Experts weigh in on the impact of inflation on housing costs

Mortgage rates continued to rise this week as inflation remains stubbornly higher than policymakers would like, according to data from Freddie Mac.

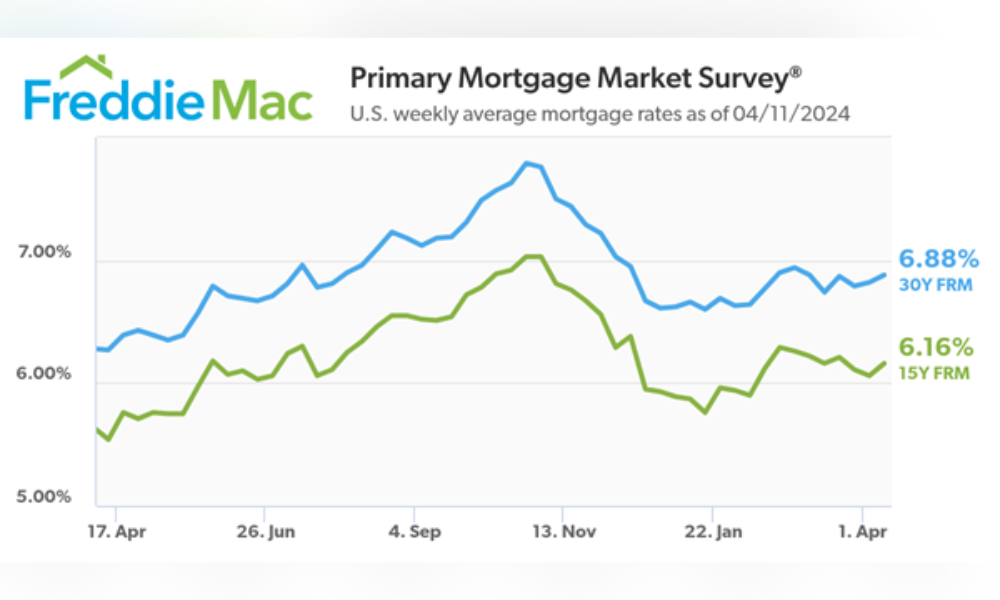

Freddie Mac’s survey revealed that the average rate for a 30-year fixed-rate mortgage rose to 6.88%, up from 6.82% last week. This time last year, the average was 6.27%.

Similarly, the 15-year fixed-rate mortgage averaged 6.16%, an increase from last week’s 6.06% and significantly higher than last year’s average of 5.54%.

“Mortgage rates have been drifting higher for most of the year due to sustained inflation and the re-evaluation of the Federal Reserve’s monetary policy path,” Freddie Mac chief economist Sam Khater explained in the report.

Khater noted that while inflation data has shown a deceleration from 9% to 3% between June 2022 and June 2023, the annual growth rate has remained relatively flat, ranging from 3.1% to 3.7% and averaging 3.3%. The March estimate of 3.5% annual growth is in the middle of that range.

“However, the market’s reaction was dramatically different, as illustrated by a significant drop in the Dow Jones Industrial Average post-announcement,” he said. “It’s clear that while the trend in inflation data has been close to flat for nearly a year, the narrative is much less clear and resembles the unrealized expectations of a recession from a year ago.”

This rising rate environment is causing potential buyers to pause, according to Holden Lewis, home and mortgage expert at NerdWallet.

“Would-be buyers are waiting for mortgage rates to drop before they make offers on homes, which means that the inventory of unsold homes is rising. That gives buyers more homes to choose from,” Lewis said.

Read more: Originators need to be realistic about market prospects - CEO

First American deputy chief economist Odeta Kushi added that the “rate lock-in effect” is weakening homeowner incentives to sell, with nearly 90% of existing homeowners locked into rates below 6%.

“While ‘life happens’ events may spur some buyers and sellers, it’s not enough to fuel the housing market to more normal sales levels,” she said. “To buy a new home, you have to sell the home you already own. The rate lock-in effect will likely weaken if the Federal Reserve cuts rates and mortgage rates fall.”

Kushi said the driving force behind sales activity will remain the five Ds – death, divorce, diplomas, downsizing, and diapers – until the Federal Reserve can cut rates and bring mortgage rates down further.

Stay updated with the freshest mortgage news. Get exclusive interviews, breaking news, and industry events in your inbox, and always be the first to know by subscribing to our FREE daily newsletter.