Australia’s second-tier lenders are looking beyond pricing towards innovation, flexibility and human-centric service to win broker loyalty

How are Australia’s second-tier lenders meeting the increasingly complex demands of brokers and borrowers? How are they providing the flexibility and consistency that are more highly sought after than ever?

In times of unprecedented technological change – artificial intelligence, automation, digitisation, to use a few buzzwords – and rising fraud risk, how are these lenders fostering client trust?

As the economic winds blow interest rates higher, what are they doing to separate themselves from the pack, beyond just pricing?

These were just a handful of the compelling themes explored at MPA’s 2026 Non-major Banks Roundtable.

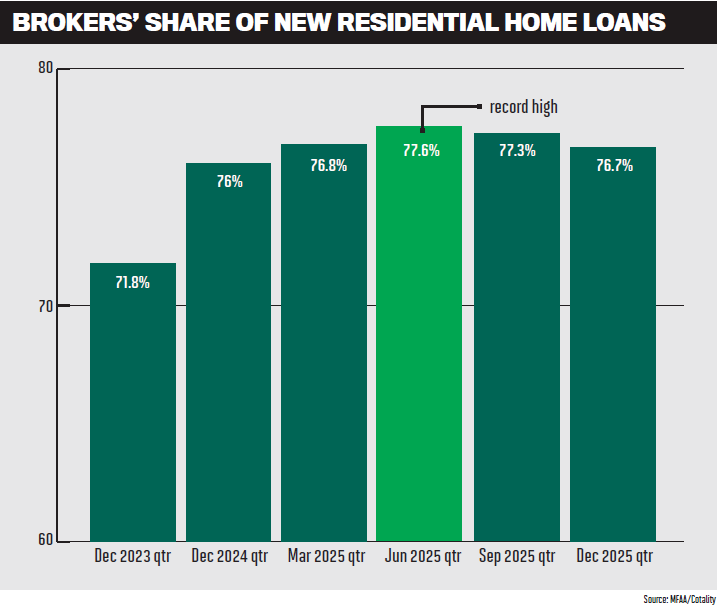

Five representatives from across this dynamic, innovative sector talked candidly about culture, channel conflict, post‑settlement care and the delicate balance between AI-driven efficiency and human support. With brokers now writing the lion’s share of Australian home loans, they stressed that they couldn’t just be another option on a 30‑strong lender panel.

Each panel member –

- Grant Roden, executive manager business support, home buying distribution at Bankwest

- Travis Hall, national manager broker distribution at AMP Bank

- Sergio Delvescovo, national sales manager and acting head of mortgages at ING Australia

- Johnny Lockwood, general manager broker and strategic partnerships at BOQ Group (including broker‑focused brand ME Bank) and

- Shane Davis, acting head of broker partnerships at Suncorp Bank

– had different views on how to go about that, but they aligned on the point that matters most: non-major banks are a crucial component of the Australian financial system, and broker relationships are more important than ever.

Representing the broker voice at the roundtable, Azura Financial’s Avril Clutterbuck and Indigo Finance’s Melanie Cunliffe relished the opportunity to press the banks on topics of utmost importance to the mortgage broking industry.

Here’s what the panellists had to say.

What is your value proposition for brokers, and how are you differentiating yourself in the market beyond just pricing?

ME Bank’s proposition is centred around certainty, capability, and solutions tailored for brokers. “Besides being a strong challenger brand, we’re committed to ensuring you and your customers consistently receive excellent service at every step,” said Lockwood.

Over the past four years, Suncorp Bank has put a lot of effort into creating a consistent experience. “One of the things we get feedback from brokers on is, when they submit a certain transaction to us, they’d like to have a pretty good idea it’s going to be approved from the outset,” said Davis.

Davis noted that brokers have direct access to the bank’s credit team, “so you’re talking to the decision‑maker on a file. That’s been really valuable for brokers in the market.”

Roden outlined the four Ps at Bankwest: people, policy, process and product. “It’s all driven by our people,” he said. “Our BDMs are often ranked right up there, and they’re delivering brilliant policies, fast processing, and we’re looking to offer more solutions for brokers to then offer to their customers.”

“While price remains important, brokers are telling us it’s not the key driver,” Roden added.

Hall said AMP Bank’s focus is on transparency, highlighting its new Simpology‑powered digital platform that lets brokers track applications “from start to finish, which they haven’t previously been able to do”.

This visibility delivers a quicker turnaround time and a clearer understanding of each deal’s progress. Hall noted that 81% of AMP Bank’s documents are issued within 90 seconds of being instructed. “That’s a massive change for AMP Bank,” he said. “That supports brokers to take the customers out of market.”

Ease of doing business, for both brokers and customers, is the name of the game at ING. “For us that means clear policy, simple processes and consistent pricing, service and decision‑making. In my experience, that’s what really delivers value,” said Delvescovo.

ING has been “quite deliberate” in removing friction from the application process, including investing heavily in streamlining and digitising the process. “As broker demand has grown – we had a strong 2025 – we’ve expanded our BDM team across the country and lifted the way we support brokers.”

Broker question from Melanie Cunliffe: In the non-major space, what would be the one thing you’d be most proud of disrupting or transforming, and how would you plan to achieve it?

AMP Bank made the bold move in 2025 of reinventing its broker platform using Simpology. For Hall, this was an important decision that set AMP Bank up for the future of digital integration and broker efficiency, including tackling the scourge of duplication.

“We can continue to be nimble in market, continue to change as brokers give us feedback, and continue to evolve. That’s really important,” said Hall.

That’s all well and good, but Cunliffe reiterated, “What’s the one thing you want to be known for?”

“That would be our digital platform,” Hall replied.

As for Suncorp Bank? It’s looking both forward and backward. On the looking backward front, Davis drew attention to Suncorp Bank’s SunLight automated home loan approval process. Primarily used for low‑risk applications that require less human activity, it’s designed with productivity in mind. “We can get through up to five assessments in the time it takes us to do one traditional assessment,” said Davis. “That produces speed of answer to the broker and also [means] less information that has to be provided up front.”

Looking forward, Davis wants to push this model even further. He sees enormous potential in tapping directly into tax portals and harnessing open banking to remove even more of the manual work currently performed by brokers, customers and bankers. Removing friction, to put it simply.

“We’re focused on making life easier for brokers,” said Delvescovo. “We really want to be seen as the bank of choice for brokers, where the process is redesigned around what helps make them more efficient.”

If ING had a claim to fame, it would be “supporting brokers and helping them manage the full life cycle of a customer, not just a mortgage”, he added.

Lockwood agreed that, because the scale and market share of the broker channel is undeniable, “every lender has to do a really good job at having a great proposition, and it’s really competitive … you’ve got products, platforms – we’re all trying to win in that area”.

But if he could pinpoint one key point of difference for ME Bank, it would be culture. Lockwood said the bank’s strength lies not just in what it offers but in the quality of its people and providing consistent service. Brokers appreciate meeting ME Bank’s BDMs face‑to‑face and developing a great rapport with them, whether that’s at the ME Bank offices or when BDMs are out on the road, meeting brokers in their patch. “Helpful, good people, within a supportive culture is what really matters,” said Lockwood.

It’s a tough question to be lucky last on, but Roden seized the opportunity to say what makes Bankwest different from the crowd.

“Everyone’s chasing speed and efficiency, taking out friction,” he said. “I don’t think that’s anything new; the whole market’s chasing that. What’s equally important is the actual solutions a bank can arm brokers with to help support their customers, whether that’s policy, thinking outside the square in terms of policy, or the digital solutions that we’re coming up with, not only for brokers but for your customers.”

Roden emphasised that customers are a broker’s greatest referral source. “If brokers can offer great solutions for their customers, those customers are more likely to refer them to their friends, and that’s going to enhance their business.”

“While price remains important, brokers are telling us it’s not the key driver” – Grant Roden, Bankwest

On the back of these comments, Cunliffe wanted to know what the banks round the table were doing post‑settlement to support the customer journey.

First to respond, Roden highlighted the enhancements Bankwest is making to its digital banking app. “The onboarding journey is critical,” he said. “We want brokers recommending customers to Bankwest, so we’ve got to onboard them really, really well.”

Delvescovo said automation at ING is about removing friction, not relationships. “We want to be known for supporting brokers through complexity, using technology to make things easier while keeping personalised service where it matters most.”

A question was lobbed back at Cunliffe: Does she think the non‑majors are doing a good enough job of telling brokers what their proposition is and why brokers should pick them over someone else?

Not always, seemed to be the vibe. “I feel I learned some new things today, so maybe that answers the question!” said Cunliffe.

She stressed how important it is to genuinely understand a brand to confidently recommend it to a customer. “As humans we’re very relatable to stories or brands. I wonder how we, as brokers and brands, are connecting, because when we are positioning something with a client, if we’re connected with that brand in a way, that flows on to when we’re talking to the client.”

Hall took the chance to tout AMP Bank’s personalised videos that go out to brokers’ customers. “It’s bespoke to that customer and their individual needs and requirements, and it talks them through the entire formal approval or even the settlement process,” he explained. “The customer now feels that they’re receiving that from you. It mentions you as the broker in the video and is an extension to your business.”

Majors are increasingly targeting proprietary lending. How are you, as non‑majors, taking advantage of this development?

At AMP Bank, where 96% of lending volume comes through the broker channel, “the broker is not a strategy … it’s actually our business model”, said Hall. “Everything that we do evolves around how we consult, how we continue to get feedback from our brokers.”

To that end, AMP Bank conducts roundtables and information sessions, which are particularly important given the bank’s recent platform overhaul. “The reason why we built the platform is to be nimble, to use that information to make the broker’s experience and the customer’s experience better than it was previously,” Hall said.

At ME, Lockwood said, “We’re dedicated to brokers. This isn’t just an extra channel; it’s a key growth driver. We’ve invested heavily in a new platform for brokers and are still allocating resources and hiring staff to support their needs. Our financial commitment speaks for itself.”

With 97% of ING’s production coming through brokers, “it’s clearly at the core of our business”, said Delvescovo. “Since arriving in Australia, we’ve been consistently committed to brokers.”

Customers vote with their feet, noted Delvescovo. When four out of five customers choose a broker for their home loan in Australia, it’s clear where the market is heading.

“For ING, being a broker‑led distribution model creates a huge opportunity for us to grow our market share, and that’s exactly what we’re focused on.”

At Bankwest, over 90% of flow is derived from brokers. “It’s a key channel for us,” said Roden. “We’ve been in broker for three decades now; that hasn’t changed.”

Bankwest’s broker relationships were never more important than when it made the tough decision a few years ago to transform into a fully digital bank. “Part of that decision was to win in broker, and that’s written into our plan,” said Roden. The decision has allowed Bankwest to invest heavily into digital solutions, “not only for brokers but also their customers”, he added.

“It’s about being where your customer is,” continued Davis. And with broker share at over 75% of the residential lending market, partnering with them makes simple, logical sense.

Davis believes there’s room for both the broker and direct channels at Suncorp Bank, and a lot of this comes down to regional footprint. With a strong branch network in Queensland, proprietary lending will remain a core part of that state’s business. In other states where Suncorp Bank’s brick‑and‑mortar footprint is smaller, brokers are critical to growing the brand.

“Over the best part of the last five years, we’ve really doubled down on the broker space, and that’s following customer choice. Customers have chosen brokers,” said Davis. He has seen generational broker businesses develop lifelong relationships with customers that simply cannot be replicated elsewhere.

It was a good opportunity to bring guest broker Avril Clutterbuck into the discussion. As a new‑to‑industry broker of less than a year – and a former banker no less – what does she think of the channel conflict debate?

“For me personally, channel conflict hasn’t been a major issue, but I’d say there are probably some lenders out there – less so the non‑majors – who seem to be saying all the right things about supporting the broker market, but then take a different approach in their internal strategy/allocation of resources,” said Clutterbuck.

Davis stressed how important it is to stop channel conflict in its tracks whenever it emerges. “There are plenty of customers out there,” he said. “We should compete for the customer, but we shouldn’t compete for the channel when the customer has already chosen us via a broker or vice versa.”

“Brokers aren’t just competing with banks; they’re competing with each other,” noted Delvescovo. That competition “keeps brokers honest and focused on delivering genuine value”.

As a non‑major, ING’s priority is simplicity. “We want to make it as easy as possible for brokers to deliver great service and the right advice,” said Delvescovo. “Once customers are on board, we need to service them in a way that caters for their personalised lifestyle, and with the broker still central to provide support where needed.”

Cunliffe stressed that post‑settlement servicing is “really critical” to providing the best customer service.

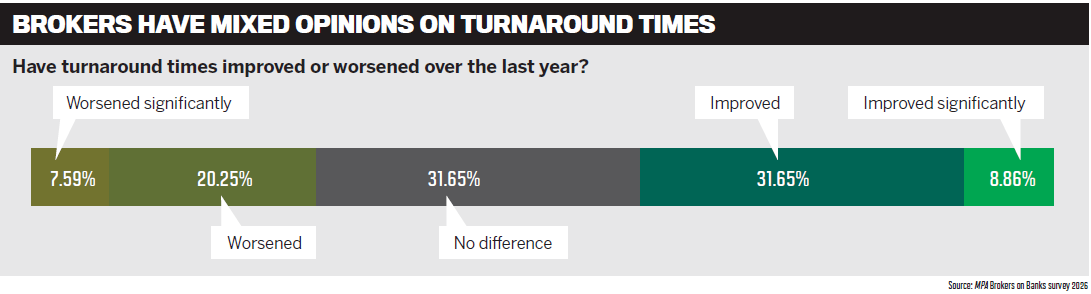

There is a lot of noise around deal consistency and turnaround times. How much of this stems from brokers submitting subpar scenarios or not taking guidance early, and how do you encourage better upfront conversations to improve the submission process?

Roden said he had “a lot of empathy” for brokers trying to navigate panels of 30‑plus lenders, each with their own risk appetite and document requirements. Keeping across that ecosystem, he acknowledged, could be “a nightmare”.

At the same time, he believes lenders must own their part in simplifying the process: being clear about what they ask for and making it easy for brokers to provide the right documents once they have chosen a lender.

Bankwest has and will continue to invest in tools such as its proprietary DocBox – a secure document hub where files land on the application instantly and any missing information requests can be turned around quickly. The bank is also building a digital intuitive checklist that tailors documentation requirements to the specific deal, rather than forcing brokers through a generic list every time.

Roden drew on his own experience as a broker two decades earlier. “I empathise; I’ve been on that side. I started as a broker 20 years ago. A lot’s changed, and it will continue to change, but we need to play our part.”

Hall echoed the message of shared responsibility. Yes, “lenders’ SLAs and turnaround times are only as good as the quality of the application submitted”, but he argued that digital technology is now critical to helping brokers meet those expectations. He said, “Brokers accepting and trusting those systems that lenders are introducing actually makes their lives easier. It’s less documentation they’re required to provide, and it fast‑tracks the system for them.”

Tools such as digital ID verification and digital income verification reduce the documentation burden and accelerate assessment – provided brokers are comfortable adopting and trusting those systems.

Hall noted that AMP Bank has embedded its credit policies directly into its broker platform. At each stage of the process, the system signals whether the scenario is on or off policy, giving brokers clarity and helping them avoid surprises down the track. For him, it’s a partnership: brokers bring quality submissions, and technology plus clear policies make the whole ordeal easier.

Davis agreed that the complexity of lender panels and varied credit policies is real, but in many ways it’s a strength of a competitive market. To support brokers, Suncorp Bank has integrated a dynamic checklist into its ApplyOnline process, guiding brokers through which documents are needed for a given scenario. Davis sees future potential for technology that goes even further, such as scanning payslips to highlight inconsistencies or common issues before submission.

Davis also highlighted the importance of proactive human support, especially for newer brokers. “Having that two‑way conversation between the person assessing the risk and the broker is really powerful in building familiarity. One of the challenges as a non‑major is that brokers don’t always deal with us regularly, so it’s about getting that regular rhythm that helps build knowledge,” he said.

From ING’s perspective, Delvescovo noted that brokers must navigate not one set of policies and systems but dozens. “That’s why we’re building a more intuitive application experience that guides brokers step by step through what’s needed for their specific scenario.”

At the same time, ING has grown its support base so brokers can speak directly to the team when a scenario gets complex, and Delvescovo actively encourages brokers to lean on BDMs to navigate tricky cases quickly.

“While the industry talks a lot about ‘time to yes’, and while we’re focused on that as well, for us it’s about creating a seamless end‑to‑end experience,” he said. “Customers remember the moments that matter. From approval through to settlement and how smooth the journey was. And in areas where speed really counts, like refinances, we’re currently averaging around 10 to 12 days, which makes a big difference to that overall experience.”

In Delvescovo’s view, there is little value in a lightning‑fast approval if the customer is then left waiting weeks to settle.

Clutterbuck said the real test of service often comes with more complex self‑employed clients. “Having the ability to workshop scenarios up front is really important,” she said, as is access to credit experts or even securing a preliminary reference from a credit coach. Some lenders, Clutterbuck noted, already offer credit coaching models that she and her colleagues value highly.

“We see this very much as a shared responsibility,” Lockwood said. “There’s so much for brokers to get across. It doesn’t matter how many awesome tools and self‑serve digital options we offer through the portals, there’s still going to be that need for excellent support on more complex lending. Demand for high‑quality assistance remains, especially regarding complex lending such as self‑employed applicants and negative gearing.”

ME Bank has focused on upskilling its BDMs to support these conversations, while also granting brokers direct access to assessors once deals are submitted. BDMs receive ongoing capability training, which enables them to effectively collaborate with brokers on individual scenarios. “On the policy side, we’ve expanded our capability and our credit appetite by providing more options for self‑employed customers, which now includes wages‑only, one‑year and two‑year financials, giving more flexibility and alternative paths to assessment,” Lockwood said. “You should expect the BDM and assessor support from ME Bank to be pretty up to speed and to stick with you through the process from start to finish,” he added.

If you were sitting in a broker’s chair today with a panel of lenders available and a client expecting certainty and speed, what would make you confidently choose your bank over a competitor?

Hall highlighted AMP Bank’s deliberate emphasis on retirees and pre‑retirees preparing for retirement. “If you have a scenario that is quite in‑depth, we can run that past our senior credit team and give you approval in writing before you submit it. You’ll have the confidence that, as long as you package it up the same way the scenario came in, you’ll have an approval from a credit team,” he said.

Hall also returned to AMP Bank’s Simpology‑powered broker platform, which is evidently a major source of pride for the bank.

Switching to ME Bank, Lockwood said, “We’ve been working hard to broaden our relevance for brokers. For most of what you’re looking for, we can deal with it, but if we can’t, you’ll get a quick no from us.”

ME Bank aims to hit the trifecta of “certainty, speed and reliability”, said Lockwood. “And we can probably cater for 95% of what you’re going to do.”

Roden believes Bankwest provides the most solutions for any customer in terms of its credit policies, including its one‑year self‑employed policy, the market‑leading expat policy, and flexible treatment of bonuses and overtime.

“We’ve consistently been in the top three banks in ‘time to approval’ for the last 12 months,” said Roden, referring to MPA’s Brokers on Banks survey results. “As a broker, you’ve got to have different solutions for different customers. Not every customer is the same; they have different needs, different requirements, and their income is changing. The world is changing with digital, so people are earning income in different ways.”

Behind the scenes, Bankwest’s credit quality managers (CQMs) work alongside BDMs to workshop challenging deals, often providing conditional comfort that, if structured as discussed, a deal can proceed.

For Suncorp Bank, “it’s about target segments,” said Davis. The bank’s approach to self‑employed income assessment is intentionally straightforward, even if it doesn’t offer some of the more flexible one‑year policies that other lenders do. The trade‑off, Davis explained, is a consistent, transparent offering backed by firm turnaround‑time promises: 48 hours to documents for Suncorp Bank SunLight PAYG, and self‑employed transactions assessed using the bank’s basic self‑employed process; five days for most other deals and longer only for the most complex, comprehensive self‑employed cases.

ING has been “broadening our credit policy to expand into new segments because our challenge and opportunity is to become the lender that brokers recommend most often”, said Delvescovo. Brokers only recommend lenders they trust. “They need to know that their customers will be looked after, not just at approval and settlement but post‑settlement as well,” he said.

Flexibility and a common‑sense approach to credit are more important than ever. How are you delivering on these demands?

“Clear and flexible credit policy is critical,” said Delvescovo. “This has been a strong focus for us. We’ve made several policy enhancements and entered new segments.”

ING’s investment lending was enhanced around 18 months ago. It was designed to improve borrowing capacity and has already driven strong growth in investor flows. The bank is now turning its attention to the self‑employed market, where it had a relatively limited presence for close to eight years. Recent enhancements include options for one‑year financials and greater flexibility around ownership structures.

The bank has invested in expanding and upskilling its credit assessment team and is running frequent education webinars to support brokers in navigating complex self‑employed scenarios and better understanding company financials. “For us, it’s about having clear and broad credit policy to cater for more customers,” said Delvescovo.

Davis framed flexibility through the lens of clarity and risk. “We’re very clear about what type of customer we can bank and what type of customer we choose not to. That quick ‘no’ is really valuable. You need to know that an application is not going to meet our risk settings with us.”

Suncorp Bank, explained Davis, uses a strongly risk‑based approach: where clients have strong fundamentals – such as excellent credit history, stable employment and solid equity – there may be room for more flexibility elsewhere in the deal. Where those foundations are missing, the bank is more cautious. The aim is to help brokers understand where Suncorp Bank sits on the risk curve and where it will, as Davis put it, “tap out”.

“There’s no such thing as a vanilla deal,” Lockwood said. “The ideal is a vanilla deal that goes through untouched, but in reality there’s always something that needs to be spoken about at some point.”

ME Bank’s approach is to connect the broker directly with the assessor “so both can walk through the detail together”. The bank has also invested heavily in upskilling BDMs to support this collaborative approach and broadened its product and policy suite to increase its relevance.

“We are focused on increasing our market share,” said Lockwood. “We aim to process more deals by being top of mind and offering flexibility, so brokers see ME Bank as capable of handling a wider range of transactions.”

Under its Built by Brokers program, Bankwest has actively sought feedback from frontline brokers to ensure its policy changes are meaningful and commercially relevant. Policies for self‑employed, bonus income, expats and, soon, high‑LVR lending have all been shaped and refined based on what brokers say they need.

“I think we’re pretty well known for our flexibility and common sense,” said Roden. “Brokers have got such a wide range of customers; we can offer solutions to the majority of them, which gives brokers a great opportunity to recommend us to your customer.”

Bankwest’s CQM team works with BDMs to workshop tricky scenarios and look beyond single data points – for example, a missed repayment – to the full context of a customer’s situation. As the Bankwest mantra goes, “Never say no until you’ve got the full picture.”

Hall stressed that, regardless of how much technology a bank brings into its business, “there still needs to be a commercial decision based on the person’s circumstances. That can’t be removed.”

AMP Bank’s “highly experienced senior credit team” is crucial for delivering the flexibility brokers expect. Hall explained, “We’re continuing to invest in educating and upskilling our other credit teams and making sure they have the right delegated lending authority to make informed decisions. It’s about using the data and documents we have available about the customer’s circumstances to then make a commercial decision on whether it’s fit for AMP Bank as well as the customer.”

“Having the ability to workshop scenarios up front is really important” – Avril Clutterbuck, Azura Financial

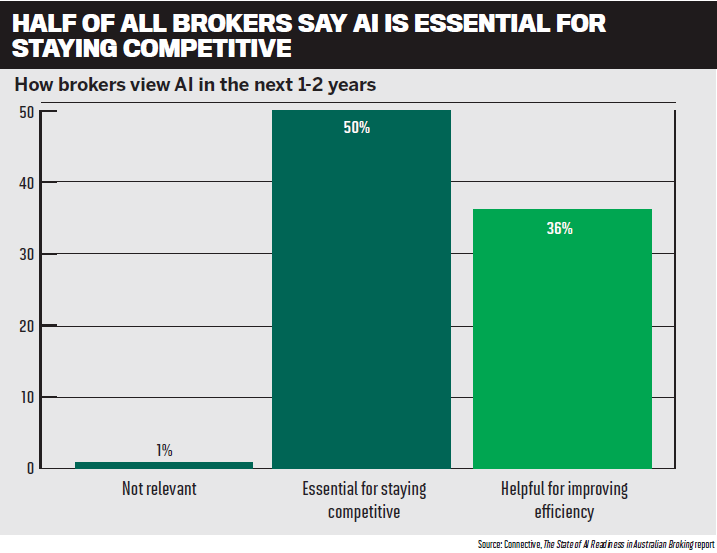

How are you balancing investment in AI and automation with maintaining the human element and support that brokers and customers value?

Hall discussed how important it is for banks to continually invest in AI to create efficiencies within teams, not necessarily to replace humans for the purpose of doing so. “It’s about using data and information as best as possible and using AI to get an outcome that supports human decision‑making and creates efficiencies,” he said.

Roden reinforced that the mortgage industry is “human‑led, built on human interaction”, and he doesn’t see that changing. While people using AI and digital tech will undoubtedly be able to stay ahead of the curve, “the human element is always going to be there”, said Roden.

Bankwest has developed “numerous digital tools” and continues to build more “not just for brokers but for their customers as well”, but Roden stresses that people remain “one of the key pillars to delivering these”.

As for the broker experience, Cunliffe said that “as brokers, we’re always focused on how we can bring in AI and tech so we can have more customer‑facing time”. She worries that with some bank initiatives, “it’s about distancing from us with technology”.

Cunliffe also drew attention to the unintended consequence that, with more tech in play, brokers are now spending a lot of time dealing with tech support. She pressed lenders to explain how they are providing tech support for brokers “to navigate those issues when things go wrong or when the tech doesn’t quite work”, and whether BDMs or lender teams are effectively being positioned to help with the tech support piece.

“It’s a really good question,” Davis responded. “Where it’s on the lender, it often does fall to BDMs to help navigate that. We provide BDMs with the knowledge they need before we launch anything into market so they can support brokers and troubleshoot.”

Clutterbuck recalled numerous instances where lenders had rolled out certain AI advances that had removed the human element a little too much, “and that’s caused a lot of issues”.

“It’s about balancing that and making sure there is still a human touch to deal with that transition,” said Clutterbuck.

At ME Bank, “we are digitally enabled, relationship‑led”, said Lockwood, in one of the best soundbites of the day. “We’re invested heavily in a new platform with tools available for brokers. We’ll utilise industry technologies that are out there to provide familiarity for brokers, but we’ll also look to innovate and make things very simple.”

When dealing with ME Bank, “you’re always going to have the BDM there, you’re always going to have the assessor there”, Lockwood continued. He agreed that new product launches can be difficult for brokers. To combat this, “our BDMs have a hypercare channel which facilitates direct communication to the platform and program teams for rapid identification and resolution of any issues. We make sure we’re plugged in through brokers and the sales team.”

Delvescovo encapsulated ING’s approach succinctly: “Our view is simple – technology should remove friction, not relationships. Our goal is to utilise technology to support a more efficient process but ensure we keep personalised service every step of the way, particularly where there’s complexity.”

Complex scenarios are where brokers value that support and personal service most, Delvescovo explained. “AI and automation have made processes more efficient for both brokers and for us, but the personalised service stays, especially when things get complex. Ultimately, we want to help brokers write more business and help ourselves write more business.”

Rounding off the question, Cunliffe reminded the roundtable that it’s not just about how fast lenders are when everything goes smoothly, but how quickly they can resolve issues when something goes wrong.

“We’re always focused on how we can bring in AI and tech so that we can have more customer‑facing time” – Melanie Cunliffe, Indigo Finance

Competition is good for consumers. What is your role in promoting competition in the Australian mortgage market?

Roden said you “can never control what anybody else does”, so Bankwest’s focus is on what it can influence: “We’ve just got to continue to offer more solutions, continue challenging processes and getting more efficient.” As long as the bank keeps lifting its own game, he believes “competition stays strong within the market”, giving brokers and customers more genuine choice.

“It’s a bit of a catchphrase, but we’re customer‑centric,” said Davis. “We’re always asking what’s the best we can do for our customer. That’s the best form of competition if everyone is thinking that way – providing value to customers.”

“Competition is totally healthy,” added Lockwood. “We’re a challenger brand, so we can’t just sit there and wait for business to come rolling in. We’ve got to try harder than some of the big five. For us, that means continuing to innovate and invest, not just in platforms but in people as well.”

For Lockwood, “it’s great being a challenger because you can do things a little differently, but you’ve got to work pretty hard, and we’re going to continue to do that”.

Hall sees AMP Bank’s role as a challenger as helping “raise the bar” for everyone. “As a challenger bank with a strong desire to continue to innovate, I think that’s important for everyone because it promotes others to continue to raise the bar,” he said.

Whether AMP Bank or another player is “setting the benchmark high, we’ve got something to strive towards”. In his view, the ultimate winners are “brokers and customers”, which is why he strongly supports “continuing to innovate as a challenger bank”.

Bringing the day’s discussion to a close, Delvescovo shared his view: “Non‑majors play a critical role in ensuring brokers can deliver fair value to customers. That’s not just on price but on policy, service and core execution. That’s what delivers value to customers.

“ING’s growth ambitions combined with our commitment to the broker channel drive competition in the market. The fact that we want to grow, and that customers choose brokers four out of five times, shows we’re contributing to a more competitive market where customers get better value.”