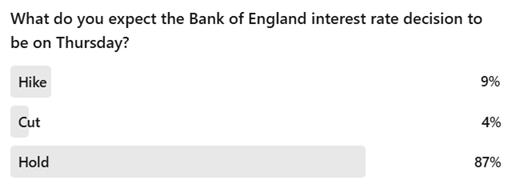

The decision to hold rates was widely expected by the market. A couple of brokers interviewed by Mortgage Introducer earlier in the week predicted that the central bank would keep the base rate unchanged this month. A Mortgage Introducer poll also supported that view, with an overwhelming majority of respondents, as of Thursday morning, expecting the Bank of England to hold the base rate.

“A hold should not be mistaken for a sign that the Bank is relaxed about the outlook,” said industry commentator Nicholas Mendes (pictured right) of London broker John Charcol. “This is still a difficult backdrop, with inflation pressure picking up again while growth remains weak and the labour market shows signs of softening.

“A hold should not be mistaken for a sign that the Bank is relaxed about the outlook,” said industry commentator Nicholas Mendes (pictured right) of London broker John Charcol. “This is still a difficult backdrop, with inflation pressure picking up again while growth remains weak and the labour market shows signs of softening.

“For mortgage borrowers, a hold does not automatically mean mortgage rates are about to fall. Fixed mortgage pricing is driven more by swap rates and lender funding expectations than by Bank Rate alone. If markets still believe rates may need to move higher later in the year, lenders are likely to remain cautious.”

“We may still see selective cuts where individual lenders want to compete, or where funding costs ease for a period, but borrowers should be careful not to read that as a sustained downward trend.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.