Is now the time to make a move?

The US housing market continues to offer more breathing room for buyers, with inventory reaching its highest level since the pandemic began, according to Realtor.com’s April 2025 Housing Market Trends Report.

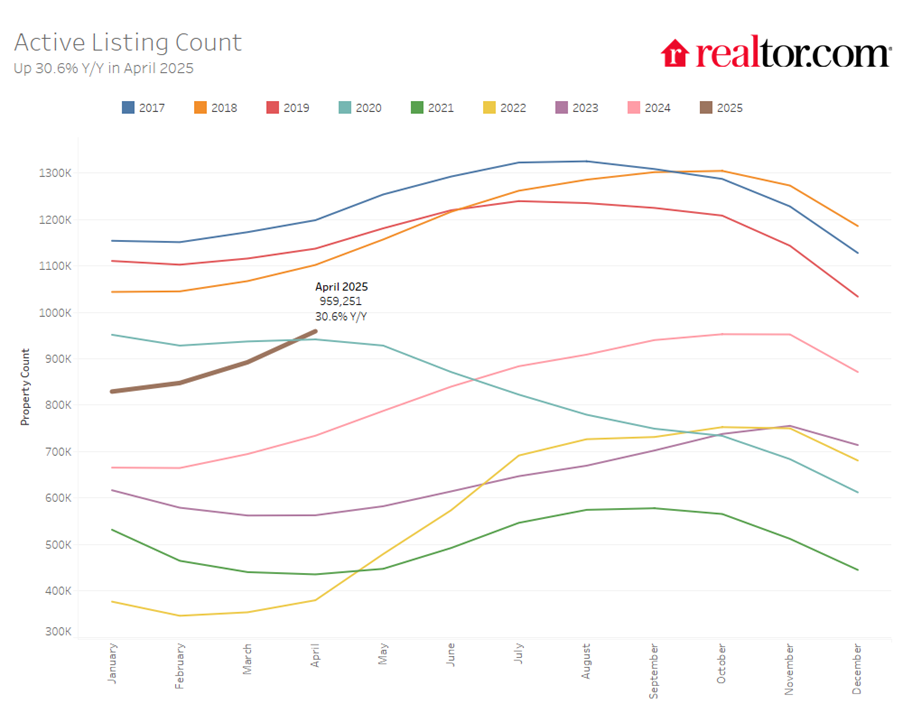

Active listings surged 30.6% compared to last April, marking the 18th consecutive month of inventory growth. For the first time, the number of homes for sale has surpassed April 2020 levels, though inventory still remains 16.3% below pre-pandemic norms.

The data indicates a meaningful rebalancing of the housing market after years of extreme seller advantage, the report noted. Buyers now have more options and slightly more negotiating power than they’ve had in years.

Newly listed homes increased by 9.2% year-over-year, with the strongest growth in Denver (24.7%), Phoenix (22.9%), and Boston (20.1%). However, late-April mortgage rate increases could dampen this positive momentum in the coming months, Realtor.com suggested.

The Western region led inventory growth at 41.7%, followed by the South (33.3%), Midwest (18.7%), and Northeast (12.4%). Major metros seeing the sharpest inventory jumps include San Diego (70.1%), Washington, DC (69.3%), and San Jose (67.6%).

Despite more options, affordability remains a significant challenge. The typical home was priced at $431,250 in April, virtually unchanged from a year ago. But with current mortgage rates, buyers need to earn approximately $114,000 annually to afford the median-priced home—nearly $47,000 more than was required in 2019.

The pressure on buyers is evident in several metrics. Homes spent a median of 50 days on market, four days longer than last year but still five days faster than pre-pandemic norms. Meanwhile, 18% of listings saw price reductions—the highest April figure since at least 2016 and up 2.5 percentage points from last year.

The market is moving toward balance, but hasn’t reached equilibrium yet, according to the report. While sellers are adjusting expectations in many areas, high mortgage rates continue to limit buyer purchasing power.

Regional price patterns varied, with the Northeast showing slight growth (+0.2%) while the South (-0.4%), West (-0.5%), and Midwest (-1.6%) experienced mild declines in median list prices.

The report suggests market dynamics could shift again if mortgage rates continue their upward trend. After briefly easing in March, rates climbed again in April amid uncertainty around government economic policies, potentially slowing both buyer and seller activity in the months ahead.

For now, the housing market appears to be in transition—offering more options for persistent buyers but still presenting significant affordability hurdles that continue to sideline many potential homeowners.

What are your thoughts on the shifting trends? Share your insights below.