Help your clients decide if mortgage points are worth it. Learn how points work, how much they cost, and when buying them makes sense in today's market

Buying a home is often one of the biggest financial decisions people make. As such, it’s no surprise that many home buyers look for ways to save money along the way. While securing a competitive mortgage rate is a common strategy, there’s another option that can help your clients reduce their long-term costs: purchasing mortgage points.

In this article, Mortgage Professional America will help you learn all about mortgage points. We will talk about how these points work and whether buying them is a smart move for your clients. Want to know the benefits of purchasing mortgage points and when to buy them? Read on for more.

What are mortgage points?

Mortgage brokers often need to translate complex home loan options into terms that their clients understand. One concept that trips up many borrowers is mortgage points. These are also known as discount points and mortgage buydowns.

Mortgage points are fees that home buyers pay directly to the bank or mortgage lender in exchange for a reduced mortgage interest rate. The process itself is also sometimes referred to as buying down the rate. Every point that your clients purchase costs one percent of the total amount of their loan.

Purchasing points to lower the monthly payments could be a good idea if your clients go for a fixed-rate mortgage. The same is true if they plan to own the property even following the break-even period. This period refers to how long it will take to recoup the cost of purchasing points.

To better understand what mortgage points are, watch this video:

Aside from buying mortgage points, another way to reduce your clients’ mortgage interest rate is by taking advantage of the mortgage interest deduction.

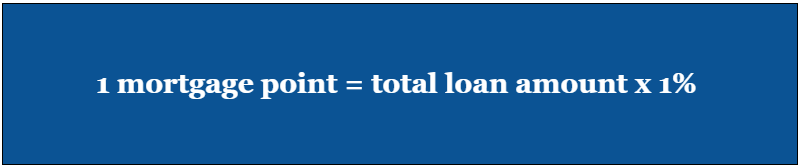

How do points work on a mortgage?

To know how mortgage points work on a mortgage, check out this formula:

For example, let’s say your clients want to know how much 1 mortgage point costs for a $500,000 loan. Using this formula, multiply the total loan cost by 1 percent. So, in this scenario, 1 mortgage point is equal to $5,000.

For every mortgage point that your clients purchase, their interest rate will be reduced by a certain percentage point. While this percentage varies depending on the bank or mortgage lender, a reduction of 0.25 percent in their interest rate per mortgage point purchased is common.

Your clients can buy more than one mortgage point or fractions of a point. They can also buy a half-point, which would be as little as 0.125 percent in interest rate reduction.

When to buy mortgage points

Here are a couple of instances when it would be smart to buy mortgage points:

- your clients plan to remain in the home in the long term

- your clients have figured out when the break-even point is

Why are these two favorable instances for your clients to buy mortgage points? Let’s dive in further below:

1. Your clients plan to remain in the home in the long term

If your clients want to stay in their house for a longer period, they will increase the chances of benefitting from a lower mortgage rate. In that case, it would make sense to purchase mortgage points. This is especially true if your clients are certain to have the same mortgage for a long time.

The longer they have the same home loan, the more they will benefit from mortgage points (or in other words, the more money they will save).

2. Your clients have figured out when the break-even point is

Another favorable instance is when your clients have already calculated when the upfront cost of the mortgage points will be surpassed by the lower mortgage payments. Buying mortgage points could be a good option so long as they do not plan to move or refinance before reaching the break-even point.

To find out the break-even point, use this formula:

Photo alt text (not a caption, so this should not appear on the web page): formula for getting the break-even point when deciding whether to buy mortgage points or not

When not to buy mortgage points

Here are two reasons why it might not make sense for your clients to buy mortgage points:

- your clients plan on moving

- your clients would be sacrificing on their down payment

Here is a more in-depth look at both:

1. Your clients plan on moving

Buying mortgage points is a long-term strategy for reducing mortgage interest rates. As such, your clients will not benefit from this option if they plan to move in the short term. As indicated by the break-even point, it takes time for the savings from lower monthly payments to outweigh the upfront cost of the points.

So, if your clients are planning to move soon, let them know that spending on mortgage points might not be worthwhile.

2. Your clients would be sacrificing on their down payment

“Should I buy points or a bigger down payment?” If your clients ask you this question, tell them that it might be better to spend extra money on a down payment instead of mortgage points. A larger down payment can give them more benefits such as:

- increased equity in the home right from the start

- improved chances of securing a better interest rate

- a smaller loan balance, which means less interest paid over time

- potentially avoiding private mortgage insurance (PMI) if the down payment is 20 percent or more

On the other hand, buying mortgage points doesn’t carry all these perks.

Should clients buy mortgage points if they’re refinancing?

Purchasing mortgage points might seem like a great idea when interest rates are ballooning. However, it might not be a good decision if your clients are planning to refinance soon. If they do, they’ll be forced to pay origination points and discount points again for the new mortgage. This means that they’ll pay the same costs twice.

Is it a good idea to buy mortgage points?

Mortgage points can offer meaningful savings, but only under the right circumstances. For some borrowers, the upfront cost makes sense. This is because they plan to stay in their home long enough to benefit from lower interest payments over time. For others, especially those who are unsure about how long they’ll hold their mortgage, the extra expense might not be worth it.

As a mortgage broker, you must guide your clients in weighing their options based on both short-term cash flow and long-term goals. You’ll need to explain how buying points affects not just monthly payments but also the total cost of the mortgage over its full term. Many borrowers won’t understand the trade-off without your guidance.

In most cases, your clients might just want reassurance that they’re not missing out on a good deal or overpaying where they don’t have to. That’s where your communication skills and mortgage knowledge can make a lasting impact.

Mortgage points are a way to get around the interest rate hikes that your clients might be facing. If their mortgage interest rate is going up a considerable amount, it might be worth looking at using mortgage points to buy down their interest rate.

Do you have clients who are interested in buying mortgage points? What tips would you give them? Let us know in the comments below