The customer owned banks saw a huge boost after the Hayne Royal Commission. One year on and their market share is growing as customers continue to see their value

The customer owned banks saw a huge boost after the Hayne Royal Commission. One year on and their market share is growing as customers continue to see their value

Last year this feature’s headline declared that customer-owned banks were the industry’s “best kept secret”, but as these banks have continued to see success over the past 12 months, the secret might be coming out.

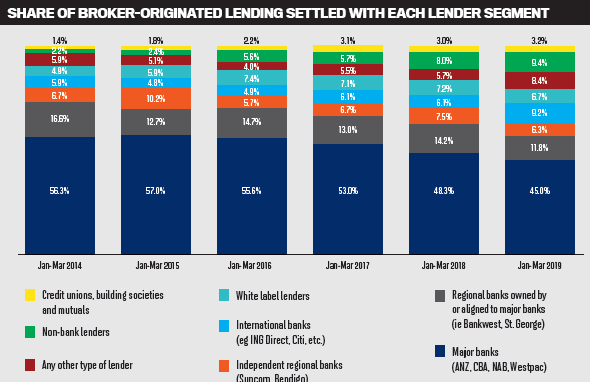

Although there was a slight dip in the early months of 2019, the mutual banks’ market share has grown to more than 3% of broker business since the royal commission began. The sector’s growth has corresponded to a drop in loans settled with the major banks, as well as regional banks aligned to the majors.

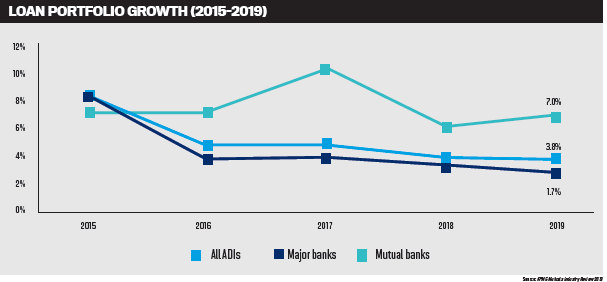

On top of this, an independent report by KPMG has demonstrated that mutual banks, credit unions and building societies managed to grow their residential lending by 7.3% and customer deposits by 8.5% in 2019. The report noted that this was down to their increased investment in both people andt echnology to meet customers’ needs. Read more about these investments over the following pages.

On top of this, an independent report by KPMG has demonstrated that mutual banks, credit unions and building societies managed to grow their residential lending by 7.3% and customer deposits by 8.5% in 2019. The report noted that this was down to their increased investment in both people andt echnology to meet customers’ needs. Read more about these investments over the following pages.

In January, MPA held a roundtable discussion with four customer-owned banks: Heritage Bank, Beyond Bank, Teachers Mutual Bank Limited and Bank Australia. We were also joined by two brokers who use mutual banks for their clients’ business: Christopher Lee and David Merison.

As brokers such as these struggle with the greater scrutiny that has following the royal commission, customer-owned banks are stepping up to the plate, providing a service that highlights the value of human interaction. With questions around living expenses forcing a heavier workload on brokers, this personal touch can be vital.

During the roundtable, which took place at Otto restaurant in Sydney, the group discussed the unique value proposition that customer-owned banks o ffer, particularly with the lack of shareholders they have to cater for. While other banks may have to worry about driving a profit , customer owned banks work for their customers.

Thank you to the representatives of the customer-owned banks who took part in MPA’s roundtable. It is always great to speak to those within these organisations about how they are working with brokers. Thank you also to the brokers who took time out of their day to take partin the discussion. Read more about what they allhad to say in the pages ahead.

Q: A recent KPMG report showed that customer owned banks grew their residential lending in the past year – why do you think this is?

The customer owned banking sector has continued to grow over recent years, particularly as borrowers and brokers look for alternatives to the major and second-tier banks. Released in November, the KPMG Mutuals Industry Review 2019 found that mutual banks, credit unions and building societies grew their residential lending by 7.3% in the year previously.

Taking the lead in answering this first question, Stewart Saunders, head of broker distribution at Heritage Bank, said the royal commission had been a key driver in the increase the mutuals has seen as customers look elsewhere.

“The value proposition that mutual banks provide is getting some more attention,” he said. “We’ve known for a long time that the customer satisfaction that members get through mutual organisations is very high compared to major banks. I think we’ve struggled converting that into member growth, but more recently with it being so front of mind with customers it’s definitely starting to grow.”

With the growth in the sector comes the mutuals banks’ “time to shine”, said head of third party bank at Beyond Bank Darren McLeod, adding that the sector has worked hard over the last two years selling its proposition.

He referenced the roundtable in 2019, where the catchphrase of the day called the customer owned banking sector the ‘best kept secret’: “I think that secret is finally getting out,” he said.

“I don’t think we’re doing anything different,” he added. “We’re doing what we’ve always done but there’s more customer uptake because the market’s in a place where people are now looking and they’re willing to try it.”

Agreeing the royal commission has had an effect on consumers heading to the mutual banks, head of third party at Teachers Mutual Bank, Mark Middleton, said there was a building groundswell. Not only are borrowers looking for alternative options, but aggregators are adding more choice to their panels, he said.

But adding a different perspective, Middleton said consumers were becoming more aware of responsible lending and social responsibilities and asking about things like climate change. Teachers Mutual is not only carbon neutral, but it gives back around 7% of its profits to community grants and other projects.

“It’s particularly very topical right now with the bushfires happening around the country, that people will start looking for who is doing things to make a difference, to not just this generation but future generations,” Middleton said. “I think we’ve been actually ahead of the curve, no one’s been really aware of it, but the last 12 months it’s becoming more prevalent.”

Middleton also referred to the wider recognition the sector is receiving with the high NPS scores. “From all the mutuals around the table here, clearly when the customers are being recommended by the brokers to come to us, they’re voting with their feet,” he adds.

Following on the line of the brokers, McLeod said a lot of the growth was coming out of the third party space.

“We’ve all been working hard in the broker space over the last couple of years as more brokers use customer owned banks,” McLeod said. “I think the growth is definitely in the broker channel and the work all of us have been doing in the business, the growth we’re talking about is definitely coming from brokers.”

Brokers have also been an important factor for Bank Australia, and senior relationship manager Fernando Lemos said it had been bolstering its support around the third party distribution space. He added that not only was it about diversification of products, but it was also about diversification of lenders and it helps brokers cater for a wider client base.

“I think brokers are really starting to become aware of what we’re about and what we stand for,” Lemos said. “I think there’s a marketing edge as well: They can go out there and promote themselves, they’re not just a line to a particular organisation, they can look after certain type of clients.”

Agreeing with this, McLeod said there had also been an effect thanks to the extra regulation, such as the caps to interest only loans.

“We all had to slow down for the caps,” he said. “But when it’s opened up, the brokers who used four lenders are now using ten, so it really gave us a chance because we’re in that ten. So it’s really opened up the market because it was so confusing who was doing what, who’s doing construction, who’s doing interest only, who’s doing investment, so it’s opened up the market and it gives us a shot at getting the business.”

As one of two brokers in the roundtable, Vault Plus Mortgage and Finance Consultancy broker David Merison said the demographic of people wanting to borrow money meant they wanted choice, rather than relying on those who came straight out of banks and were simply agents for those lenders.

“We’ve got to hold ourselves open and come up with some innovative solutions and that means introducing some lenders they wouldn’t always think of,” he said.

Fisnure broker Christopher Lee said he viewed his primary objective as putting the most amount of money in his client’s pocket rather than the bank’s pocket, and the mutuals have a cheaper alternative, as well as a more diverse product range.

Not only that, Lee simply enjoys dealing with the mutuals more. “They actually listen to you and there’s genuine open conversation,” he said. “I’m there to work for my clients and a lot of my clients don’t have a straightforward profile, but the mutual banks are always willing to listen and to see how they can potentially make the deal work.

“And you don’t just feel like a number; I know a lot of the staff at the mutual banks and that gives me the confidence to pass it on to the clients.”

Q: How are you keeping up with players like fintechs in terms of technology and innovation?

Technology has been crucial for a while, but these banks fully understand that does not mean it stops where it is. Everyone is continuing to innovate to make the path faster and simpler for both brokers and customers, but Saunders cautioned that it is not the most important factor for them.

While the mutuals are “fairly on par” with the rest of the lending space, they can offer a much better customer experience on top of the mobile apps and internet banking.

“Yes, fintechs are looking at experience, but a lot of customers are looking for more than just fastest decision, cheapest loan, they’re looking at what we’re doing in corporate and social responsibility and how we engage with communities,” he said.

“There’s a lot more that we stand for than just our technology. While we’ve all got a focus on it, we’ve all got a focus on a number of areas as well.”

Although that may be the case, McLeod said Beyond Bank had invested in its apps and technology to ensure customers expect the same experience at a mutual than they would anywhere else.

“You don’t want them to say I used to do that with CBA, I can’t do that with Beyond, so we invest a lot of time to make sure our internet banking is right up there,” he said.

“I think it’s a combination of having that technology and having that people side. If you get that mix right, if you’re using the technology to get the deals, you can still speak to someone to walk through the deal, it’s about getting that right mix together.”

The mutual banks know the major banks have more power to drive their technology, but Middleton said they can be a fast follower and they are already providing the internet banking, mobile apps and all the tools that NextGen.Net offers to allow for easier processing for brokers.

He also said there were two different areas of technology to focus on: that for the customer and that for the broker. When it comes to introducing new systems, however, there can be resistance, which has always been the case, added Middleton.

“It wasn’t that long ago, electronic submission came through. Brokers resisted doing – they wanted to fax,” he said. “They’d fax in reams of paper and moving from that to a monoline lodgement was a big thing, so it’ll be interesting to see the evolution and how brokers respond to that.”

Lemos agreed and said there were some brokers who loved embracing new technology, but others who were not interested in the technology piece.

“They want the ability to say, I want to pick up the phone, rather than plugging it into a system that’s going to position my deal, so it’s a real fine balancing act,” he said.

“Electronic lodgement sounds great in theory: I think for your vanilla deals, perfect. But what about the rest? It’s important to have a human element behind it. This comes back to why we’re seeing an increase in volumes – because they can pick up the phone and speak to any one of us, any of our support staff, any of our credit team.”

Expanding that, Saunders said the reason this personal experience was so good was because of the values of the people that work for the company and their attitudes towards their customers.

“I think if we look at why mutuals are exceptional in that personal interaction is the people that work for our businesses. The people that work for our businesses are working for a bigger purpose,” Saunders said.

“I think that’s why you see such high customer satisfaction numbers because our people actually really care about the customers.”

Talking from a broker’s perspective, Merison said while it is important to have those human interactions for deals which are not as simple as a vanilla loan, technology is inevitable.

“We just need to embrace it because it’s going to happen so we can’t just put our head in the sand and try and hide from it,” he said.

Q: How have non-major players - like customer owned banks - been affected by regulatory changes?

With the royal commission and changes from APRA and ASIC, brokers have seen more difficult lending landscapes as the banks shift their policies in tune with regulation. While it seems to be reported that the major banks are tightening their policies more than others, around the table Middleton said he had not seen a lot of evidence that anything had changed. In fact, he said banks like the mutuals have been treated more harshly.

“I don’t think anything’s really changed for the majors out there and what they can and can’t do,” he explained.

“From an APRA and ASIC perspective, we’re just as impacted, we get no favours. In fact I think we probably are under a harder regime because the level of experience of the regulators teams are at such a high level. Their actions are probably stronger.”

There was a murmur of agreement around the table with Middleton’s comments, and Saunders followed by adding that the biggest frustration was that all the changes they have been affected by were caused by the behaviour of the major banks.

The customer owned banks were not called up at the royal commission or had any findings out of the hearings, and Saunders said this comes down to the way the mutual are run for their customers not making profit for shareholders.

“The for-profit organisations, they’ve got a fundamental mismatch between, are they driving value for customers or for shareholders?”, Saunders said. It was found they were driving profits for their shareholders, so we’ve had to bear that brunt, as Mark was saying, and be subject to the same regulatory scrutiny and changes to practices, but on much smaller budgets. It’s proportionately greater change for us to have to deal with.”

While the royal commission was first on everybody’s lips, McLeod added an alternative factor by way of ASIC’s RG 209, an updated guidance on responsible lending obligations. While the guidelines kept ASIC’s principles-based approach, one recommendation includes brokers introducing a clear written copy of their assessment and decision into their current process.

McLeod believes this legislation could be the biggest thing to happen to the broker industry. After the regulation came out in December McLeod is concerned other banks are digesting the information and working out how they can use it to their advantage.

“What we’ll do is make sure we’re doing the right thing by regulators and the customer, and the majors will be sitting around trying to use it as a business advantage,” he said. “That’s my fear that we might see them getting more of the market, and it won’t be based on product or price or service, it’ll be some sort of regulatory loophole.”

But from the broker point of view there have been increased changes and difficulties with policies. Merison said that at least with the mutuals, there was consistency.

Talking to the group around the table, he said, “Your credit assessment team and policies have been consistent all the way along, which gives me confidence and makes my business look good. While with the major banks, they’re jumping around left right and centre.”

Q: Post-royal commission, do you think there needs to be further reforms in the broking industry?

After the royal commission final report came recommendations such as the Best Interests Duty and removing broker commissions to be replaced with a fee-for-service. The industry banded together at this time to fight for its commission payments, which would ensure adequate competition within the industry, but also a fair opportunity for all.

As broker Merison explained it, the current model is “exemplary” to make sure “all classes of society can go to a mortgage broker and get the same level of help”.

The fee for service would mean those who are less well-off are less capable of receiving help to get into a home.

“Where there’s enough profit in all of the lenders’ transactions to pay an upfront and whatever the commission might look like going forward, so there’s no out of pocket expenses for the client, it just allows a level playing field for all classes of people whether they have gone through a divorce and they don’t know a hell of a lot but they still get the same level of advice,” he said.

The Combined Industry Forum (CIF) has played a particularly important role in the advocacy for mortgage brokers. Beyond Bank’s McLeod praised the group for the good job it did in the fight for trail commission post-royal commission.

“The CIF is a great example of the industry coming together and I think the next two parts obviously are the best interest duty: working together to work that through, and then the next part is the commission piece: what’s going to change in terms of trail and upfronts and that sort of stuff,” he said.

“I think we’ve just got to continue to do that self-regulation bit and keep on top of things so we don’t get stuck when the regulation comes out.”

Around the table, self-regulation was a common theme. Bank Australia’s Lemos said reforms in any industry should be ongoing, whether it’s the finance industry, the car industry or the real estate industry.

“We as an industry should self-regulate ourselves where we get to a point where we want to get the best outcomes for the consumer that we possibly can,” Lemos said. “Now I don’t know what that means over time, but we need to be doing this ourselves, not having someone else telling us, saying this is what you need to implement as of tomorrow.”

Coming from another mortgage broker, Finsure’s Lee said while there are certain proposals he disagrees with, he thinks regulation is a positive thing. Looking at changes to commission, he said it did not make any sense to him and he would not understand what to charge a customer if a fee-for-service were introduced.

Turning it back on to the regulators, Lee said, “They need to be educated as well, the people who are conducting these proposals, or reforms. They need to be listening to both the banks and the brokers, because there were a lot of points in the royal commission where they just weren’t listening. I’m definitely for always being held accountable and ongoing monitoring, as long as it’s done the right way.”

Q: Brokers, how have you seen your workloads changing over the last year?

Unsurprisingly, the first thing broker Lee mentioned was living expenses, adding that it was not just brokers this was affecting, but credit assessors, BDMs and the banks. Brokers have been experiencing wider scrutiny of borrowers’ living expenses, particularly since the royal commission when the banks were called out for relying on the Household Expenditure Measure (HEM).

Lee said he had always been educated around responsible lending and having thorough conversations with his customers so not too much had changed for him, but he is finding a lot of additional forms on top of banks having different policies and procedures from each other.

“In that sense you don’t know what you need to be prepared for until that customer’s made their final decision who they want to go with,” he said.

With the added scrutiny, Lee is finding he receives questions from the banks even when he explains his clients’ situations. For example, a number of his clients are good with their money and spend less than the banks generally expect.

He has even found some banks going a little further: “I was exposed to a lender recently where they were even Googling descriptions on bank statements; that’s something I confess I didn’t do.”

Saunders asked Lee if he had noticed an increase in the level of detail across all lenders outside of their minimum document requirements, to which Lee said he had.

“Sometimes I joke that it’s almost better to over-declare your living expenses to try and get your loan across the line quicker,” he said.

Looking away from Australia, McLeod said that he went to America on a recent study tour and visited a brokerage to look at the credit processes there. When he asked where the living expenses were for the borrowers, he was asked why they would need it.

“They’ve got so much evidence to prove that people, when they buy their home, change their spending habits,” he explained. “So they’re relying on years and years of data which proves that people get a home loan, they used to do something and now they don’t. They don’t go out, they want to pay their loan.”

Turning again to the workload of brokers, Merison said he had some sympathy for credit assessors who have regulators looking over their shoulders, and he is choosing to embrace the new way of doing things.

“We’ve all got some more work to do. I’m not whinging, just like technology we need to embrace it,” he said. “So that’s ok, I decided to embrace it some time ago. But I kind of went beyond that in my business, I realised not only do I need to ask for more things but I need to ask better questions, more investigative questions.”