One Nation mortgage plan has ignited debate, but break costs and funding models make US-style fixes a hard sell

What to make of One Nation's latest policy brainchild.

The minor party has suggested putting Australians into 30-year fixed-rate home loans at 5%, sold over the counter at Australia Post, with the tab picked up by scrapping the Albanese government's $11.5 billion Housing Australia Future Fund.

It's a neat pitch on paper – a rate comfortably below the 6%-plus average on new owner-occupier loans, unlocked with just a 5% deposit that could come from superannuation or a first-home buyer grant.

The trouble, as with most things that sound too good to be true, is in the fine print.

Richard Holden, an economics professor at the University of New South Wales (UNSW), told the Australian Financial Review the real funding bill could balloon to 10 to 50 times the advertised $11.5 billion once borrowers inevitably stampede toward the cheaper government rate.

Challenger chief economist Jonathan Kearns has raised a related concern – who wears the losses if house prices fall and defaults follow?

Even One Nation can't quite agree with itself: Treasury spokesman Barnaby Joyce has downgraded the plan to "a discussion piece," while leader Pauline Hanson insists the costs are already capped and budgeted.

MPA asked brokers, lenders and aggregators what they actually make of importing a very American idea into a very Australian market – and the consensus is that the two systems don't translate quite as neatly as a 30-year fixed rate might suggest.

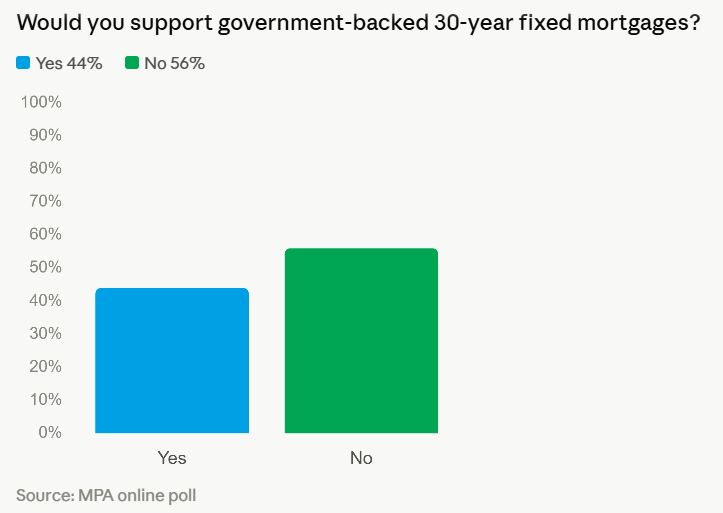

An online poll found mixed support for such a scheme, with 44% saying they would support 30-year fixed mortgages and 56% saying they wouldn’t.

“The devil’s definitely in the detail on this one,” said one respondent. “Big ideas sound great, but what really matters are the terms for the borrower, the flow‑on effects for the home‑loan industry, and whether the government can realistically fund it. And if taxpayer liability sits behind it, that needs serious scrutiny.”

“As long as it can be transferred dollar for dollar to another property, with sufficient security in place, and without breaking the fixed rate, it is something I would support and recommend,” said another, adding: “If not, and there were break rates involved, it would be an untenable offering.”

Troy Phillips (pictured, right), director at FirstPoint Mortgage Brokers, explains that the US mortgage market benefits from deep capital markets funding, and borrowers can generally refinance without the sort of break costs they’d encounter in Australia.

In Australia, break costs apply whenever a borrower exits, refinances, or switches a fixed-rate loan before the term ends, and they’re calculated on the difference between the wholesale rate at the time of fixing and the wholesale rate at the time of exit, multiplied by the loan balance and the remaining term.

Because Australian lenders fund fixed-rate loans through wholesale markets rather than a deep securitised secondary market, they pass that funding-cost mismatch directly onto the borrower.

“Imagine the break cost on a 30-year fixed rate on a $1.5 million loan with 22 years to run? It would be north of $300,000,” says Phillips.

The US system works almost in reverse. Prepayment penalties on US mortgages were largely reined in after the 2008 crisis: under Dodd-Frank and the CFPB's qualified mortgage (QM) rules, a penalty can only be charged on certain qualifying fixed-rate loans, and even then it's capped at 2% of the balance in the first two years and 1% in year three, disappearing entirely after that. US government-backed loans are barred from carrying prepayment penalties at all, and most conventional 30-year fixed loans written today simply don't include one.

Despite the differences in prepayment penalties, Phillips considers the Australian mortgage market as one of the best in the world – “It's flexible, highly competitive and borrowers benefit from that. In many ways, I reckon the US would love parts of the system we've got.”

Tony MacRae (pictured, left), chief commercial officer at Bluestone Home Loans, agrees that there are fundamental differences between the US and Australian markets.

“While there may be consumer appeal for 30-year fixed loans, Australia’s funding model is very different to the US, where long-term fixed rates are supported by a deep secondary mortgage market,” said MacRae. “It’s not something that can be easily replicated here, and there are significant funding and pricing challenges lenders would need to investigate before participating.”

A history lesson

Nonetheless, One Nation’s off-the-cuff policy suggestion is not particularly unique – the New South Wales government’s ill-fated HomeFund, which ran through the 80s and early 90s, offered mortgages for low-income borrowers for loan terms between 25 and 30 years.

Rising rates and a flawed "low-start" loan design (initial repayments didn’t even cover the costs of accruing interest) caused mass borrower defaults and a genuine social housing scandal, forcing a government bailout and restructuring in 1993.

The FANMAC corporate entity, which administered the scheme, later transformed into prominent non-bank lender Resimac.

The policy being floated by One Nation differs in that repayments will be fixed at 5% rather than HomeFund’s floating-rate design, but Phillips sees issue here too.

“Who would genuinely want to lock in for 30 years at 6% today? If rates fall, borrowers will want out… If Australians fixed for 30 years and rates dropped materially, either borrowers would be hit with enormous break costs, or someone else would be wearing that risk. Governments love floating these ideas, but execution is the hard part, and that's usually where they fall over.”

Tanya Sale (pictured, centre), chief executive of outsource Financial, is not a huge fan.

“While the likes of a 30-year fixed-rate mortgage being currently bandied around is being presented as a solution to housing affordability, I am not and never will be convinced they would assist in improving home ownership outcomes,” Sale told MPA. “The reality is that affordability is driven primarily by house prices, housing supply, household incomes and borrowing capacity, not simply the length of a fixed-rate term.”

It’s worth noting that 40-year mortgage terms were also bandied about in recent years as a solution to soaring monthly mortgage costs (not to be upstaged, the US has floated the idea of 50-year terms).

But while some lenders – Great Southern Bank, MA Money, Liberty, Pepper Money and RACQ Bank among them – offer 40-year terms, they are little more than a rounding error in the wider Australian lending ecosystem.

Borrowers, at the end of the day, treasure flexibility.

“Many homeowners make extra repayments, refinance, restructure their lending or sell well before 30 years,” says Sale. “A long-term fixed-rate mortgage can reduce that flexibility and potentially leave borrowers exposed to significant break costs if their circumstances change… they are unlikely to address the fundamental challenges preventing property buyers from entering the housing market.”