Rents remain under upward pressure ahead of new tenancy rules

Real estate consultancy Knight Frank has lowered its short-term expectations for UK house prices after the Middle East conflict fed through into mortgage pricing and buyer confidence.

“The Middle East conflict has pushed mortgage rates higher, dampened buyer sentiment and fuelled speculation about how the government will respond to the resulting economic shock,” said Tom Bill, head of UK residential research at Knight Frank. “This hat-trick of headwinds means we have revised down our near-term house price forecasts.”

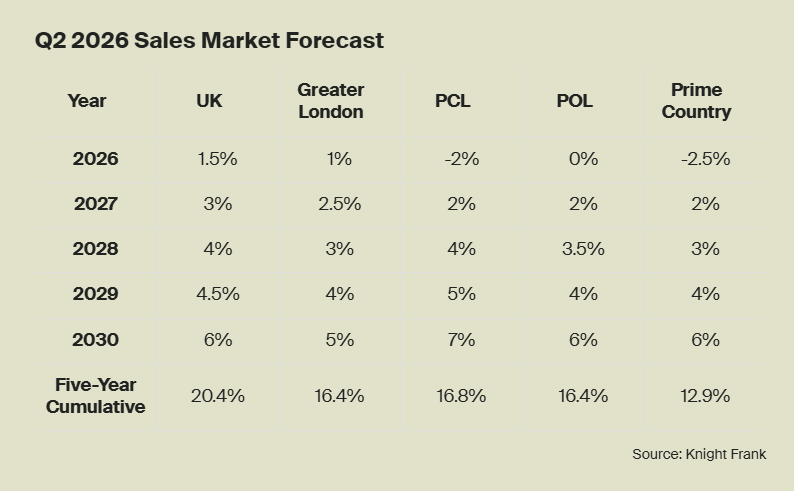

The firm now expects UK house prices to rise by 1.5% this year, followed by 3% next year and 4% in 2028. In its September view, it had pencilled in 3% growth in 2026 and 4% the following year.

Knight Frank said the economic picture was still forming because the conflict, which began on 28 February, had only recently started to show up in the data. It pointed to diverging house price readings, with Halifax reporting annual growth slowing to 0.8% from 1.2% in March, while Nationwide’s measure rose to 2.1% from 0.9%. It added that mortgage approval and transaction figures available so far pre-dated the conflict.

On inflation, the consultancy noted a rise in headline inflation in March, driven by higher energy costs, to an expected 3.3%. It said underlying inflation — excluding food and energy — came in lower than forecast at 3.1%, which could make the case for holding rates in April more likely.

Knight Frank also flagged that the latest fall in unemployment masked an increase in economic inactivity, rather than signalling stronger growth.

In mortgage markets, the firm said swap rates used to price fixed-rate loans had moved higher since the conflict began. It reported the five-year swap rate trading at around 4% this week, compared with just under 3.5% before the war started, though it had eased from about 4.3% in March.

It added that any direct impact on house prices may be softened by the share of homes owned outright: it cited 36% owned without a mortgage versus 29% with a mortgage in England. It also highlighted political uncertainty and the risk of tax speculation ahead of the Autumn Budget, alongside questions over the post-summer make-up of government.

Prime markets: weaker near-term expectations

Bill (pictured right) said higher borrowing costs and geopolitical uncertainty were expected to weigh on prime markets, even though buyers typically have more equity.

Bill (pictured right) said higher borrowing costs and geopolitical uncertainty were expected to weigh on prime markets, even though buyers typically have more equity.

Knight Frank now forecasts prime central London prices to fall by 2% this year, instead of being flat as previously expected. Prime outer London prices are forecast to be flat in 2026, down from a prior expectation of 2% growth.

For its “prime Country” market — covering £750,000-plus locations outside London — the firm expects average prices to fall by 2.5% in 2026. It said prices in that segment fell by 5.5% in the year to March.

Longer-term view: uplift assumed from 2029

Knight Frank said it had raised longer-term forecasts on the assumption that a new government takes office in 2029. It argued that, despite uncertainty over the composition of any future administration, current polling suggested a tilt towards lower taxes and tighter controls on public spending, which could reduce government borrowing costs and support affordability.

The firm said it expected a shift in political direction to support annual house price growth of more than 5% in mainstream and prime markets in 2030.

Rents: marginal downgrade, but pressure remains

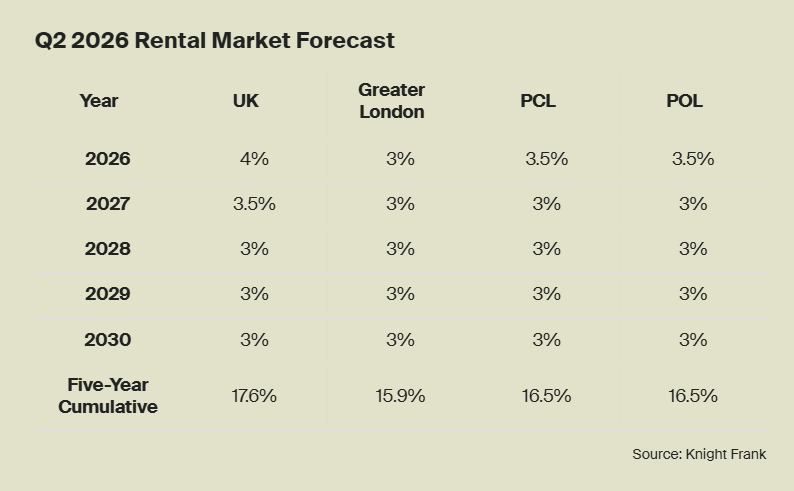

Rental forecasts were reduced slightly, but Knight Frank said upward pressure on rents would continue this year, which it linked to the introduction of the Renters’ Rights Act.

It said the rules, due to take effect on 1 May, increased risks for landlords around repossession and sales, rent setting and income certainty — factors it said would push rents higher. The firm also suggested supply could tighten if more landlords exit the market once the rules are in force.

Knight Frank expects 3.5% annual growth in prime central and outer London rents this year, and said rental demand may also be supported in the near term as some households delay buying amid higher borrowing costs and geopolitical uncertainty.

On energy efficiency requirements, it noted discussion around landlords needing an EPC ‘C’ rating by 2030. “This particular change in legislation I think is going to be bigger and potentially more demanding (than the Renters’ Rights Act) because I don’t believe we’ve got the infrastructure to support it,” said Louisa Sedgwick, head of mortgages at buy-to-let specialist Paragon Bank.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.