Mortgage lender Lloyds says two-thirds of UK purchase fraud now originates on Facebook, Instagram and WhatsApp – is that fraud affecting you and your clients?

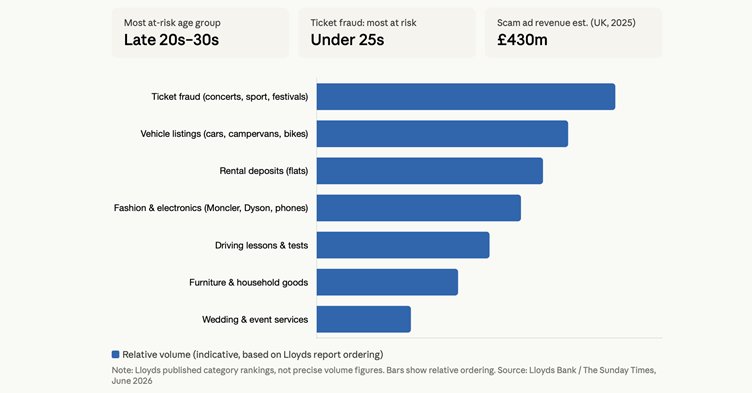

Consider the typical profile of a first-time buyer making an appointment with a mortgage broker in the second half of 2026. They are most likely in their late twenties or early thirties. They have been saving for a deposit while paying rent that accounts for 45% or more of their take-home pay, according to research by Skipton Building Society. They have been building that deposit over several years of careful, often painful financial discipline.

And according to new data published by mortgage lender Lloyds Bank this weekend, there is now a better than one-in-three chance that at some point during those years that if they were defrauded, it was on a Meta platform - and that the loss they absorbed, silently and often without reporting it, was over £500.

What Lloyds actually found

The bank's analysis, drawn from reports made by more than 25 million retail customers between March 2025 and March 2026, found that 68% of all purchase fraud reports originated on Meta platforms. The platform-linked loss figure has risen from £27 million in 2023 to approximately £66 million today - a figure that has more than doubled in two years without attracting anything like equivalent action from the originating platform. The average claim value reported to the bank now exceeds £500, up roughly £100 on last year.

Fraud categories listed in the Lloyds report read like a transaction log of life events that precede homebuying. Fraudulent deposits for flats. Fake listings for household furniture. Purchase scams for mobile phones, gym equipment, and vehicles. Driving lesson and test scams exploiting the long waits that affect younger clients trying to get mobile and working. Ticket fraud - fake Taylor Swift and Peter Kay concerts, Liverpool FC matches, Alton Towers - disproportionately targeting under-25s, including those under 18: tomorrow's first-time buyers, absorbing their first lessons in financial loss.

Facebook Marketplace features throughout. A study by Generation Rent, published in late 2024, found that over half of Facebook Marketplace rental listings it analysed showed indicators of potential fraud - newly created seller profiles, photographs duplicated from Rightmove and Zoopla, below-market pricing designed to generate rapid enquiries and deposit payments. In the period July to October 2025, the Metropolitan Police received multiple reports of rental fraud involving a single operator in London, with victims losing deposits they had saved carefully over time.

For a first-time buyer saving a 10% deposit on the average UK property, a £500 fraud loss is meaningful but recoverable with time. For someone in London, where a 10% deposit on an averagely priced property requires saving tens of thousands of pounds, even a modest fraud setback can push a purchase timeline back by months. That is the scale at which platform fraud intersects with the mortgage market - not dramatically, but persistently, in ways that show up as quiet distortions in clients' finances.

The ghost broking connection - and why it matters at the point of completion

The intersection between Meta's platforms and the mortgage market is not limited to deposit erosion. It runs directly into the transaction itself through the ghost broking pipeline - and this is a risk that mortgage brokers are already watching closely.

The Insurance Fraud Bureau tracked a 52% rise in ghost broking cases between 2022 and 2024. FCA research from May 2026 found that 49% of young drivers had purchased insurance through social media or messaging platforms, and four in ten said they would not feel confident identifying a fake policy. Ghost brokers - fraudsters selling worthless insurance documents via Facebook, Instagram and messaging apps - are generating fictitious policy documents that undercut legitimate brokers on price, leaving consumers uninsured while believing themselves protected.

For mortgage brokers who are also arranging or advising on buildings or contents insurance, or whose clients arrive at completion relying on cover arranged via social media, this is a live risk. A client completing on a purchase with a ghost-broked buildings insurance policy has no cover. If their lender requires proof of buildings insurance as a condition of mortgage, a fake policy is a transaction-breaking problem - and, under Consumer Duty, it is the kind of outcome a thorough adviser should have anticipated and prevented.

Bringing the ghost broking risk forward - raising it during the protection advice conversation rather than at the eleventh hour - is both a Consumer Duty obligation and a practical safeguard for the transaction.

Consumer Duty: the broker's real obligation here

The FCA's Consumer Duty has been in full force since July 2024. Its outcomes-based framework places firms under an explicit obligation to understand the circumstances of retail clients, to identify vulnerability, and to ensure that the advice and products delivered serve the client's genuine interests.

Consumer Duty does not extend a broker's liability to fraud committed by third parties on social media platforms. But it does have practical implications for how brokers engage with a clientele that is, by Lloyds' own data, experiencing financial crime at significant rates.

As Mortgage Introducer reported last September, Keith Humphreys of Pinpoint Commercial Finance has articulated the downstream problem with precision: "Mortgage fraud has a knock-on effect that reaches right across the market. For lenders, it damages confidence, which leads to tighter criteria, slower processes, and higher costs for genuine borrowers. Lenders have to recover their losses somehow, and that means everyone pays the price in the long run."

The same logic applies to platform fraud. A client who has lost money to a Facebook scam and is now short of a deposit target faces a binary choice: wait longer to save, or misrepresent their position. Paradigm Consulting's 2025 mortgage fraud analysis found that 25-to-34-year-olds - exactly the first-time buyer demographic most exposed to Meta fraud - are the age group most likely to commit application fraud, citing affordability pressure as the underlying driver. The broker sitting across from that client is the last line of defence between a frustrated aspiration and a fraudulent application. Consumer Duty demands that firms have processes capable of identifying and responding to that situation - not as a compliance exercise, but as a genuine outcome for a client who is financially distressed.

Bob Singh of Chess Mortgages, speaking to Mortgage Introducer last year, identified the essential tension: "The fraudsters are one step ahead. The FCA and lenders could do a lot more to combat and reduce the incidence of fraud." That is true. But brokers cannot wait for the regulatory environment to catch up before treating their clients' full financial circumstances - including losses that happened before the mortgage conversation began - as relevant to the advice they give.

The legal pressure on Meta and what it means

The group fraud claim being assembled by Richardson Hartley Law and Humphries Kerstetter - now attracting more than 260 victims - argues that Meta has breached its contract with users by permitting the conditions in which scammers operate at scale and in some cases profit from placing paid advertisements on the platform. The claim's eligibility window covers losses in the past six years, capturing the majority of the working-age adult population that forms the core mortgage-buying demographic.

Reuters' reporting in November 2025 added a dimension that resonates beyond the legal arena: leaked internal documents reportedly showed that Meta's own assessments placed approximately 10% of its 2024 revenue - around $16 billion - as generated from scam advertisements or ads violating its own policies, and that the company maintained internal "revenue guardrails" limiting how much of that income it was willing to sacrifice. Whether those documents feature in the UK group action remains to be seen.

The regulatory pressure is also tightening, though slowly. Meta launched a judicial review in the High Court in May 2026, challenging Ofcom's methodology for calculating Online Safety Act fines based on worldwide rather than UK-only revenue. A hearing is scheduled for October. Were Ofcom to prevail, the company faces potential penalties of up to 10% of global revenue - a figure that, on $201 billion of 2024 revenue, runs to tens of billions of pounds. Meta describes the approach as "disproportionate and unlawful." Ofcom says it reflects "a plain reading of the law."

For mortgage brokers, the trajectory of that litigation matters primarily as context: it tells you something about the gap between the scale of the problem and the pace of the institutional response. The £66 million being lost annually by British consumers on Meta's platforms is not going to be resolved by any regulatory action in the near term. The costs are being absorbed now - by victims, by banks under the APP reimbursement regime, and by the mortgage market in the form of clients who arrive at your door in a worse financial position than they should be.

The wider picture

The Lloyds data, the Ofcom dispute, and the group legal action against Meta are all expressions of the same underlying problem: a platform generating billions in revenue from an advertising ecosystem that includes, knowingly or otherwise, a significant volume of fraudulent content - and the costs of that fraud being distributed to everyone except the platform.

For UK mortgage brokers operating in a market where rates are competitive, volumes are rising, and 1.8 million borrowers are coming to the end of their fixed rates this year, the clients coming through your door are predominantly the people Lloyds identifies as most at risk from Meta-originating fraud: late twenties to early thirties, saving carefully, digitally active, time-pressured. Consumer Duty asks what outcomes you are delivering for them. One of the answers, increasingly, has to engage with the financial world they are actually navigating - not just the mortgage transaction in front of you.

Liz Ziegler's line from her Sunday Times piece is worth carrying into the next client conversation: "Fraud prevention needs urgency, strong action and a clear focus on protecting people before they fall victim." The platform regulator has not yet found the mechanism to make Meta share that focus. In the meantime, the broker sitting opposite a first-time buyer is often the most trusted financial professional that person has ever dealt with. That trust is worth using.