Analysts predict a 'higher-for-longer' mortgage rate scenario, influencing home price trends

US home prices continued to rise in March, though the pace of growth continued to decelerate, according to the latest First American Data & Analytics Home Price Index (HPI) report.

From February to March, house prices were up 0.9%, while the year-over-year increase was 6.2%. Prices are now 52% higher compared to pre-pandemic levels in February 2020.

Despite these increases, house prices are starting to see a deceleration as the market adjusts to a period of higher for longer mortgage rates.

First American chief economist Mark Fleming anticipates a further slowdown due to stubborn inflation and the likelihood of sustained high mortgage rates.

“Persistent inflation has diminished any optimism that the Federal Reserve may start to cut rates in June, meaning mortgage rates seem more and more likely to remain ‘higher for longer’ this year,” Fleming said in the report.

Fleming noted that many current homeowners may remain hesitant to sell in this environment, keeping inventory tight.

“However, as we saw last fall when mortgage rates peaked, demand may also wane,” he said. “Even though the supply of homes for sale will remain tight, sagging demand should further slow price appreciation in a ‘higher-for-longer’ mortgage rate environment.”

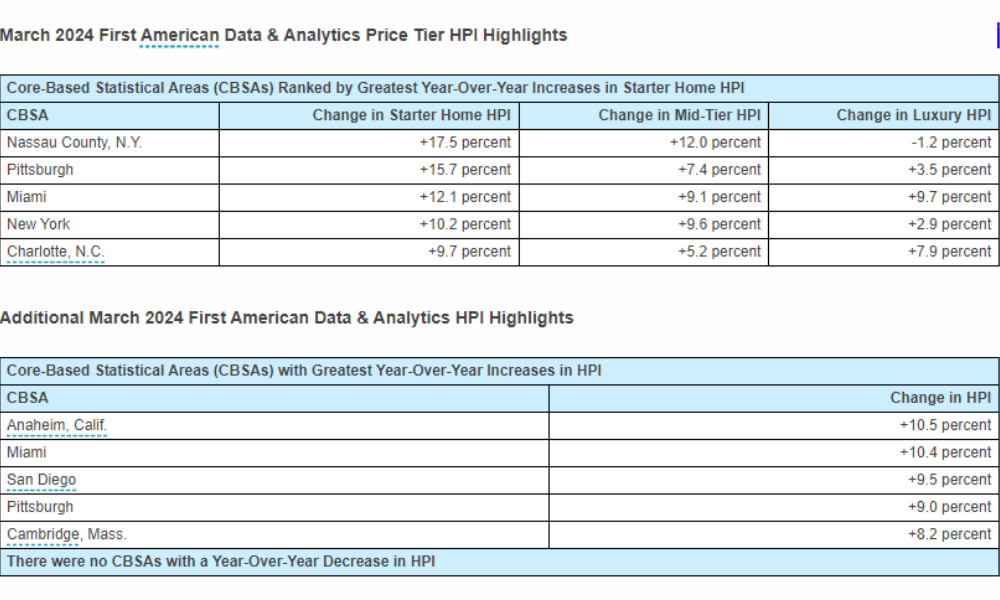

The First American HPI report showed starter home prices, representing the bottom third of the market, continue to face the most upward pressure nationally. Starter-tier prices are increasing by more than 10% year-over-year in several markets, including Nassau County, New York, Pittsburgh, Miami and New York City.

“Nationally, starter home price appreciation will continue to face upward pressure in a ‘higher-for-longer’ market,” said Fleming. “Starter homes are the least supplied because it is the market segment most supplied by existing homeowners, who are the most vulnerable to the rate lock-in effect and thus unable or unwilling to list their home for sale to fuel a move-up purchase.”

Stay updated with the freshest mortgage news. Get exclusive interviews, breaking news, and industry events in your inbox, and always be the first to know by subscribing to our FREE daily newsletter.