Jump to winners | Jump to methodology

The mortgage industry is enduring turbulence, the result of bruising economic conditions. However, Mortgage Introducer’s Top Brokers have thrived in the face of this adversity and delivered exemplary service.

One winner, Rebecca Shuttle, principal owner of MIMA Mortgage and Protection Advice, feels there is a fundamental reason for her recognition.

“Winning is a representation of service. Anyone can sell a product, but I believe being truly successful is shown by the service you provide,” she explains. “I have always done well in helping clients achieve their goals, but it feels really nice to be credited for the job I have accomplished by an external source. I have worked hard every day, so it feels great to get the recognition.”

Fellow winner, Monica Bradley, managing director of MB Associates, believes her success is down to the work ethic of her colleagues. “Everyone in the business is highly motivated to ensure they provide the best possible service for each and every client,” she says. “We go the extra mile for every client and as a result, we often have clients tell us they’d been turned down for a mortgage elsewhere and yet we’ve been able to help them.”

It’s no surprise these service-based approaches have earned recognition, according to Robert Sinclair, chief executive of the Association of Mortgage Intermediaries. He says, "A good broker is one who explains the process to the customer, who stays close to the customer, acts in the customer’s interests, sees themselves as a partner in the process and works hard to make sure that the customer gets the best deal."

“Anyone can sell a product, but I believe being truly successful is shown by the service you provide”

Rebecca Shuttle, MIMA Mortgage and Protection Advice

Part of delivering exemplary service requires brokers to handle 24-hour availability, outlines Lea Karasavvas, board member of the Society of Mortgage Professionals and managing director of Prolific Mortgage Finance.

“As an industry, we need to be aware of burnout and the best way to do this is to ensure that we are all managing the expectations of our clients as best we can to ensure we are not overpromising and underdelivering in a time where service is more important than ever,” he adds.

A sizeable part of outstanding service delivery is dealing with backlogs, likely to be no fault of the client. Research conducted by Mortgage Introducer shows mortgage industry recruitment consultants have seen large delays in conveyancing.

“This means that the gap from lenders making an offer to completion of a property is often five or six months, resulting in a slowing of pipelines,” says Sinclair.

This, coupled with rising interest rates, make it challenging for brokers to keep all parties aligned. For example, Nationwide revealed its recent rate increases with less than a month’s notice.

Neil Standring, mortgage and protection adviser for MB Associates, explains that lenders can announce changes with as little as a few hours in some cases.

“This is why we always ask our clients to have their paperwork ready so that we can respond quickly and secure a competitive rate for them,” he says.

Shuttle is sympathetic to what her fellow brokers must contend with. She points towards rapid rate increases, along with a lack of communication from lenders, and long processing and hold times.

“This is then combined with the market interest rates increasing quickly, so as brokers we are having to try and do everything in double time at the outset, and then lots of chasing to ensure that the lenders are dealing with the processing appropriately,” she adds.

Bradley explains that MB Associates offer an exceptional level of service for its clients to help combat the issues arising from service delays.

“While securing the right mortgage for each client is clearly important, we ensure customers know that they’re in safe hands and reassure them throughout the process,” she says. “We try to take the stress out of the process and ensure that clients are kept updated throughout every stage of their mortgage application.”

To achieve this, MB Associates ensures its mortgage advisers are supported by a highly efficient and dedicated administrative team.

“We offer advice on the benefits of making overpayments on mortgages and remortgaging to save money. We see it as our responsibility to educate clients on being financially savvy,” Bradley adds.

“We go the extra mile for every client and as a result, we often have clients tell us they’d been turned down for a mortgage elsewhere and yet we’ve been able to help them”

Monica Bradley, MB Associates

With backlogs and challenging circumstances faced by brokers, Karasavvas points to the remortgage process as a priority that needs to be addressed earlier than ever before.

“Brokers should be ensuring they are getting in touch with their clients as early as possible to ensure that clients can lockdown on their rates at the earliest opportunity, if they so wish, as each week that passes sees increases in available rates,” he adds.

A similar note of caution is expressed by Sinclair, who says there is a large set of maturing fixed-rate mortgages coming out at the end of 2022. Looking forward to 2023, he estimates the remortgage market, “which usually is around the £200bn level, to [grow to] £270bn”.

Shuttle outlines that brokers should ask clients what they know about interest rates, as well as the current cost-of-living crisis, and then document it.

“As the market is in a period of intense change, it is important that we are recognising what a client wants and needs, as well as what impact this market is having on a client’s personal financial position,” she says.

Barry Webb, chief executive of Mortgage Saving Experts, believes brokers are typically striving to deliver even under pressure.

“I think most brokers work until the early hours to submit applications and book interest rates for their clients to ensure the rate has been secured. That is the most important thing and brokers are doing this,” he says.

“A good broker is one who explains the process to the customer, who stays close to the customer, acts in the customer’s interests, sees themselves as a partner in the process and works hard to make sure that the customer gets the best deal”

Robert Sinclair, Association of Mortgage Intermediaries

According to Sinclair, as the industry endured the pandemic, the broker community adapted quickly to more flexible working arrangements. Webb says that brokers have been fortunate to be in an industry that was extremely busy even during the public health crisis.

In Shuttle’s view, most brokers have embraced the post-COVID world with video calling, which enables them to be more accessible to their clients who they may not otherwise meet face to face.

She believes that brokers should be taking advantage of the technological advancements gained during the pandemic to assist their transactions.

The improvement of technological processes is partly the reason for the rise in mortgage borrowing by a net £11.8bn in March 2021, as reported by the Bank of England. This figure is the strongest increase since records began in 1993.

Nevertheless, Shuttle cautions the industry to never lose the human touch. “Clients need real people with real advice, appropriate to circumstances and requirements. Sometimes, the only way to identify these specific requirements is through a good conversation with a client and this cannot be done via a form being filled out.”

Standring explains that remote working and client meetings on Zoom are now accepted methods of getting the job done.

“We are still very happy to meet clients in person, but some clients now prefer Zoom calls for convenience,” he adds.

“As an industry, we need to be aware of burnout, and the best way to do this is to ensure that we are all managing the expectations of our clients as best we can”

Lea Karasavvas, Prolific Mortgage Finance

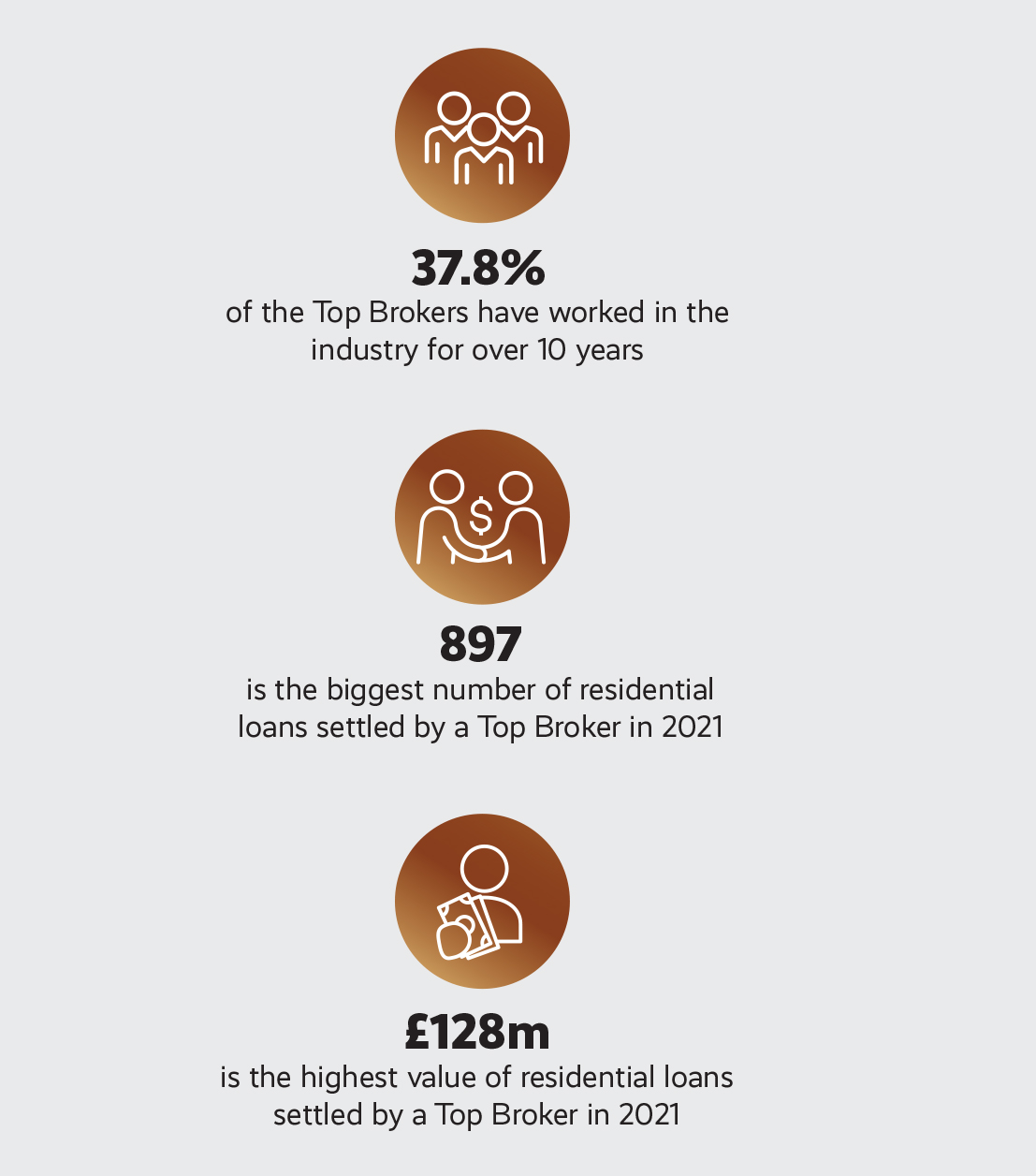

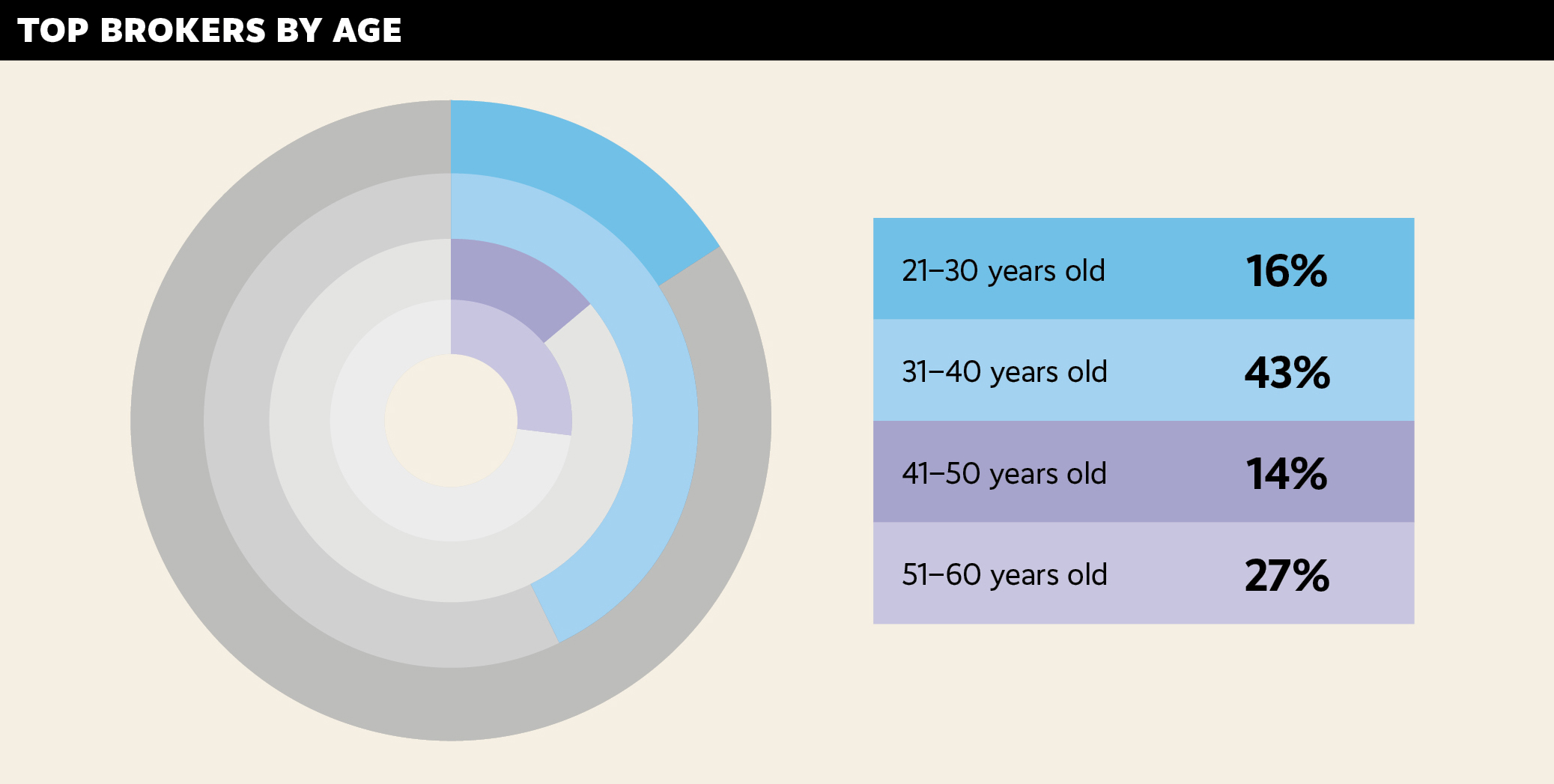

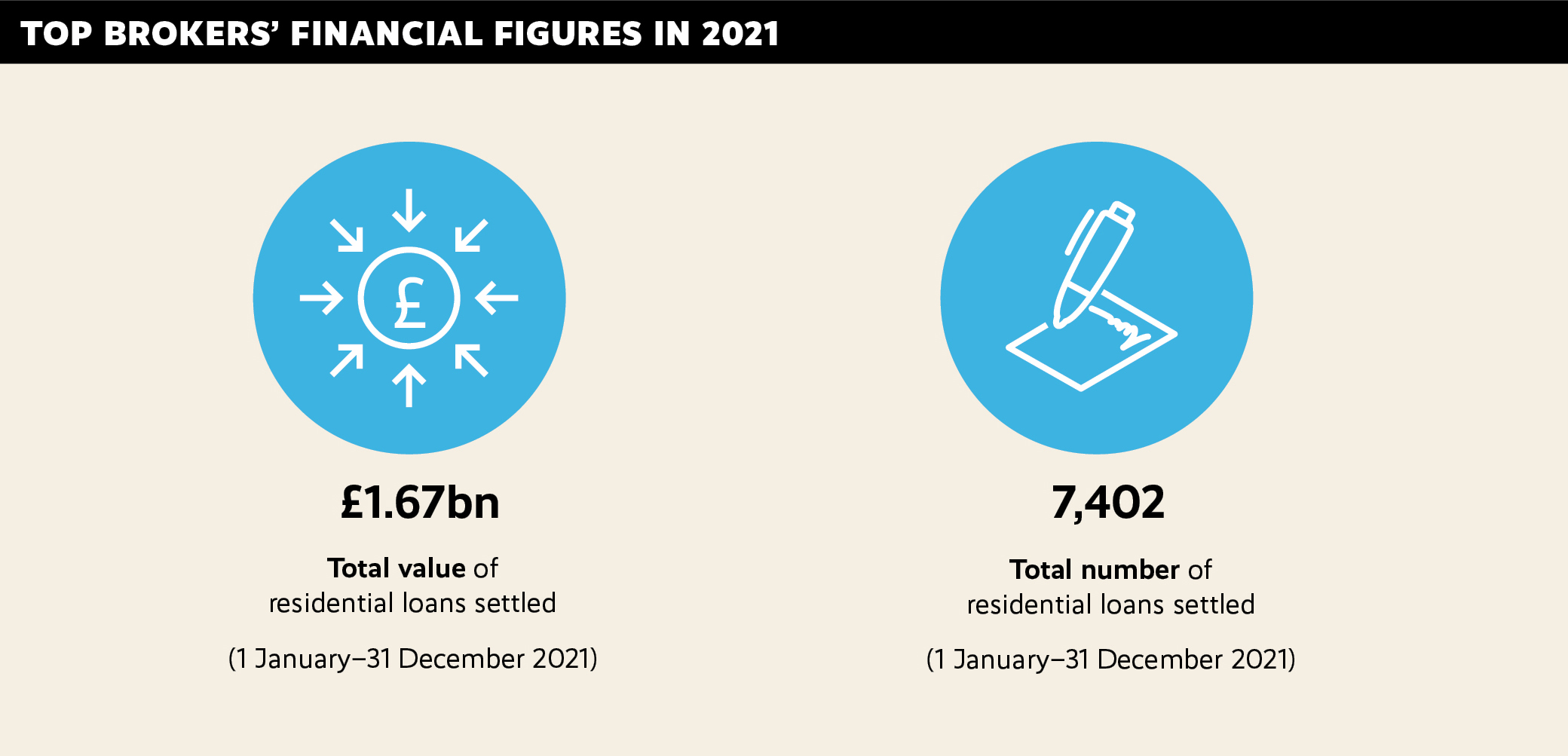

In September, Mortgage Introducer sought to delve into the challenges mortgage brokers are facing during this period of economic uncertainty. Nominees were asked a series of questions relating to this topic, with their feedback developing insights into the mortgage market. Detailed submission forms from the nominees were validated by the in-house research team and used to prepare the shortlist. The Top Brokers were determined and ranked based on the total value of residential loans settled in the 2021 calendar year, as well as the number of loans and rate of year-on-year growth.