When it comes to lenders, brokers have got used to the same old faces – but not for much longer.

‘Competitive’ is perhaps the most misused word in this industry. You generally find it prefixing the terms ‘competitive rates’ or ‘competitive salary’, when the writer wants to disguise the actual figures, which are generally consigned to the small print, if printed at all.

The lenders you see here are actually competitive, in the proper meaning of the word. They have disparate backgrounds; some are mutuals, some are regional banks; all are mindful that as relatively new players they need to impress brokers. That starts with rates – sub-4% variable rates are not unusual in this sector – but also applies to turnaround times and in some cases LVRs.

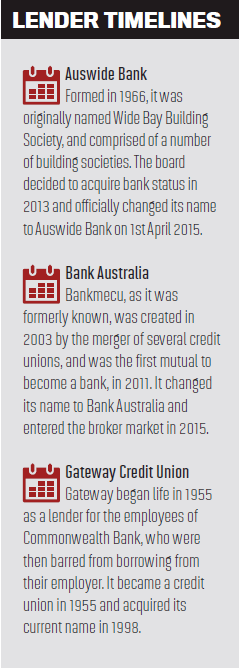

In this feature we’ve gone to three lenders we doubt you’ve dealt with before; Auswide Bank (formerly Wide Bay), Bank Australia (formerly Bankmecu) and Gateway Credit Union. The former two banks underwent rebranding this year and it was also Bank Australia’s first entry into the third party channel. Gateway has been steadily increasing their engagement with the broker channel over the last five years.

However, it’s not simply being new which makes these lenders competitive, but the transformation of the lending environment around them. Wednesday

14th October was a watershed moment in this respect, as Westpac raised their owner-occupier variable interest rates out of cycle. The three other majors followed Westpac’s lead, for the same reasons: increased capital requirements. More surprisingly, so did many of Australia’s non-major banks, preferring increased returns to increased market share.

Two out of the three lenders here are banks, and thus still regulated by APRA, but have gone in a very different direction: holding rates or launching deliberately targeted counter-offers. They know they have a unique opportunity to take market share and here they explain to you, the broker, why they’re

the real competition.

Why are you increasing your engagement with the third party channel now?

Bank Australia:

Up until this point, we had a purely retail distribution model. We have had considerable appetite from brokers wanting access to our competitive suite of home loan products. We are very focused on ensuring that we enter the broker channel in a considered way, as we understand that service and consistency are extremely important.

Gateway:

Gateway has been a strong supporter of the third party channel for over five years now. Instead of taking a big bang approach which comes with some obvious risks, we’ve adopted a progressive growth plan, partnering initially with Yellow Brick Road, bringing on Mortgage Choice in 2012, then Connective in 2013.

In this way we’ve been able to better control growth, volumes and ultimately deliver a more consistent level of service to our partners. It has also given Gateway the opportunity to better understand brokers’ needs. This has allowed us to refine and develop our processes, policies and products to ensure quality of experience and needs satisfaction. There’s a steep learning curve for any lender who is new to the third party channel and we did not want to learn at the expense of our partners. Rather we rolled out partnerships in a controlled way where we could handle the volume and allow our partners to contribute to that knowledge development.

Auswide Bank:

This is the third year of our renewed strategy to create and deliver a market leading third party value proposition to brokers throughout Australia. Over this period Auswide Bank has achieved much in this respect. The product set is fully featured and market leading; pricing is consistently at

the value end of market and brokers have more resources to call on to assist them through the loan process. Our staffing model provides them

with a dedicated relationship manager and once a loan is lodged they deal with a dedicated assessor.

Furthermore the brand has been refreshed due to the conversion from Wide Bay Australia to Auswide Bank. Auswide Bank provides extensive engagement points for customers nationally. Additionally, our loan documentation has been slimmed down for convenience to the customer and

our broker loan processes have been simplified. This means that we are ready for the next three-year phase of our strategic plan.

Are you able to service brokers nationwide?

Auswide Bank:

We are a national business. We have broker relationship managers (BRMs) on the ground in Queensland and New South Wales. Very shortly, we will have on-ground presence in Victoria. We cover the rest of the country with an outbound relationship telephone program (and other means of electronic communications). Our BRM force will continue to grow over the short term as our objective is to deepen our broker partnerships.

Bank Australia:

Yes, we are committed to having an Australiawide distribution footprint and our relationships with brokers are imperative to achieving this outcome. We are in the process of recruiting relationship managers in each state to support brokers on the ground. We are also committed to having a 100% owned Australian operation – with our dedicated assessment team based in regional Victoria. We want brokers to have access to our teams to support quick decision making.

Gateway:

Gateway is nationwide and have three highly experienced BDMs on the ground in New South Wales, Victoria and Queensland. Our back office

team is based in New South Wales.

Which aggregators’ panels are you currently on and do you have plans to expand?

Bank Australia:

We are currently working primarily with AFG, who have been exceptional support to our entry into the broker market. We continue to have discussions with other aggregators with the intention of partnering with another 1-2 over the next 12 months. Demand from brokers who are on other aggregator panels has been high, especially with our attractive interest rates – currently 3.98% for our basic home loan product and with no LVR restrictions.

Auswide Bank:

We are proud to partner with brokers from a very wide range of aggregator panels. These include AFG, Connective, Choice, PLAN, FAST, eChoice, Finsure, Vow, Centrepoint Outsource, Smartline, Custom Equity, Specialist, Ballast. Our focus is very much on growing our connection within each aggregator network. I do anticipate that we will also enter into partnership with further aggregators over 2016.

Gateway:

We’re currently on the panels of Yellow Brick Road, Mortgage Choice and Connective. We are looking to grow in a managed way and are in discussion with

a number of potential partners. We regularly scan and evaluate new opportunities for mutual fit and where we believe we can add significant value to a partner.

Do you compete on rate with major and non-major banks?

Gateway:

We don’t single out any specific competitors on pricing but as a mutual we exist for the sole benefit of our members, not shareholders, so we’re

able to pass back profit and reward members with product that is typically better priced than lenders with different ownership models. This is something we’ve done for 60 years and is at the core of our DNA as a member-owned, member-focused business.

Auswide Bank:

Not only do we compete, we actually blow most of this opposition out of the park. If you compare our pricing over the last couple of years, you’ll notice that we are always in there with a special offer seeking to provide value to customers. An example is our fixed rate with 100% offset. If a customer opts for an average loan of say $400,000, we will offer them a very competitive retail rate. However, consider the savings that are available to them once the offset balance is deducted from the principal loan amount in order to determine the monthly interest charge. Now

convert that to the true interest rate that the customer bears and it demonstrates that we are streets ahead in providing true value!

The basis of our competitive positioning is that we extensively raise retail deposits through our branches and retail offerings. Accordingly our

funding base is deep and stable. We are not overly exposed to wholesale funding. This is a major advantage for us, relative to non-ADI

competitors, and a significant source of peace of mind for our brokers and customers.

Bank Australia:

Yes, we are currently very competitive. Our basic home loan for owner-occupied customers is arguably the best in the market at 3.98% (3.99% comparison rate). There are no LVR restrictions to access our rates, which is unique in a market which seems very focused on risk-based pricing.

Who are your target clients, and what are the products you can offer them?

Auswide:

Auswide targets the key customer segments of owner-occupiers, investors, first home owners and upgraders, and professionals. Auswide’s target geographies are nationwide.

Auswide uses only a premium product suite that is fully featured. Our fixed rate loans with 100% offset have already been discussed. We are also specialists at funding construction loans, and we even apply the fixed rate at the first construction draw as this gives the customers certainty from the outset. We do use these features to stand out from the competition. For first home owners we cap the full LMI to the loan hence we are one of

a few that offer 95%+ full cap LMI.

Bank Australia:

We are currently focused on owner-occupied customers and not offering investment loans on their own. Therefore, the majority of the business we have

been doing has been refinances and first home owners. Given our competitive rates, we have had significant interest from brokers looking to get a better deal for their customers, especially in an environment where the major banks are increasing rates.

Gateway:

We target a number of segments from first time home buyers to seasoned investors. The key for us is to provide products with the flexibility to

cater to borrower needs as they change over time. For example, we offer up to four free variable or fixed rate splits on our package product and can link multiple offset accounts to these, which makes it easier to manage multiple debt and saving strategies from the one loan facility.

Another thing we do differently to most is the fact we don’t credit score; we individually assess each application on its merits and the broker can

talk to and work with the assessor to get a deal over the line.

How can brokers deal with limited consumer awareness of your brands?

Bank Australia:

Bank Australia has been in operation for 50+ years and is the result of 60+ mergers of credit unions, building societies and customer owned banks.

I am not sure I share the sentiment that Bank Australia is not well known. Whilst it is a new brand, it is not a new bank. Bank Australia is customer owned and the mutual structure resonates with customers of brokers – as the concept of doing the best thing by the customers is a shared vision.

Auswide Bank:

Over the years, brokers have been great at helping customers to become comfortable with brands that are not necessarily market dominant (in terms of advertising voice in the market). Our brand is a simple proposition to sell… we’re a Bank… we are listed on the ASX… we are Australian (every aspect of the Bank’s operation is national). The further details that I would like to push out to the broker networks are as follows:

Our current customer base is spread nationally and these customers use one of the largest ATM networks for free. They utilise our very extensive Internet Banking platform and our mobile banking Apps. They can deposit cheques and cash at post offices and agencies. They can reach out to our contact centre for assistance and service.

Our customer satisfaction rate is very strong as a result of a very strong service ethos delivered by Auswide Bank service representatives. This is critical

as brokers can feel very confident that the customers they introduce will enjoy the service environment.

Gateway:

Gateway feels that clients of brokers seek out a broker because they are implicitly open to a better outcome for them, whether that is with a name-brand lender or a lesser known brand. Understanding this, we tackle the opportunity on two levels – firstly we need to get the building blocks right, we’ve got to make sure we have competitive, flexible, feature rich product at the right price. Next we make sure we provide the highest service standards to our brokers and make sure their interactions with us are as simple and easy as possible. In our experience, when we get that right, brokers believe in us and have no problem overcoming any brand awareness objections.

Why else should clients consider you before major banks?

Gateway:

In terms of why a client should consider Gateway, our mutual structure is really important here – being customer owned makes for a model where there’s no conflict between customers and shareholders. Ultimately this means a superior outcome for the customer; first-class value product and exceptional levels of service.

Our smaller size is actually a big advantage. As a broker with Gateway, you can contact our loan assessors directly and you can talk to the person who is assessing your deal all the way through the process. They’ll even call a broker if their application is declined and discuss the reason behind that decision.

Bank Australia:

Bank Australia is owned by its customers, so there is only one master who are also our shareholders – our customers. This is important in making decisions, as there are no conflicts – we only focus on what is the overall best interests of our customers. This can be illustrated at the moment, with the major banks increasing interest rates, which provide a positive outcome for shareholders, but negatively impact their existing home loan customers.

Auswide Bank:

I strongly believe that retail banking consumers want to give the ‘small guys’ a go. Most recognise the pitfalls of a market that is dominated by only a few players. Such pitfalls are evident in a number of essential industries and services that people use every day.

Auswide Bank represents the organisation that is taking the fight to the Big 4. It has for the past 50 years and will do so for the next 50 years.

The lenders you see here are actually competitive, in the proper meaning of the word. They have disparate backgrounds; some are mutuals, some are regional banks; all are mindful that as relatively new players they need to impress brokers. That starts with rates – sub-4% variable rates are not unusual in this sector – but also applies to turnaround times and in some cases LVRs.

In this feature we’ve gone to three lenders we doubt you’ve dealt with before; Auswide Bank (formerly Wide Bay), Bank Australia (formerly Bankmecu) and Gateway Credit Union. The former two banks underwent rebranding this year and it was also Bank Australia’s first entry into the third party channel. Gateway has been steadily increasing their engagement with the broker channel over the last five years.

However, it’s not simply being new which makes these lenders competitive, but the transformation of the lending environment around them. Wednesday

14th October was a watershed moment in this respect, as Westpac raised their owner-occupier variable interest rates out of cycle. The three other majors followed Westpac’s lead, for the same reasons: increased capital requirements. More surprisingly, so did many of Australia’s non-major banks, preferring increased returns to increased market share.

Two out of the three lenders here are banks, and thus still regulated by APRA, but have gone in a very different direction: holding rates or launching deliberately targeted counter-offers. They know they have a unique opportunity to take market share and here they explain to you, the broker, why they’re

the real competition.

Why are you increasing your engagement with the third party channel now?

Bank Australia:

Up until this point, we had a purely retail distribution model. We have had considerable appetite from brokers wanting access to our competitive suite of home loan products. We are very focused on ensuring that we enter the broker channel in a considered way, as we understand that service and consistency are extremely important.

Gateway:

Gateway has been a strong supporter of the third party channel for over five years now. Instead of taking a big bang approach which comes with some obvious risks, we’ve adopted a progressive growth plan, partnering initially with Yellow Brick Road, bringing on Mortgage Choice in 2012, then Connective in 2013.

In this way we’ve been able to better control growth, volumes and ultimately deliver a more consistent level of service to our partners. It has also given Gateway the opportunity to better understand brokers’ needs. This has allowed us to refine and develop our processes, policies and products to ensure quality of experience and needs satisfaction. There’s a steep learning curve for any lender who is new to the third party channel and we did not want to learn at the expense of our partners. Rather we rolled out partnerships in a controlled way where we could handle the volume and allow our partners to contribute to that knowledge development.

Auswide Bank:

This is the third year of our renewed strategy to create and deliver a market leading third party value proposition to brokers throughout Australia. Over this period Auswide Bank has achieved much in this respect. The product set is fully featured and market leading; pricing is consistently at

the value end of market and brokers have more resources to call on to assist them through the loan process. Our staffing model provides them

with a dedicated relationship manager and once a loan is lodged they deal with a dedicated assessor.

Furthermore the brand has been refreshed due to the conversion from Wide Bay Australia to Auswide Bank. Auswide Bank provides extensive engagement points for customers nationally. Additionally, our loan documentation has been slimmed down for convenience to the customer and

our broker loan processes have been simplified. This means that we are ready for the next three-year phase of our strategic plan.

Are you able to service brokers nationwide?

Auswide Bank:

We are a national business. We have broker relationship managers (BRMs) on the ground in Queensland and New South Wales. Very shortly, we will have on-ground presence in Victoria. We cover the rest of the country with an outbound relationship telephone program (and other means of electronic communications). Our BRM force will continue to grow over the short term as our objective is to deepen our broker partnerships.

Bank Australia:

Yes, we are committed to having an Australiawide distribution footprint and our relationships with brokers are imperative to achieving this outcome. We are in the process of recruiting relationship managers in each state to support brokers on the ground. We are also committed to having a 100% owned Australian operation – with our dedicated assessment team based in regional Victoria. We want brokers to have access to our teams to support quick decision making.

Gateway:

Gateway is nationwide and have three highly experienced BDMs on the ground in New South Wales, Victoria and Queensland. Our back office

team is based in New South Wales.

Which aggregators’ panels are you currently on and do you have plans to expand?

Bank Australia:

We are currently working primarily with AFG, who have been exceptional support to our entry into the broker market. We continue to have discussions with other aggregators with the intention of partnering with another 1-2 over the next 12 months. Demand from brokers who are on other aggregator panels has been high, especially with our attractive interest rates – currently 3.98% for our basic home loan product and with no LVR restrictions.

Auswide Bank:

We are proud to partner with brokers from a very wide range of aggregator panels. These include AFG, Connective, Choice, PLAN, FAST, eChoice, Finsure, Vow, Centrepoint Outsource, Smartline, Custom Equity, Specialist, Ballast. Our focus is very much on growing our connection within each aggregator network. I do anticipate that we will also enter into partnership with further aggregators over 2016.

Gateway:

We’re currently on the panels of Yellow Brick Road, Mortgage Choice and Connective. We are looking to grow in a managed way and are in discussion with

a number of potential partners. We regularly scan and evaluate new opportunities for mutual fit and where we believe we can add significant value to a partner.

Do you compete on rate with major and non-major banks?

Gateway:

We don’t single out any specific competitors on pricing but as a mutual we exist for the sole benefit of our members, not shareholders, so we’re

able to pass back profit and reward members with product that is typically better priced than lenders with different ownership models. This is something we’ve done for 60 years and is at the core of our DNA as a member-owned, member-focused business.

Auswide Bank:

Not only do we compete, we actually blow most of this opposition out of the park. If you compare our pricing over the last couple of years, you’ll notice that we are always in there with a special offer seeking to provide value to customers. An example is our fixed rate with 100% offset. If a customer opts for an average loan of say $400,000, we will offer them a very competitive retail rate. However, consider the savings that are available to them once the offset balance is deducted from the principal loan amount in order to determine the monthly interest charge. Now

convert that to the true interest rate that the customer bears and it demonstrates that we are streets ahead in providing true value!

The basis of our competitive positioning is that we extensively raise retail deposits through our branches and retail offerings. Accordingly our

funding base is deep and stable. We are not overly exposed to wholesale funding. This is a major advantage for us, relative to non-ADI

competitors, and a significant source of peace of mind for our brokers and customers.

Bank Australia:

Yes, we are currently very competitive. Our basic home loan for owner-occupied customers is arguably the best in the market at 3.98% (3.99% comparison rate). There are no LVR restrictions to access our rates, which is unique in a market which seems very focused on risk-based pricing.

Who are your target clients, and what are the products you can offer them?

Auswide:

Auswide targets the key customer segments of owner-occupiers, investors, first home owners and upgraders, and professionals. Auswide’s target geographies are nationwide.

Auswide uses only a premium product suite that is fully featured. Our fixed rate loans with 100% offset have already been discussed. We are also specialists at funding construction loans, and we even apply the fixed rate at the first construction draw as this gives the customers certainty from the outset. We do use these features to stand out from the competition. For first home owners we cap the full LMI to the loan hence we are one of

a few that offer 95%+ full cap LMI.

Bank Australia:

We are currently focused on owner-occupied customers and not offering investment loans on their own. Therefore, the majority of the business we have

been doing has been refinances and first home owners. Given our competitive rates, we have had significant interest from brokers looking to get a better deal for their customers, especially in an environment where the major banks are increasing rates.

Gateway:

We target a number of segments from first time home buyers to seasoned investors. The key for us is to provide products with the flexibility to

cater to borrower needs as they change over time. For example, we offer up to four free variable or fixed rate splits on our package product and can link multiple offset accounts to these, which makes it easier to manage multiple debt and saving strategies from the one loan facility.

Another thing we do differently to most is the fact we don’t credit score; we individually assess each application on its merits and the broker can

talk to and work with the assessor to get a deal over the line.

How can brokers deal with limited consumer awareness of your brands?

Bank Australia:

Bank Australia has been in operation for 50+ years and is the result of 60+ mergers of credit unions, building societies and customer owned banks.

I am not sure I share the sentiment that Bank Australia is not well known. Whilst it is a new brand, it is not a new bank. Bank Australia is customer owned and the mutual structure resonates with customers of brokers – as the concept of doing the best thing by the customers is a shared vision.

Auswide Bank:

Over the years, brokers have been great at helping customers to become comfortable with brands that are not necessarily market dominant (in terms of advertising voice in the market). Our brand is a simple proposition to sell… we’re a Bank… we are listed on the ASX… we are Australian (every aspect of the Bank’s operation is national). The further details that I would like to push out to the broker networks are as follows:

Our current customer base is spread nationally and these customers use one of the largest ATM networks for free. They utilise our very extensive Internet Banking platform and our mobile banking Apps. They can deposit cheques and cash at post offices and agencies. They can reach out to our contact centre for assistance and service.

Our customer satisfaction rate is very strong as a result of a very strong service ethos delivered by Auswide Bank service representatives. This is critical

as brokers can feel very confident that the customers they introduce will enjoy the service environment.

Gateway:

Gateway feels that clients of brokers seek out a broker because they are implicitly open to a better outcome for them, whether that is with a name-brand lender or a lesser known brand. Understanding this, we tackle the opportunity on two levels – firstly we need to get the building blocks right, we’ve got to make sure we have competitive, flexible, feature rich product at the right price. Next we make sure we provide the highest service standards to our brokers and make sure their interactions with us are as simple and easy as possible. In our experience, when we get that right, brokers believe in us and have no problem overcoming any brand awareness objections.

Why else should clients consider you before major banks?

Gateway:

In terms of why a client should consider Gateway, our mutual structure is really important here – being customer owned makes for a model where there’s no conflict between customers and shareholders. Ultimately this means a superior outcome for the customer; first-class value product and exceptional levels of service.

Our smaller size is actually a big advantage. As a broker with Gateway, you can contact our loan assessors directly and you can talk to the person who is assessing your deal all the way through the process. They’ll even call a broker if their application is declined and discuss the reason behind that decision.

Bank Australia:

Bank Australia is owned by its customers, so there is only one master who are also our shareholders – our customers. This is important in making decisions, as there are no conflicts – we only focus on what is the overall best interests of our customers. This can be illustrated at the moment, with the major banks increasing interest rates, which provide a positive outcome for shareholders, but negatively impact their existing home loan customers.

Auswide Bank:

I strongly believe that retail banking consumers want to give the ‘small guys’ a go. Most recognise the pitfalls of a market that is dominated by only a few players. Such pitfalls are evident in a number of essential industries and services that people use every day.

Auswide Bank represents the organisation that is taking the fight to the Big 4. It has for the past 50 years and will do so for the next 50 years.