Freddie Mac economist signals rates could reach 7%

Like the proverbial frog unwittingly relaxing in a pot of slowly boiling water, many have become desensitized to ever-escalating mortgage rates. Thursday offered a reminder of inflation-induced economic heat, as mortgage rates rose for the fourth week in a row.

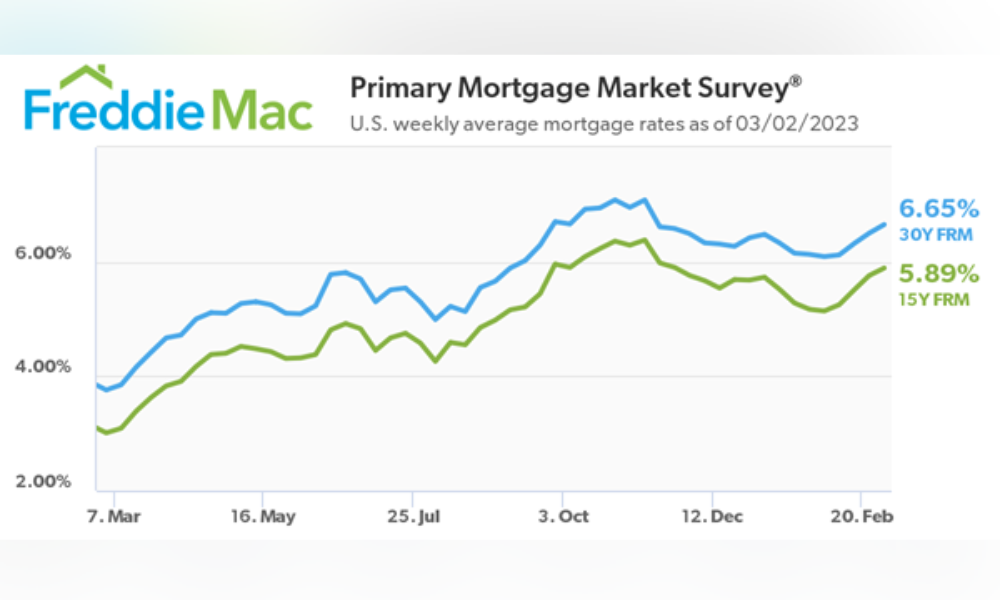

The 30-year fixed-rate mortgage averaged 6.65% in the week ending March 2 – up from 6.5% the prior week, according to data from Freddie Mac contained in the agency’s Primary Mortgage Market Survey. The average mortgage rate is based on mortgage applications Freddie Mac receives from thousands of lenders across the US.

How high will mortgage rates go in 2023?

“As we started the year, the 30-year fixed-rate mortgage decreased with expectations of lower economic growth, inflation and a loosening of monetary policy,” Freddie Mac’s chief economist, Sam Khater, said in a prepared statement. ”However, given sustained economic growth and continued inflation, mortgage rates boomeranged and are inching up toward 7%. Lower mortgage rates back in January brought buyers back into the market. Now that rates are moving up, affordability is hindered and making it difficult for potential buyers to act, particularly for repeat buyers with existing mortgages at less than half of current rates.”

In buttressing the commentary, Freddie Mac issued a pair of “news facts” in the aftermath of the higher rate:

- 30-year fixed-rate mortgage averaged 6.65% as of March 2, 2023, up from last week when it averaged 6.50 percent. A year ago at this time, the 30-year FRM averaged 3.76%.

- 15-year fixed-rate mortgage averaged 5.89%, up from last week when it averaged 5.76%. A year ago at this time, the 15-year FRM averaged 3.01%.

Are mortgage rates rising now?

To be sure, rates that had been on a downward trend after reaching 7.08% in November are now climbing back up. Adding heat to the economic stove, the Fed is expected to continue increasing its benchmark lending rate in its ongoing battle to tame inflation.

While the Fed does not set the interest rates paid by borrowers on their mortgages, the central bank’s moves influence those rates. Mortgage rates typically track the yield on 10-year US Treasury bonds that are susceptible to actions from the Fed. Mortgage rates go up or down as Treasury yields do.

Inevitably, reactions abounded after the latest rate increase.

The Kobeissi Letter - an industry-leading commentary on the global capital markets – broke down the abstraction of rate increases in real terms, noting its impact on a $500,000 mortgage. Interest in that half-a-million-dollar home that would have been $220,000 in May 2021 is now $710,000, according to the site. “In 18 months, mortgage rates have risen from 2.5% to 7.1%,” the Kobeissi Letter noted. “Further, the housing affordability index is officially below 2008 levels. The well overdue housing market correction is on its way.”

Total Interest Paid on a $500,000 Mortgage:

— The Kobeissi Letter (@KobeissiLetter) March 2, 2023

- May 2021: $220,000

- NOW: $710,000

In 18 months, mortgage rates have risen from 2.5% to 7.1%.

Further, the housing affordability index is officially below 2008 levels.

The well overdue housing market correction is on its way.

Indeed, mortgage applications have plummeted amid hikes to the 30-year fixed rate. The Mortgage Bankers Association last month reported a 13.3% decline in mortgage applications as purchase applications fell to their lowest level since 1995.

Genevieve Roch-Decter, CFA, used the example of the impact on a median-priced home at a 7% rate. A down payment on a $467,700 home would require a $93,540 down payment with monthly mortgage payments of $2,514. “Is this doable for the average American?” she asked rhetorically.

Mortgage rates are back above 7%. At that rate, here's what buying a median home in the US looks like:

— Genevieve Roch-Decter, CFA (@GRDecter) March 2, 2023

- $467,700 price

- $93,540 down payment

- $2,514 monthly mortgage payment

Is this doable for the average American?

“No-one is selling real estate and getting rid of a 3% mortgage when interest rates are 7% today,” Andrew Lokenauth of BeFluentInFinance.com observed. “This is called the ‘golden handcuff.’ They are handcuffed to the property (financially tied to property due to low-interest rates), and not selling to keep it.”

No one is selling real estate and getting rid of a 3% mortgage when interest rates are 7% today

— Andrew Lokenauth (@FluentInFinance) March 2, 2023

This is called the "golden handcuff"

They are handcuffed to the property (financially tied to property due to low-interest rates, and not selling to keep it)

Inventory is so low