Equifax data links a two-speed credit economy to rising SME mortgage delinquency, with payday super changes adding fresh pressure ahead

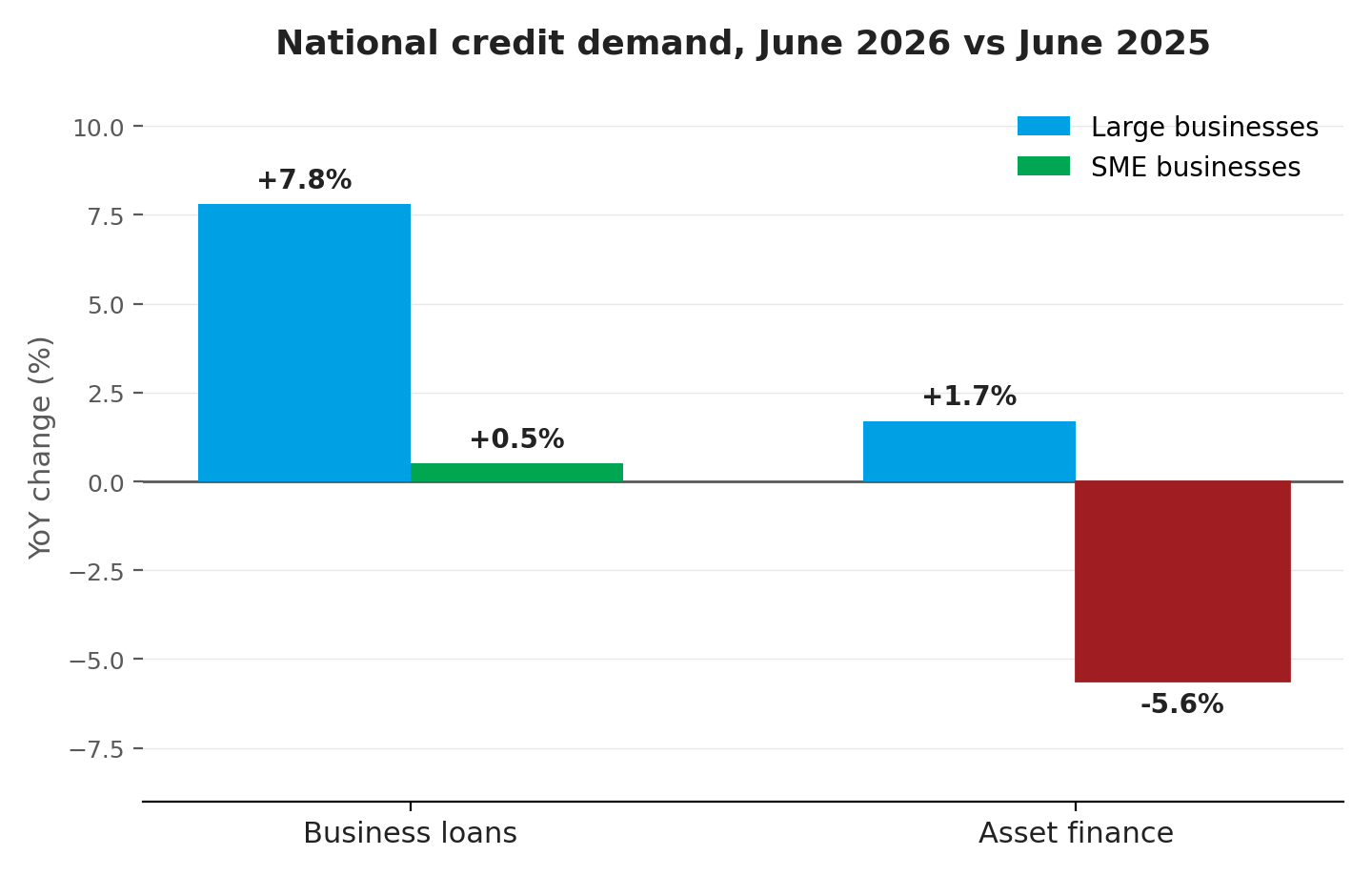

Australia's business credit market split further apart in June, with larger companies continuing to borrow freely while SMEs pulled back sharply on both loans and equipment finance.

The divergence, as noted in the latest Equifax Business Market Pulse, points to a growing cohort of SME owners under financial pressure that could soon show up in loan conversations.

Brad Walters (pictured), general manager of commercial at Equifax, said the headline numbers point to a broader shift in appetite for risk.

“The June Equifax Business Market Pulse shows that the rapid pace of business credit growth we saw late last year has cooled,” Walters said. “After a period of heavy borrowing, possibly to keep up with inflation and rising costs, Australian businesses now appear to be moving into a much more cautious, conservative phase.”

The data suggests large enterprises still have the balance-sheet strength to keep expanding, while smaller operators are pulling back on both fresh borrowing and equipment upgrades.

“Look under the surface and you see a clear and continuing multi-speed economy,” Walters said. “Large enterprises still have the financial runway to borrow and expand. Meanwhile, small businesses have pulled back. Small business owners are actively halting upgrades to machinery and vehicles, possibly to protect immediate cash reserves.”

Source: Equifax Business Credit Demand Data Trends, June 2026

The two-speed pattern is highly pronounced in the services sector – which spans professional, financial and administrative firms – as large operators continue to invest heavily in equipment and technology, while their smaller counterparts have pulled back hard.

“It's likely that while big players are scaling up, possibly to capture market share, small services firms are halting new investments,” Walters said.

Late payments start to bite

The caution isn't limited to borrowing decisions. Equifax's data also points to a build-up in day-to-day payment delays, with more businesses stretching out the time they take to pay suppliers even as severe, long-term defaults have steadied.

Source: Equifax Business Credit Demand Data Trends, June 2026

“We've also been observing what looks like cash preservation starting to cause bottlenecks in day-to-day payment times,” Walters said. “Given the economic environment, this may be a sign that businesses are intentionally taking a bit longer to pay their suppliers as a practical way to manage their weekly cashflow.”

Mortgage stress follows business owners home

Equifax's data shows SME owners are carrying meaningfully larger mortgages than the general population, and are falling behind on those personal repayments more often than non-business-owning borrowers.

The data shows that SME owners are carrying mortgages roughly 50% higher than the general public, averaging $585,000 compared to $379,000. Furthermore, personal mortgage delinquency rates are higher (by four basis points) among SME owners compared to non-SMEs.

“This could be an indication that many small business owners are making tough choices, possibly delaying their own personal mortgage payments to keep their businesses running,” Walters suggested.

The cashflow squeeze

The financial squeeze evident in Equifax's figures echoes a wider pattern playing out among SME owners.

New ATO tax defaults jumped nearly 48% year-on-year in May, a signal that many small businesses are running down working capital simply to cover day-to-day obligations.

That pressure is showing up in sentiment data too. According to the Prospa SME Sentiment Report for May 2026, the share of SMEs confident of staying cashflow positive over the next year fell to 60%, down from 70% in February, with the proportion feeling “very confident” dropping even further.

Brokers on the ground are seeing the same dynamic play out in commercial lending conversations, MPA has reported, with cost pressures on payroll and bills compounding as customers take longer to settle invoices, pushing SME owners to lean harder on working capital and cashflow finance rather than dip into savings.

When a business's cash buffer runs low, the owner's home loan repayment is often one of the few discretionary items left to delay, particularly given SME owners carry higher average mortgages.

Further compliance change could add to the load. From 1 July, employers must now pay superannuation alongside wages under the payday super reform – a change nearly four in 10 SMEs said they were unprepared for.

For businesses already stretching payment terms to preserve cash, more frequent super obligations leave less room to manage short-term shortfalls.

"Payday super is one of the biggest compliance shifts for SMEs in years, and the data shows a lot of businesses still aren't ready," said Roberto Sanz, general manager sales and partnerships at Prospa.

Around one in five SMEs pulled back on investment because of the payday super changes, noted Sanz.