Analysts flag tightening bias among Monetary Policy Board, warn rate pause may not last

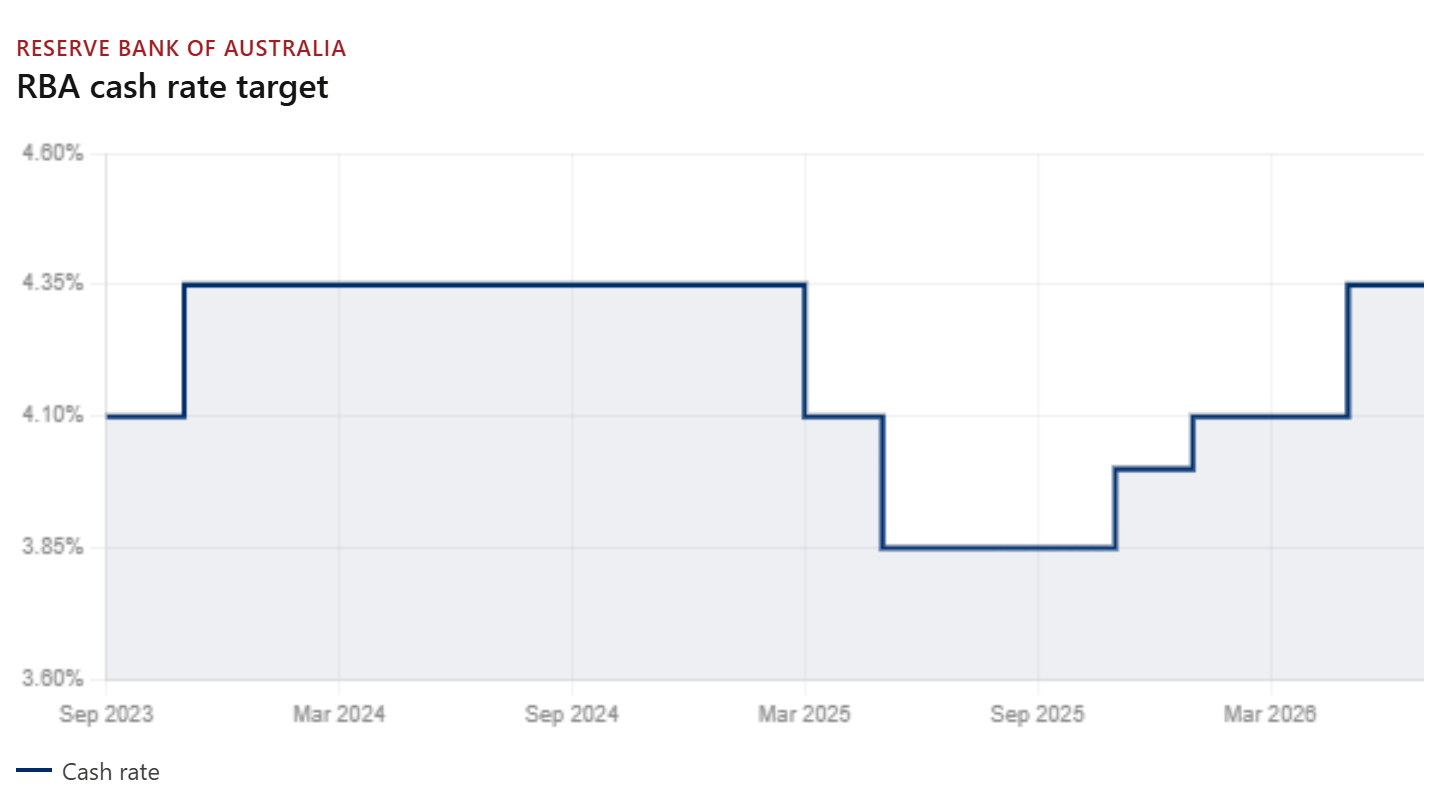

The Reserve Bank of Australia (RBA) may have left the official cash rate on hold at 4.35%, pausing after three consecutive increases this year, but the unanimous decision carried an unmistakable tightening bias.

In making the decision, the Monetary Policy Board acknowledged signs of economic slowing – easing consumer spending, falling house prices in some capital cities, and a higher-than-expected April unemployment rate – yet made clear that inflation remains the dominant concern.

The Board noted that "headline and underlying inflation are still too high" and that higher oil prices from the Middle East conflict are flowing through to the cost of goods and services more broadly.

Crucially, the statement left the door open for further hikes, with the Board saying it "will do what it considers necessary to achieve that outcome, including increasing the cash rate target further if required".

At a press conference, RBA governor Michele Bullock laid out the stakes: "Unless we get inflation down, ultimately that won't be good for the jobs market because if inflation rises, we'll have to raise interest rates… ultimately that will be bad for the jobs market."

Bullock also made a point she said was insufficiently understood: Bringing inflation down does not mean the price level comes down. “We have got permanently higher prices for everything because of the inflation that we've experienced in the past."

Analysts see further hikes ahead

Shane Oliver, chief economist at AMP, said there was a clear tightening bias in the decision. “We continue to expect a further rise in rates," he said, noting that the RBA's statement retained all its hawkish language while omitting any reference to rate cuts.

Oliver flagged several factors underpinning that view: trimmed mean inflation rose to 3.4% year-on-year in April and appears on track to hit 3.8% year-on-year by the end of the current quarter.

The Fair Work Commission's granting of a 4.75% increase in award wages and a 6% increase in the minimum wage from July – affecting approximately 21% of the workforce – points to an acceleration in cost pressures. Combined with Federal spending locked in near 27% of gross domestic product (well above pre-pandemic norms), this does little to ease inflationary demand.

Oliver has pencilled in a further rate hike in August and another in November, with rate cuts not expected until the second half of 2027.

Adam Boynton, head of Australian economics at ANZ, described the post-meeting statement as reading "on the hawkish side" and noted that all nine members of the RBA's Monetary Policy Board voted in favour of the hold.

Boynton added that for August, "the risk of a rate hike is not trivial, with the Q2 trimmed mean particularly important for the Board”.

Is time nigh to refi?

For mortgage brokers, the hold creates a moment of opportunity rather than relief. Anthony Waldron (pictured, top image, right), chief executive of Mortgage Choice in Australia, said borrowers were already responding to the rate environment, with Mortgage Choice home loan submission data showing refinance submissions up 3% year-on-year.

"With the end of financial year just weeks away, it's a timely reminder to review your home loan," Waldron said. "An annual check-in with a mortgage broker can help you understand whether your home loan is still competitive, and whether it might be worth refinancing to access a better deal."

Joseph Daoud (pictured, top image, centre), founder of It's Simple Finance, said borrower confidence has already taken a significant hit, regardless of the latest rate decision. "People are really sitting tight, holding their money together and just praying for dear life to see what's going to happen next,” he said.

Today’s hold was “a very wise decision”, said Daoud. “I think (Bullock’s) doing the best that she can with what she's got," he said, adding that borrowing capacities had already been significantly reduced by the three consecutive hikes earlier in 2026.

Daoud added that the refinance market is absorbing much of that anxiety, with borrowers focused on cutting repayments rather than growing wealth. "People are really just refinancing to save as much money as possible and not really doing much else. The banks are happy to pass those increases along. But if an individual isn't kicking and screaming, they might not have the lowest rate on the market."

Anja Pannek (pictured, top image, left), chief executive of the Mortgage & Finance Association of Australia (MFAA), noted that lender competition remains robust despite the unchanged rate. "While the cash rate has remained unchanged, competition among lenders remains strong and there may still be opportunities for borrowers to secure a better outcome through refinancing or repricing," she said.

Brokers to the front

Mark Haron (pictured, below), executive director of mortgage aggregator Connective, cautioned against reading the pause as the beginning of the end. "This isn't a turning point for borrowers. It's another step in a prolonged adjustment period," he said, adding that across Connective's broker network, clients were becoming "more focused on planning ahead and making informed long-term financial decisions, rather than simply reacting to rate movements”.

Whether the next move is a hike or an eventual cut, the path between now and then is a complex one, shaped by global oil supply disruptions, Federal Budget policy, wage growth, and the lingering weight of three rate increases already absorbed this year.

In that environment, the broker's role as a trusted navigator – helping clients understand their options, model their circumstances, and access competitive products – has rarely mattered more.

As Pannek put it: "More than four in five Australians now choose a mortgage and finance broker when arranging a home loan because brokers provide choice, competition and personalised guidance.

“This is a good time for borrowers to speak with their mortgage and finance broker about their current lending arrangements and future plans, whether they are buying their first home, refinancing, investing in property or simply seeking a better deal.”

“Mortgage and finance brokers are committed to acting in their clients' best interests and helping Australians achieve their property and financial goals regardless of the interest rate environment.”