Lenders broaden loan offerings amid tight housing market

Mortgage credit availability has improved in recent months as lenders expanded loan offerings to reach more potential homebuyers in a tight purchase market, according to the Mortgage Bankers Association (MBA).

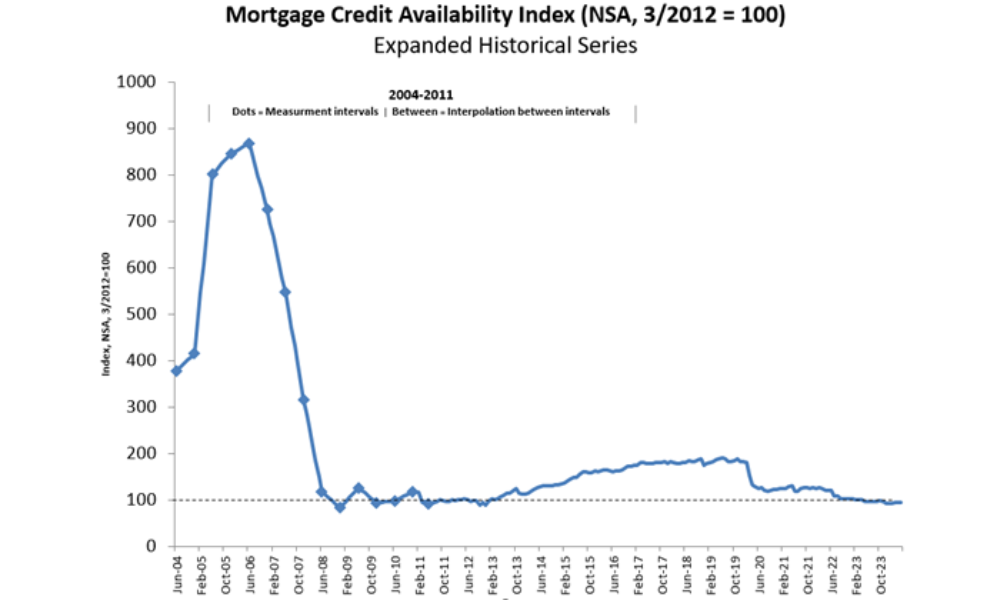

MBA’s Mortgage Credit Availability Index (MCAI) inched up 0.1% to 94.1 in May, indicating a slight loosening of lending standards. The index, which is calculated using borrower eligibility factors (such as credit score, loan type, loan-to-value ratio, etc.) from over 95 lenders, is benchmarked to 100 in March 2012.

“Mortgage credit availability rose gradually in May and has increased for five consecutive months. The overall supply of mortgage credit is still close to 2012 lows, but is slowly increasing,” said MBA deputy chief economist Joel Kan in the report. “The industry has reduced capacity over the past two years in response to extremely low unit volumes.”

Read next: Banks pull back on risky residential real estate loans

Kan highlighted that recent months have seen slight expansions in conventional, conforming, and jumbo credit availability.

The Conventional MCAI increased 0.3%, while the Government MCAI decreased by 0.1%. The Jumbo MCAI increased by 0.1%, and the Conforming MCAI rose by 0.5%.

Despite the slight expansion in credit availability, residential mortgage lending continued to struggle under the weight of high interest rates and soaring home prices.

Despite the slight expansion in credit availability, residential mortgage lending continued to struggle under the weight of high interest rates and soaring home prices.

According to ATTOM, residential loan originations fell 6.8% in the first quarter to 1.28 million loans – the lowest level since 2000.

Total lending activity was down 4.8% from the same period last year and has plummeted 69.3% from its peak in 2021. High interest rates have pushed up homeownership costs, making it harder for average wage earners to afford near-record home prices.

The report further highlighted that all major mortgage categories, including purchase loans, refinance deals, and home equity lines of credit, experienced declines in the first quarter.

Purchase loan originations fell by 9.9% to roughly 565,000, and refinance originations dipped by 1.9% to 491,000. Home equity lines of credit (HELOCs) also saw a decline, sliding 9% to 222,000.

“With little sign that interest rates are coming down, which could fire up refinance and HELOC lending, or that supplies of homes for sale are going up, any increase is likely to be limited,” said Rob Barber, CEO at ATTOM.

Stay updated with the freshest mortgage news. Get exclusive interviews, breaking news, and industry events in your inbox, and always be the first to know by subscribing to our FREE daily newsletter.