New analysis points to higher refinancing risk if oil prices remain elevated

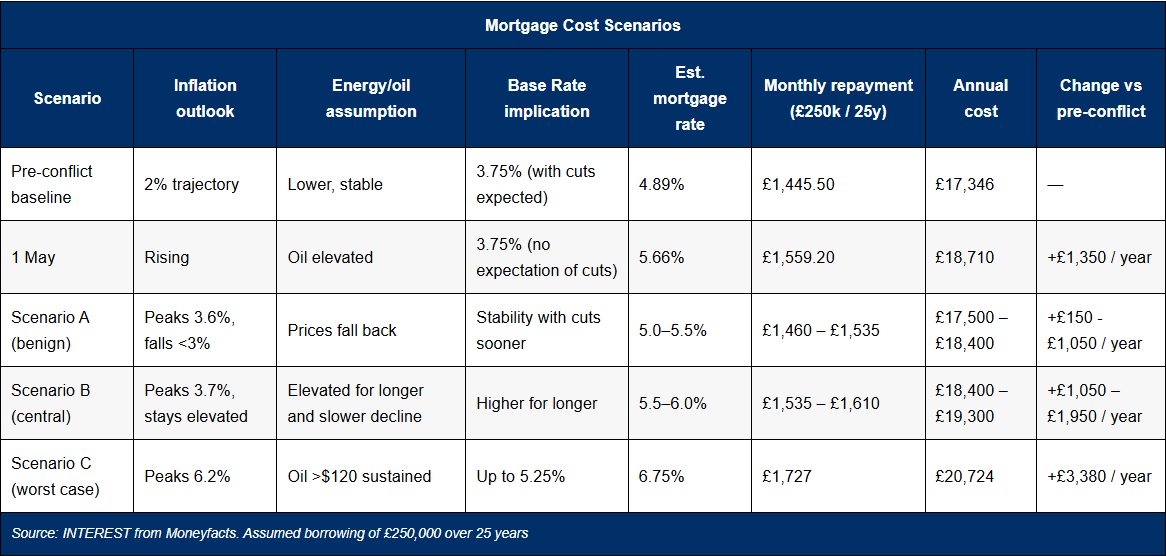

Mortgage borrowers could face annual repayment increases of more than £3,000 if inflation rises sharply and the Bank of England is forced to lift interest rates, according to analysis from INTEREST from Moneyfacts.

The analysis, based on more than three decades of rates data, found that mortgage pricing has typically been about 1.5 to 1.75 percentage points above Bank Rate. Moneyfacts said this relationship could put average mortgage rates above 6.5% in a severe stress scenario.

The assessment follows the Bank of England’s “Trumpflation” stress scenarios, which set out different possible outcomes for inflation and borrowing costs linked to the Iran conflict.

Under the more benign scenario, energy costs would fall quickly, consumer price inflation would peak at 3.6% this year, and drop below 3% next autumn. That outcome would likely bring mortgage rates down sooner.

In the central case, energy prices decline more slowly, inflation rises to 3.7%, and remains higher for longer. Moneyfacts said markets currently view this as the most probable outcome, with mortgage rates broadly steady and only limited upward pressure.

The most severe scenario assumes oil stays above $120 a barrel, inflation reaches 6.2%, and Bank Rate rises to 5.25%. On historic pricing patterns, average mortgage rates could move towards 6.75%.

“The Bank of England’s ‘Trumpflation’ stress scenarios lay bare just how damaging the economic repercussion of the Iran conflict could become,” said Adam French (pictured right), head of consumer finance at Moneyfacts.

“The Bank of England’s ‘Trumpflation’ stress scenarios lay bare just how damaging the economic repercussion of the Iran conflict could become,” said Adam French (pictured right), head of consumer finance at Moneyfacts.

“For borrowers, there are still ways to limit some of the damage. Most lenders allow you to secure a new deal up to six months before your current fixed rate expires, effectively giving you the option to ‘lock in’ today’s rates as insurance. If rates rise, you’re protected and if they fall, you can often switch to a cheaper deal before the new one begins.

“It’s also worth speaking directly to your broker or lender about flexibility options, such as extending the mortgage term to reduce monthly repayments, although this will increase the total interest paid over the lifetime of the loan. In a volatile market, being proactive and keeping options open can make a meaningful difference to borrowing costs.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.