Product choice remains below pre-March levels as affordability pressures persist for those with small deposits

Mortgage product availability and rate volatility eased in April, according to Moneyfacts, though conditions for first-time buyers remain difficult.

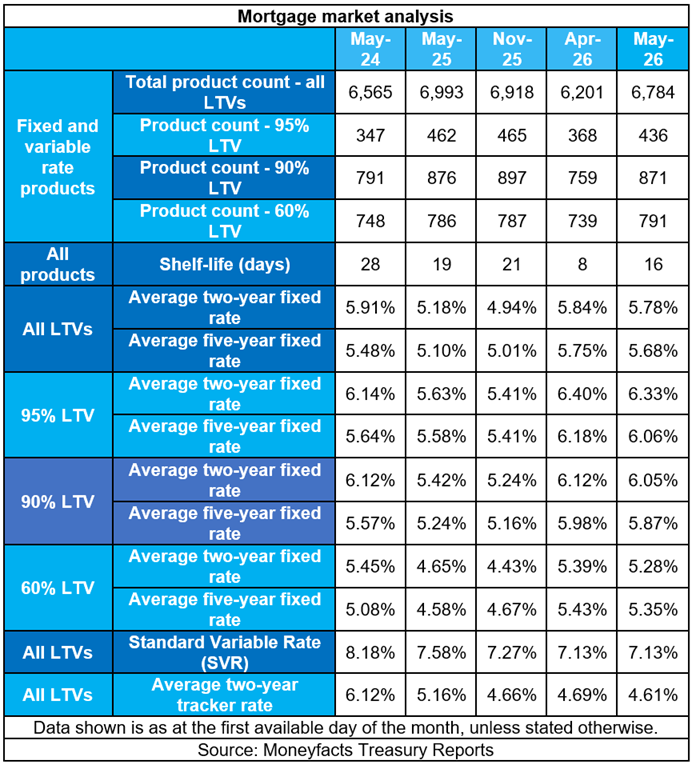

The price comparison website's latest UK Mortgage Trends Treasury Report showed that overall product numbers rose by 583 month-on-month, but this represents fewer than half the 1,283 deals withdrawn the previous month. Since the start of March, total product choice has fallen by around 10%, with higher loan-to-value (LTV) options — those requiring a deposit or equity of 10% or less — down 14%. The contraction reflects lender caution amid uncertainty over the future path of interest rates.

Product churn slowed markedly during April. The average shelf-life of a mortgage deal doubled from eight days to 16 days, indicating greater stability than in March.

Average fixed rates declined slightly over April. The two-year fixed rate fell by 0.06 percentage points to 5.78%, while the five-year equivalent dropped 0.07 percentage points to 5.68%. Both nonetheless remain higher than at the start of March, when they stood at 4.84% and 4.96% respectively. Average two- and five-year fixed rates at 95% LTV remain above 6%.

The average standard variable rate (SVR) stands at 7.13%, down 0.45 percentage points year-on-year from 7.58%, and well below its peak of 8.19% recorded in November and December 2023.

"Borrowers may feel partially relieved by the period of calm after absolute mortgage mayhem, but first-time buyers bear the brunt," said Rachel Springall, finance expert at Moneyfacts.

"Lenders slowly brought back deals and shifted to making cuts over hikes during April. Unfortunately, there is much more room for improvement, as the product choice overall is still down by around 10% since the start of March, as less than half the deals lost have returned. First-time buyers will be frustrated to see the choice of higher loan-to-value (LTV) options drop by 14% since the start of March (90%, 95% and 100% LTV)."

Springall (pictured right) recalled that geopolitical tensions in the Middle East disrupted expectations for both inflation and rate-setting, prompting lenders to withdraw products and raise fixed rates.

Springall (pictured right) recalled that geopolitical tensions in the Middle East disrupted expectations for both inflation and rate-setting, prompting lenders to withdraw products and raise fixed rates.

"Thankfully, the calm of product churn during April compared to the upheaval in March, resulted in the average shelf-life of a deal returning to a more realistic window, doubling from around a week to just over two weeks (eight days to 16 days)," she said.

"First-time buyers or those with little equity of just 5% hoping to grab a two- or five-year fixed deal will find average fixed rates remain above 6%. It is essential that new buyers in particular feel supported, to keep the market moving, but affordability strains are evident."

Springall stressed that higher interest rates, the lack of affordable housing and the potential for a spike in the cost of living can all damage the mortgage market.

"Support and innovation from lenders will be vital to keep the market moving," she said. "The strain of high payments will make borrowers consider a longer-term deal, such as for 35 years or 40 years to make initial payments more manageable. However, this means paying more interest overall, so making overpayments where possible to reduce the debt and mortgage term is wise.

"It is understandable to see why affordability for borrowers continues to be stretched, incomes are not stretching far enough to acquire a mortgage and those trapped in the rental cycle struggle to build a sizeable deposit. Over recent years, there has been a rise in the proportion of borrowers taking on a mortgage with a high loan-to-income ratio (LTI). Official data from the Financial Conduct Authority (FCA) of gross advances by income multiples during Q4 2025 revealed that proportion of lending to a single borrower at four times' income (4x LTI) rose to its highest levels since Q2 2021.

"As may be obvious, securing a mortgage can be more of a challenge for those going alone, which means any relaxation to loan-to-income rules, such as with building societies like Nationwide with its Helping Hand mortgage at six times' income, can make all the difference. Seeking advice from a broker is wise to keep abreast of the latest deals and get invaluable advice on affordability constraints."

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.