Amid rising costs and compliance pressures, SMEs turn to faster, flexible funding options and full-scope broker advice to protect cash flow resilience

With SMEs making up 97% of all Australian businesses and employing 42% of the national workforce (per official government data), they are often the first to feel the turbulence when the economy hits a stormy patch.

Such is the situation today as business owners weigh headwinds blowing in from both home and abroad.

Amid the geopolitical strife that has muddied the outlook on interest rates, along with wobbly consumer sentiment and tightening lender risk appetites, SMEs are being particularly strategic with their financing needs. This is rapidly reshaping the broker‑SME relationship as the market shifts from a growth mindset to an aware stance – but within this fast‑evolving landscape lies an opportunity for the broking community to truly prove its worth.

“SMEs aren’t just looking for funding; they’re looking for speed, someone to help them through the process and a structure that matches how they actually operate” - Roberto Sanz, Prospa

State of the market

SME credit demand can be best described as “steady overall”, according to Prospa general manager sales and partnerships Roberto Sanz (pictured, left).

While large‑scale purchases aren’t rolling in en masse, they’re in need of more “operational” financing. “We’re seeing many businesses seeking funding to smooth cash flow and stay flexible, rather than borrowing purely to chase growth,” says Sanz.

It’s no secret why this is the running theme of SME finance right now. Cost pressures – chiefly payroll and bills – remain high, and suppliers are taking their time to pay receivables.

“When businesses don’t have large buffers, they seek certainty and access to capital to keep trading with confidence,” says Sanz. “We continue to see strong demand across flexible, revolving funding solutions, which reflects the broader SME need for certainty and adaptability, particularly during busy periods like EOFY [end of financial year].”

These are certainly not new struggles for SMEs, but they are becoming more pronounced in a more demanding macroeconomic environment. Compliance obligations have never been higher for businesses, and interest rates are playing havoc with funding costs. SMEs tend to be at the coalface of these headwinds.

Global economic uncertainty – like the little matter of the US‑Iran war – is also playing a role. “What happens on the world stage continues to impact Australian inflation, and SMEs – the backbone of the economy – often feel that pressure first,” says Sanz.

As they face up to these challenges, SMEs are demanding speed and certainty from their lending partners. Unfortunately, this often comes up against rigid credit settings that don’t align with how small businesses tend to operate.

Anmol Dhingra (pictured, right), director and mortgage broker at WIN Financial Group, says it’s becoming “selectively harder” for SMEs to access funding from the major banks. “Banks are tightening credit appetite and risk models, meaning more SMEs fall outside policy, despite being viable,” he says. Amid increased regulatory pressure and strict capital requirements, their preference is for property‑backed, lower‑risk lending, as opposed to cash flow lending without strong security.

“It’s not that banks don’t want to lend to SMEs, but you have to be clean. Your story needs to make sense,” says Dhingra.

Irregular and seasonal revenue fluctuations – a well‑known bugbear across the entire SME space – can throw up additional hurdles in the application process and lead to unpredictable deal outcomes, especially if a business looks unconventional on paper.

While traditional lenders play a dominant role in providing finance for businesses that match their risk appetite, SMEs are increasingly using non‑bank lenders “because these providers offer the certainty, speed and relevance essential to business continuity”, says Sanz.

“SMEs are seeking solutions that meet their high‑yield needs, combining funding with speed and a service proposition that allows them to maintain control over their financing requirements,” he adds.

The move towards alternative lending options “is one of the biggest shifts I’ve seen in my career”, says Dhingra. “Non‑banks are no longer ‘lenders of last resort’; they’re becoming first choice for many SMEs, especially for short‑term and working capital needs. Faster turnaround times are also a big win with non‑banks.”

Dhingra believes this upheaval of the SME lending landscape is “positive and revolutionary. It will increase competition, which means more products will come into the market to support SMEs. It will also have better pricing”.

But as more lenders pile into the space, the onus is on brokers to properly educate themselves on the funding options at their clients’ disposal. “The more you know the better,” says Dhingra.

Small business cashflow outlook

-

Over a third of SMEs say they can remain cash flow positive over the next 12 months

30% of SMEs only have one month or less of expenses in reserve

14% of SMEs have no reserves at all

70% of SMEs plan to access external finance in the next 12 months (up from 31% in September 2025)

On average, businesses hold 2.7 months of expenses in reserve

Source: Prospa SME Sentiment Report / YouGov SME Sentiment Research (Feb 2026)

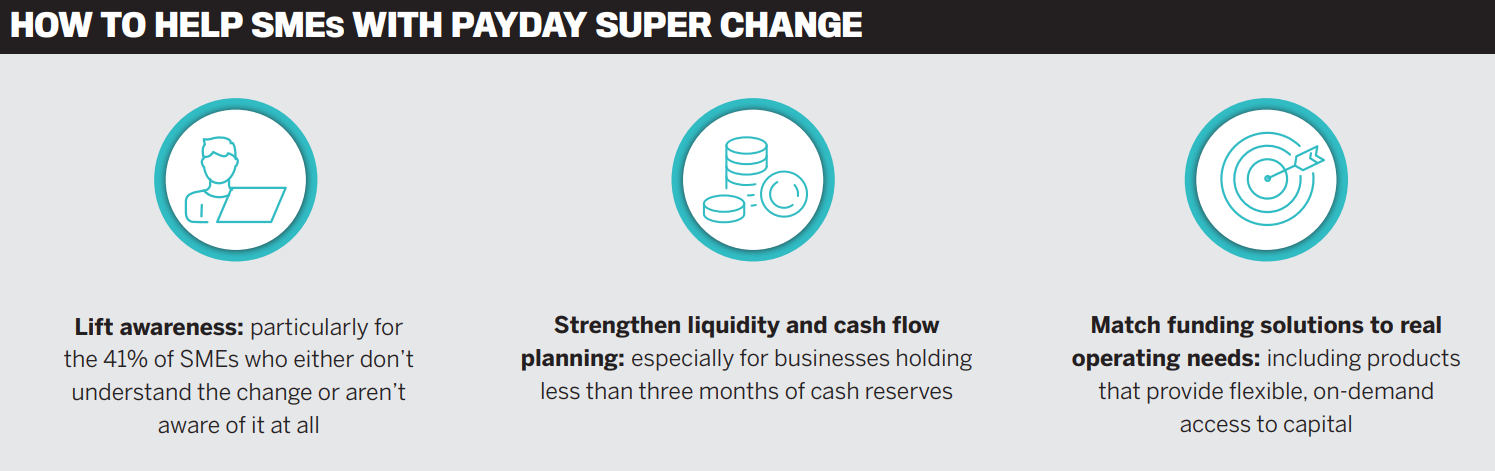

A super warning for SMEs

Payday super is shaping up as the next big compliance crunch for Australia’s small businesses – and a pivotal opportunity for brokers to step in as strategic partners.

From 1 July 2026, employers will need to pay super at the same time as wages rather than quarterly, effectively removing a key short‑term liquidity buffer from SMEs’ cash flow.

While the change may sound incidental, it’s causing a stir in the SME lending community. Many business owners are already grappling with higher costs and softening demand, yet Prospa research shows that nearly a third of SMEs are completely unaware of the change, and a significant cohort are unsure they can meet the new schedule.

With 30% holding one month or less of expenses in reserve and 14% with no reserves at all, the margin for error is thin.

“The compliance changes to payday super will have a massive impact on SMEs’ cash flow,” says Sanz. “For businesses with thin buffers, moving super payments forward compresses working capital. The risk isn’t the rule itself; it’s being caught unprepared and being non‑compliant.”

Sanz emphasises that cash flow planning is going to be key for businesses. “If you don’t have or can’t create the reserves to fund this new change, it’s time to plan a funding line to support your cash flow through this change.”

For brokers, this is a timely trigger to broaden conversations beyond rate and product. Payday super is an obvious entry point to review payroll timing, cash buffers and upcoming obligations, then align flexible funding solutions with real operating needs such as wages, BAS and supplier payments.

As Sanz notes, “The main risk with payday super is not higher costs but the change in payment cadence. It impacts SME cash flow right away by forcing businesses to increase the number of super payments, adding extra pressure on already‑tight cash positions.

“Many SMEs will move from making four super payments a year to paying super every pay cycle, which reduces flexibility and leaves far less margin for error – particularly for businesses with variable payrolls or uneven revenue.

“With cash reserves already low for many SMEs, this makes active cash flow management and access to flexible funding more important than ever.”

“It’s not that banks don’t want to lend to SMEs, but you have to be clean. Your story needs to make sense” - Anmol Dhingra, WIN Financial Group

Beyond the transaction

Whether it’s about payday super, cash flow management or operational matters, brokers continue to play a quintessential role in guiding SME clients through the full spectrum of financing needs.

Dhingra believes brokers should move away from a purely transactional mindset to give clients a more personal touch. “It is not transactional and rate focused any more. It’s more advisory focused where a broker will not just focus on the transaction in hand but on long‑term growth of their clients, which involves funding strategies, cash flow planning and navigating different lender options.”

Because of this shifting broker‑SME dynamic, it’s becoming increasingly important for brokers to work alongside SMEs’ wider professional services partners to effectively coordinate applications.

“A lot of businesses I meet have a great turnover, but they fail to understand that banks rely on what’s left over,” says Dhingra. “I have started involving clients’ accountants more often [it helps that Dhingra comes from an accounting background]. The best brokers are becoming long‑term business advisers, not just deal writers.”

Over the coming months, Sanz expects low cash reserves, global economic conditions and inflationary pressures to reshape how SMEs prepare for the rest of 2026. For many, this is likely to increase demand for cash flow solutions to help them plan for future uncertainty.

“From our side, we expect to continue investing in our partner and customer propositions, enhancing products and services that help SMEs navigate volatility with confidence,” says Sanz. “The focus remains on flexibility, relevance and supporting real‑world business needs.

“Taken together, 2026 is less about chasing big growth and more about resilience, timing and staying in control, with less room for error.”