Industry leaders weigh in as banks push for a register to track non-compliant practice

Calls for a national register of mortgage brokers who engage in misconduct are gaining momentum, backed by an overwhelming show of support from the industry – but significant questions remain about its design, scope, and whether lenders should be subject to the same scrutiny.

An AFR report suggested the Australian Financial Crimes Exchange (AFCE) – an independent body that co-ordinates intelligence and investigation of financial crimes – is putting together a broker portal to record the names of those who meet a specific threshold of non-compliant behaviour.

The register may later be extended to include bank employees. AFCE's membership includes Westpac, NAB, ANZ, Commonwealth Bank, Macquarie, the Australian Taxation Office, the Customer Owned Banking Association and more.

It comes as the estimated extent of alleged mortgage fraud at the major banks has blown out to $4 billion. In face of this mammoth figure, the mortgage broking industry resolutely agrees that something must be done.

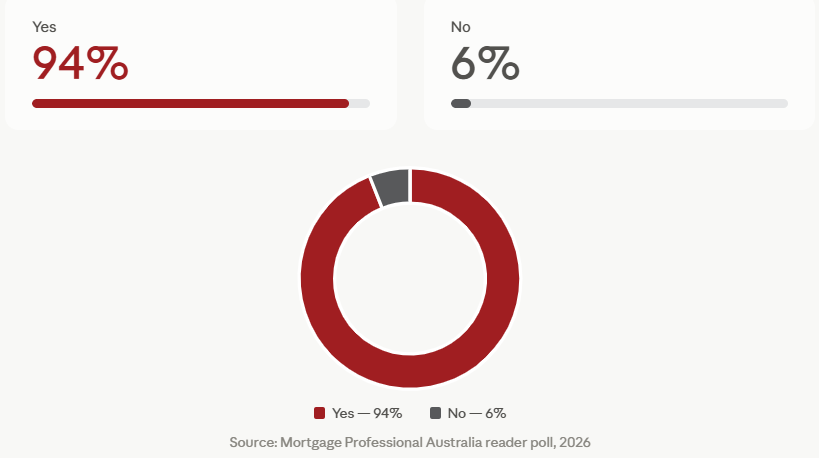

An MPA poll put the question to mortgage professionals directly: would you support a national register of brokers who engage in misconduct? The verdict was clear – 94% said yes, with just 6% opposed – although the finger pointing could do with some recalibration.

The Hai Money collapse

Recent months have laid bare the real-world consequences of alleged misconduct in the mortgage finance industry.

In December 2025, Andrew W. Hu – a former NAB and Commonwealth Bank employee who had become a mortgage broker – was charged with helping the so-called Penthouse Syndicate secure almost $100 million in fraudulent mortgage and business loans.

Hu's arrest had direct consequences for Sydney-based sub-aggregator Hai Money, where he had been writing loans under its credit licence.

"Hai Money removed 14 brokers from its network in December 2025 after NAB, one of its panel lenders, suspended their accreditations amid conduct concerns linked to a handful of brokers."

This April, Hai Money collapsed following the termination of its contract by parent aggregator Finsure, leaving over 200 brokers without access to their Australian Credit Licence (ACL) – the licence required to write new loans in Australia.

In court documents, Finsure boss Simon Bednar cited reputational concerns of being associated with Hai Money and to this day, the futures of brokers operating under the collapsed sub-aggregator remain in limbo.

The Hai Money collapse is a stark example of how the alleged misconduct of a small number of brokers can upend the livelihoods of hundreds who did nothing wrong.

The blame game

The broking industry has rightfully defended itself in response to bad press over poor broker behaviour.

Speaking off record, one broking industry source raised concerns that the register proposal could serve as a convenient distraction from misconduct within the major lenders themselves.

They noted that one major bank's internal estimates suggest approximately 90% of the fraud uncovered involved banker and referrer channels, with brokers representing a smaller proportion of the overall problem.

The source also argued that expanding the existing Australian Securities and Investments Commission (ASIC) credit representative framework – rather than building a new register from scratch – could achieve the same outcome more efficiently.

Under the current system, only brokers not employed by an Australian Credit Licence (ACL) holder carry an individual credit representative number. Employees of ACL holders and lenders at banks and non-banks operate under the ACL without individual appointment – a gap the source says should be closed.

“We all want to work in a clean industry, but this feels like an opportunistic play for banks to curtail broker impact by focussing on regulating us more, and not tidying up their own house,” they said.

Defining ‘dodgy’

AFG chief executive officer David Bailey (pictured, top of page, left) said the aggregator has long advocated for better information sharing across the industry, “the same way banks already share that information among themselves”.

Bailey believes intelligence needs to flow in all directions if all stakeholders want to be serious about addressing an industry-wide issue. “This is a whole-of-industry problem. Brokers, lenders, accountants, conveyancers, lawyers, and real estate agents all operate within the same ecosystem, and all must be part of the response,” he said.

Read more: Are bankers-turned-brokers slipping past Australia’s fraud radar?

Tanya Sale (pictured, top of page, centre), chief executive officer of outsource Financial, welcomed the proposal in principle but cautioned that the register's effectiveness would hinge entirely on its design.

"A list of 'dodgy brokers' sounds simple yet defining what constitutes dodgy behaviour is complex,” said Sale. “If the register is built on strong standards and due process it could assist in ridding 'dodgy brokers' – but let's not leave it at that, we should be going one step further and include 'dodgy bankers and accountants'. If not, it risks becoming a blunt instrument that does more harm than good."

Son Pham (pictured, top of page, right), managing director of Rethink Finance in Australia, drew directly on his background as a former financial planner to make the case for a register. "I actually welcome this," Pham said. "I was a financial planner before this and we had such a register for financial planners. From what I am hearing it isn't just the broker that is committing the fraud – it's a combination of broker, accountant and solicitors. Yes, there are fraudulent brokers but there are bad eggs in every industry. Just don't make it out like we are all bad."

MFAA calls for effective communication

Australia’s peak broking industry body the Mortgage & Finance Association of Australia (MFAA) is also calling for better information sharing across all segments of the mortgage finance industry.

“Allegations of fraud and misconduct should be taken seriously, and the industry supports strong, timely action to identify and remove bad actors. Effective information sharing between lenders, aggregators, regulators and law enforcement is an important part of maintaining the integrity of Australia's lending system,” said MFAA executive of policy Naveen Aluwahlia.

The MFAA “remains committed to working collaboratively with government, regulators and industry to further strengthen fraud prevention, enhance consumer protection and continue building confidence in Australia's lending ecosystem, while recognising the professionalism and high standards demonstrated by the overwhelming majority of mortgage and finance brokers”, Aluwahlia added.

How a financial planner register works – and could a broker version follow?

Australia already operates a model worth examining. The Financial Advisers Register is a public record of financial advisers who provide personal advice to retail clients on relevant financial products.

It is a public database maintained by ASIC that lists individuals authorised to provide personal financial advice to retail clients in Australia, allowing consumers to verify an adviser's licence authorisation, qualifications, employment history, and any relevant disciplinary outcomes.

AFS licensees are responsible for appointing and maintaining the details of their relevant providers on the Financial Advisers Register. Each listing includes the adviser's name, registration number, and ABN, along with their current and previous Australian Financial Services licensees, qualifications, and any disciplinary actions or banning orders issued by ASIC.

The requirement for financial advisers to be registered was introduced following the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

The planner register model is precisely what Son Pham points to as his benchmark. "The financial planning register provide(s) information from adviser registration number, registration status, banned status, education and qualifications," he said. "I would be displeased if the banks are just trying to paint all brokers as rotten eggs as they try to push their own agenda."

The off-record source echoed this view, suggesting that expanding the ASIC credit representative appointment framework to apply universally – covering all lender employees and brokers with an individual licence number they carry throughout their career – would be a cleaner and more durable solution than a lender-led portal.