What does this mean for borrowers?

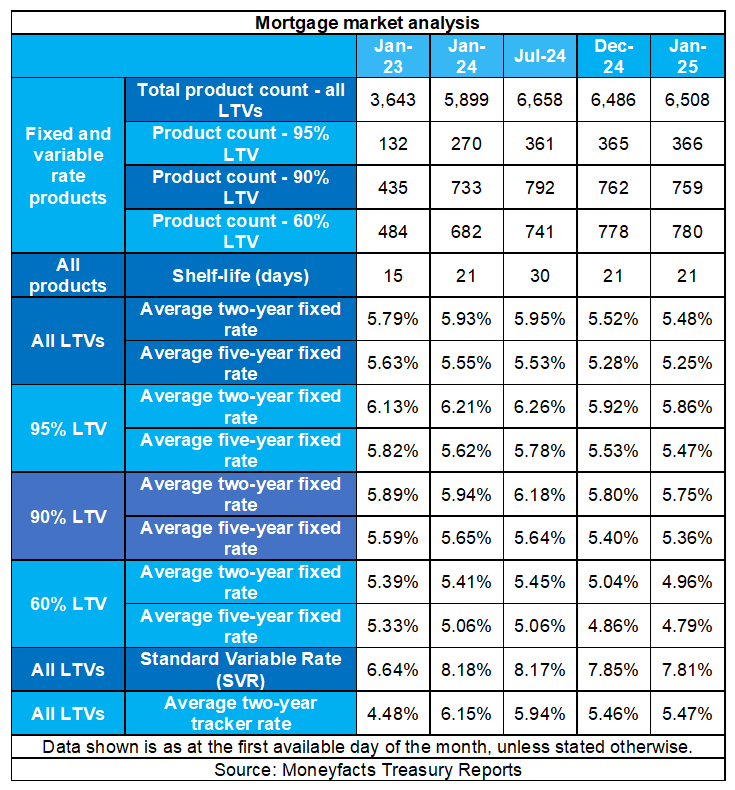

The gap between average two- and five-year fixed mortgage rates in the UK has narrowed to its lowest level in two years, according to the latest Moneyfacts UK Mortgage Trends Treasury Report.

The report shows the average two-year fixed mortgage rate dropped by 0.04% to 5.48%, while the average five-year fixed rate fell by 0.03% to 5.25%. This brings the difference between the two rates to 0.23%, the smallest margin since January 2023, when the gap stood at 0.16%.

At the start of January 2024, the average five-year fixed rate was 5.55%. Since then, it has fallen by 0.30 percentage points to its current level. Over the same period, the two-year fixed rate has seen a sharper decline of 0.45 percentage points, down from 5.93% to 5.48%.

The average two-year fixed rate has remained higher than the five-year equivalent since October 2022, a trend that continues as borrowers weigh their options amid a volatile rate environment.

Meanwhile, the average two-year tracker variable mortgage rate edged up to 5.47%. The average “revert to” rate, or standard variable rate (SVR), fell to 7.81%, down from its peak of 8.19% recorded in November and December 2023.

Product availability in the mortgage market improved, with the number of options rising to 6,508 this month, compared to 5,899 a year ago. The average shelf-life of a mortgage product remained steady at 21 days, unchanged from the previous month.

Rachel Springall (pictured), finance expert at Moneyfacts, highlighted the significance of the narrowing rate gap for borrowers.

“Borrowers who prefer to lock into a shorter-term mortgage may be pleased to see that the rate gap between the average two- and five-year fixed mortgage has dropped to its lowest margin in two years,” she said.

Springall noted that as five-year fixed rates remain lower than their two-year counterparts, borrowers may be drawn to the stability offered by a longer-term deal. However, she cautioned that fixed rates could remain volatile in 2025, particularly if inflation persists or swap rates rise.

Lenders, she added, may need to act quickly in response to market changes to attract new business. With millions of borrowers coming off fixed rate deals, remortgage activity is expected to increase significantly this year.

Springall also urged borrowers not to delay refinancing, as falling onto a lender’s revert rate could lead to substantially higher repayments. For example, homeowners coming off a five-year fixed deal from January 2020, when the average rate was 2.74%, would face a much steeper SVR of 7.81% today.

Although market stability has improved since the turmoil following the 2022 fiscal announcement, Springall warned borrowers to remain cautious. Rates may fluctuate, she said, but the widespread withdrawal of mortgage products seen in late 2022 is less likely to repeat.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.