BTL lending tilts to interest-only as rates bite

Mortgage rates for buy-to-let borrowers have climbed over the past month, pushing a larger proportion of new lending above 5% and raising monthly costs for many landlords.

An analysis by Hamptons, using data from Connells Group, found the average rate secured by landlords in April rose to 4.84%, from 4.20% in January. The average rate on two-year fixed deals taken so far this month was 4.73%, up 0.63 percentage points since January, while the average five-year fix was 4.94%, an increase of 0.74 points.

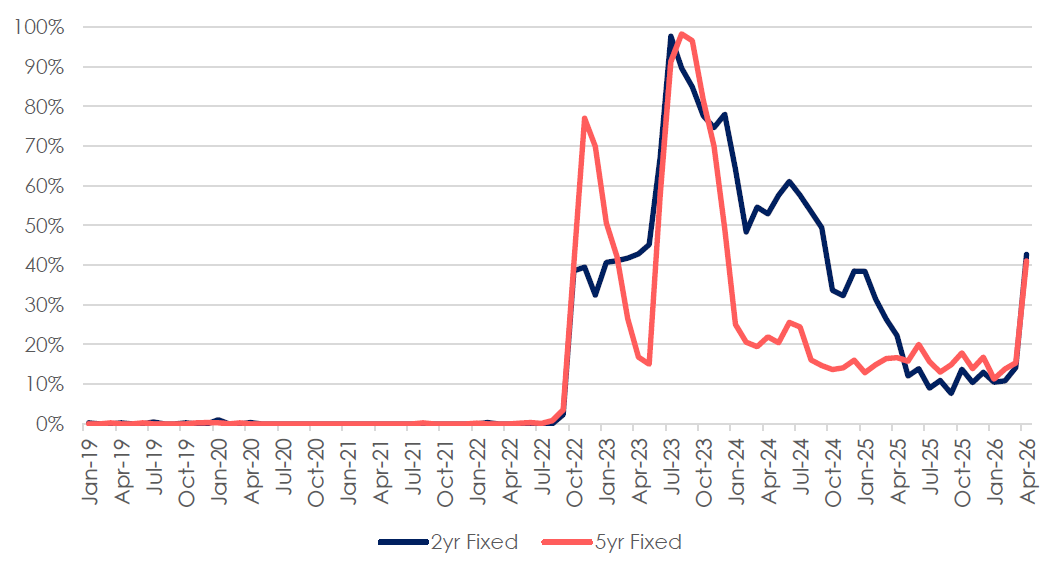

By early April, 43% of new buy-to-let loans were agreed at 5% or higher, compared with 8% in January, returning to levels last seen in December 2023. Hamptons said the change had materially increased financing costs, particularly for borrowers coming off older fixed-rate deals.

Share of new buy-to-let mortgages with a 5%+ rate  Source: Hamptons using Connells Group data

Source: Hamptons using Connells Group data

Landlords reaching the end of two-year fixed terms in April recorded an average 3.4% rise in monthly mortgage payments, according to the analysis. Those rolling off cheaper five-year fixes taken out in 2021 faced a much larger jump, with payments up 28.5%.

Hamptons said mortgage rate rises tend to have a bigger effect in buy-to-let because most borrowing is interest-only. It estimated that an increase from 2% to 4% would double payments on an interest-only mortgage, compared with a 29% increase on a repayment loan. On a £150,000 mortgage, this would equate to an extra £250 a month on interest-only, versus £162 on a repayment basis.

The firm said landlords had responded by leaning further towards interest-only borrowing, reducing balances when refinancing, and shifting towards shorter fixed-rate products. More than three-quarters (78.4%) of lending for new buy-to-let purchases in April was on an interest-only basis, the highest share since October 2022, and up from 71.1% in January 2026. The proportion of remortgaging landlords moving to interest-only was described as broadly unchanged.

On an average landlord purchase in April 2026, Hamptons estimated a repayment mortgage cost £828 a month, compared with £580 on interest-only — a gap of £258, the widest since September 2022.

Alongside the move towards interest-only, Hamptons said more landlords were putting in additional cash at remortgage. In 2026 to date, 40% of interest-only borrowers injected cash when refinancing, up from 34% in 2025. Among those with under 20% equity, 65% reduced borrowing at remortgage, compared with 35% of landlords with 40% or more equity.

The average downpayment at remortgage this year was £30,100, which Hamptons said was equivalent to cutting the outstanding balance by 18.1%. That reduced the average loan-to-value on remortgages from 61.6% to 55.2%. Around two-thirds of the fall in average LTV was attributed to overpayments, with the remainder linked to house price growth over the mortgage term.

Hamptons also pointed to a shift in product choice. It said two-year fixes had been priced below five-year fixes since May 2025, with the difference equal to about £26 a month in additional interest for a borrower choosing the longer term. Two-year fixed rates made up 48.3% of landlord lending so far in April, compared with 33.0% for five-year fixes. In each of the first four months of 2026, two-year deals accounted for more lending than five-year products.

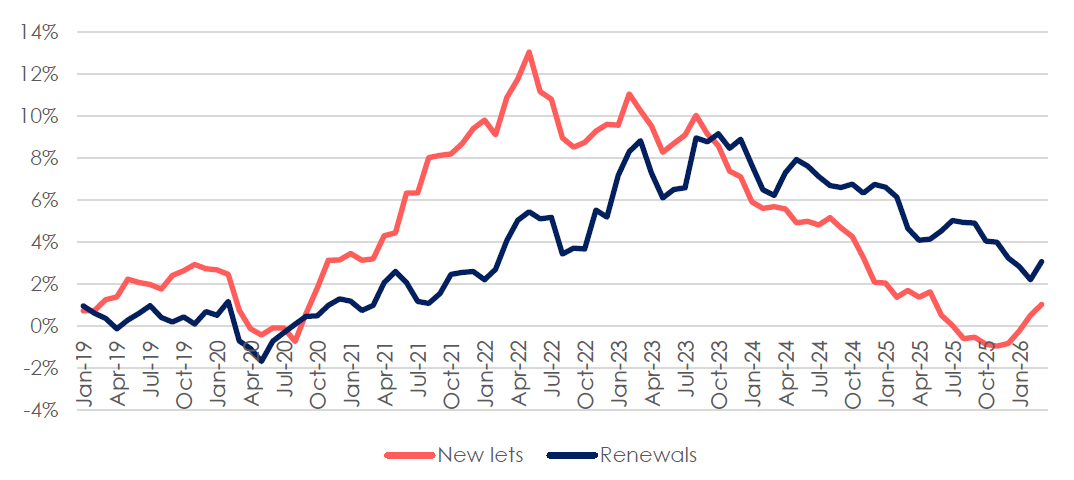

On rents, Hamptons said growth on newly let homes had begun to pick up after slowing through much of 2025. Annual rental growth across Great Britain rose from 0.5% in February to 1.0% in March. Inner London led the increase, with rents up 4.1% in the year to March, reversing declines recorded since the start of 2025.

Annual change in rents  Source: Hamptons using Connells Group data

Source: Hamptons using Connells Group data

Tenant demand also rose, the firm said, with a 24% annual increase in the number of renters searching for a home in March, and double-digit rises across every region of Great Britain. Over the same period, there were 1% fewer homes available to rent than a year earlier, and supply was 33% lower than in March 2019.

Hamptons said rents for renewals showed a similar pattern: in March, renewal rents increased 3.1% year on year, up from 2.2% in February. It added that fewer properties were being let above the advertised rent, with 6% doing so in the first quarter of 2026, down from 56% in the first quarter of 2021.

The firm said March was the penultimate month in which landlords in England could accept offers above the advertised price, and argued that the change would affect how rents are set rather than the final level achieved. It added that if rental growth strengthens further, there may be a widening gap between advertised and agreed rents after the Renters’ Rights Act takes effect, as advertised rents could become more of a ceiling than a floor.

| Annual rental growth | ||||

|---|---|---|---|---|

| Region | New lets | Renewals | ||

| Average monthly rent | YoY % | Average monthly rent | YoY % | |

| Greater London | £2,305 | 2.2% | £2,164 | 0.3% |

| Inner London | £2,733 | 4.1% | £2,616 | -1.5% |

| Outer London | £1,990 | 0.3% | £1,831 | 2.2% |

| South | £1,345 | 0.2% | £1,272 | 4.3% |

| East of England | £1,260 | 0.6% | £1,262 | 5.7% |

| South East | £1,465 | 0.0% | £1,350 | 3.0% |

| South West | £1,247 | 0.2% | £1,166 | 5.2% |

| Midlands | £1,046 | 1.5% | £981 | 4.9% |

| East Midlands | £999 | 1.8% | £936 | 4.9% |

| West Midlands | £1,087 | 1.2% | £1,021 | 4.8% |

| North | £955 | 0.3% | £905 | 5.1% |

| North East | £823 | -1.3% | £772 | 2.6% |

| North West | £1,028 | 0.9% | £944 | 6.6% |

| Yorkshire & Humber | £917 | 0.2% | £914 | 4.1% |

| Wales | £879 | -0.8% | £818 | 2.5% |

| Scotland | £1,014 | 0.8% | £934 | 4.0% |

| Great Britain | £1,373 | 1.0% | £1,294 | 3.1% |

| Great Britain (Ex London) | £1,134 | 0.4% | £1,071 | 4.6% |

| Source: Hamptons using Connells Group data | ||||

“Rising mortgage rates are once again shaping landlord behaviour, as many look for ways to manage higher borrowing costs,” said Aneisha Beveridge (pictured right), head of research at Hamptons. “The last time interest rates rose sharply back in 2022, they unleashed record rental growth.

“Rising mortgage rates are once again shaping landlord behaviour, as many look for ways to manage higher borrowing costs,” said Aneisha Beveridge (pictured right), head of research at Hamptons. “The last time interest rates rose sharply back in 2022, they unleashed record rental growth.

“Landlords were able to pass higher mortgage costs on to tenants as would-be buyers increasingly chose to rent until rates began falling back, stoking demand for rental homes. In effect, three or four years of typical rental growth were squeezed into the space of 12 months.

“While rents fell last year, early signs suggest the pace of rental growth is beginning to pick up as tenant demand rebounds and mortgage rates rise. The falls recorded in 2025 have already been wiped out, while the 24% annual increase in tenants starting the search for a new home in March was the largest since our records began.

“While stronger rental growth may help landlords balance the books over the medium to long term, mortgage stress tests mean they must also remain profitable in the short term, even at higher rates. For many, that means keeping mortgage payments at an affordable share of the rent – whether by paying down debt or moving over to interest-only deals with lower monthly costs.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.