In a year like no other, six non-banks gathered virtually to discuss the biggest topics in the broking industry right now

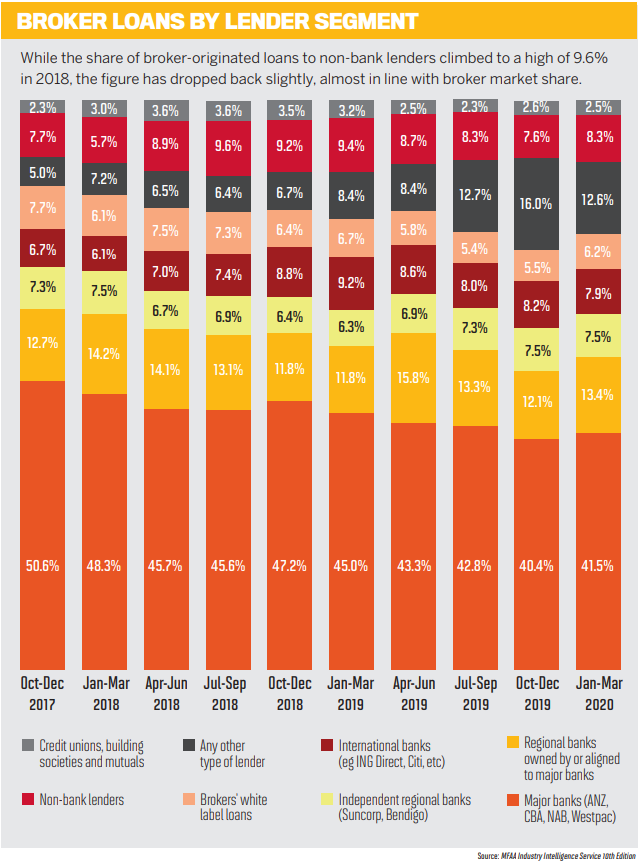

At last year’s roundtable, the non-banks began by talking about the increasing volume of loans coming to them from brokers. According to the MFAA’s Industry Intelligence Service survey at the time, 9.4% of brokeroriginated loans had gone to non-banks in the most recent reporting period. The picture is a little different this year: the coronavirus pandemic has meant that non-banks have pulled back from new originations to focus on supporting their existing customers. Not only that but, as refinancing activity has surged, the major banks have rolled out incentives in a big drive to take back market share.

Shifting to a virtual discussion in 2020, this year’s panel featured six non-bank representatives: Aaron Milburn from Pepper, Cory Bannister from La Trobe Financial, Daniel Carde from Resimac, James Angus from Bluestone, Joanna James from Mortgage Ezy, and John Mohnacheff from Liberty.

The big topic of 2020 was of course how COVID-19 had changed the industry. The panellists delved into the changes they had had to make, highlighting how strong the non-bank proposition continued to be for borrowers and the work their teams were doing to prepare for the ‘new normal’.

Although this year’s format was different as panellists were not in the room together, we still encouraged brokers to send in questions throughout the discussion. Brokers also submitted questions when registering for the livestream.

The topic brokers were most interested in asking about was the best interests duty, which is due to come into play in January. While it seems there is still some concern about how brokers will prove they are working in their customers’ best interests, the panellists were adamant that it would not be a big change and encouraged brokers to read the guidance and reach out if they had any questions.

Brokers were also keen to know how the non-banks would be embracing the future, asking about the innovations they were bringing in and how they were working on building their brands to increase consumer awareness and confidence.

The panellists tackled these questions with their usual rigour, occasionally breaking into conversation with each other as they discussed the non-banks’ role in the industry.

Read the full report to see what they had to say about what the non-banks have been doing and their plans for the future. If you would like to watch the full discussion, the video is available at www.mpa.com.au/tv.

Aaron Milburn

Aaron Milburn

Pepper Money Cory Bannister

Cory Bannister

La Trobe Financial Daniel Carde

Daniel Carde

Resimac James Angus

James Angus

Bluestone Joanna James

Joanna James

Mortgage Ezy John Mohnachef

John Mohnachef

Liberty

Q: What insights can you share from the last six months, and how have you supported borrowers?

With non-bank lenders typically being the place Australia’s self-employed borrowers turn to for financial support, it is no surprise that those represented in this year’s panel saw the impacts of COVID-19 very early on.

According to the latest AFG Index looking at broker lodgements, the market share of non-banks dropped this year, particularly in the final quarter of FY2020. At this year’s roundtable, the six non-banks talked about why this had to be the case.

“We pivoted the business to ensure that everyone who needed help got the help and proactively reached out to do that” Aaron Milburn, Pepper Money

Bluestone’s chief customer officer, James Angus, kicked off the livestream discussion by saying that this year had been about focusing on its existing customers in hardship. Within the first two weeks of April the non-bank saw two things that were alarming.

Twenty per cent of its customers approached the lender for hardship assistance, including around 10% of loans that had only been settled in March. To support those customers, Bluestone redistributed its workforce.

“Supporting our existing customers was our priority, and so we mobilised people out of underwriting roles, out of collection roles into hardship,” he said.

Angus adds that about 50% of Bluestone’s affected customers were from three industries: retail, hospitality and construction. Taking a different approach to many of the banks that were offering immediate sixmonth repayment deferrals, the lender looked to find solutions to suit individual customer needs.

“We checked in with our customers regularly, and most of them we’re touching base with every month to see how they’re doing,” he said.

“The benefit of that is we’ve been able to continue to tailor those hardship packages, and today we’ve had about 60% of people come out of hardship and resume their regular payments, which is great news for everybody.”

Another non-bank taking a proactive approach to customers in hardship is Pepper Money. Its general manager, mortgages and lending, Aaron Milburn, said the group had reached out to every single one of its customers in early March to see what help was needed.

Pepper also made an early decision to stop originating new loans until its existing customers were looked after and had the support they needed. Like Bluestone, Pepper redistributed its workforce and put more people into customer service; Milburn said the lender took a top-down approach, and he was responding to customers on social media himself.

“We pivoted the business to ensure that everyone who needed help got the help and proactively reached out to do that,” he said.

“Not dissimilar to James, what we’ve done is work with that cohort of customers to get them to a point where they’re either exiting that support that they needed or are on the pathway to doing that; then we were able to go out and start to introduce new families into the organisation.”

La Trobe Financial also repurposed its credit analysts and put them on the frontline of its hardship assistance team.

Cory Bannister, chief lending officer, said the non-bank felt it was important to have customers be able to speak to those who made the decisions on their loans. The actions taken meant La Trobe Financial saw “tremendous results”, with its hardship rates falling away quickly.

“We chose to take a more granular approach and prescribe a more specific solution for each individual customer, based on what their particular needs were” Cory Bannister, La Trobe Financial

“We chose to take a more granular approach and prescribe a more specific solution for each individual customer based on what their particular needs were,” Bannister said. “A lot of that involved loan repayment deferrals, interest-only periods and working with brokers on debt structuring to take more of a longer-term view around the repair of these customers, and it’s been really well received; we’re really pleased.”

Daniel Carde, Resimac:

Daniel Carde, Resimac:

“It’s a two-way street. We’re a broker-only brand, so we rely on brokers to be our advocates. The best way to achieve this is by providing brokers with quality service and ultimately customers with quality service. They say good things about you, and that cascades down.” Aaron Milburn, Pepper Money:

Aaron Milburn, Pepper Money:

“To Dan’s point, I think it’s about educating around what the brand is and what it stands for. We have a national presence in Australia but are also operating in New Zealand. So when we accredit a broker we talk to them about what our brand is – a little bit about the history of it, but why it’s important and what it does for customers and what it does for families. When we do our welcome call we take the time to educate the customer on who Pepper is, why it started, what it’s about and what the journey is going to be like with us.” James Angus, Bluestone:

James Angus, Bluestone:

“We’ve kicked off a set of above-the-line advertising, including billboards and other very prominent spaces to really just generate the connection for the consumer between home loans and Bluestone. What we’re trying to achieve there is when a broker is working with their customer and a broker says, ‘Hey, I think Bluestone would be a great solution’, the customer goes, ‘Oh yeah, I’ve heard of Bluestone’. That’s a big challenge for us today, and we’re working with our brokers to try to raise awareness and help consumers make the connection with Bluestone.”

Q: As we’ve all faced a difficult year, what are you doing to reassure brokers that you are working in their best interests?

Having no physical branches and operating without the level of marketing that the banks possess, non-banks rely heavily on the broker channel. So, this year, while banks have more than one channel to manage, the non-banks have really drilled down in their focus on brokers.

Joanna James, general manager of Mortgage Ezy, said this support of brokers goes to the heart of non-bank businesses. As customer needs change and mainstream banks pull back in some areas, James assured brokers that non-banks would continue to offer a range of solutions.

“We’re still offering those solutions for those individual client needs, the ones that aren’t black and white,” she said.

“They may have something individual about their particular situation; there are niche products such as self-managed super lending that they’re unable to access through the majors, and so we’re still supporting brokers in being able to support more clients by having a variety of products that actually suit their needs.”

Transparency has been a big theme for Resimac this year, said general manager distribution Daniel Carde. While the nonbank did not make a lot of credit changes, he said, when it did it was upfront about them early on. In terms of origination, Resimac ensured that brokers were able to use digital ID and signatures as far back as April.

“One good thing that came out of COVID is that it brought that forward for a lot of organisations,” Carde said.

“We were already heading towards it, but it accelerated it probably by a month to bring it in sooner rather than later.”

Another big point Resimac focused on at the start, in an effort to support brokers, was trail commission.

“We realised that brokers are business people as well,” he said. “For brokers to lose 20% of their trail income would have been a difficult task, so we made the decision very early that we would continue to pay broker trail for those customers who entered into a repayment holiday.”

“We’ve always asked questions; we’ve always assessed loans on a case-by-case basis – and that’s the way we’ll continue” Daniel Carde, Resimac

Liberty group sales manager John Mohnacheff said it was “all hands to the pumps” when the pandemic hit, as the team had conversations with borrowers and educated them on their options. He added that the non-bank threw as many resources as possible at the broker channel, because while the economy took a hit, it didn’t stop.

“We firmly believe it was during these challenging times that brokers needed us most, as did a lot of Australian borrowers,” he said. “We saw a very strong drive in the SME space because a lot of the self-employed were dramatically hit, and it would have been the worst time in the world to pull away and not help those people.”

Speaking about Liberty’s involvement in the government’s SME Guarantee scheme and its efforts to support small businesses and self-employed borrowers, Mohnacheff said, “The more we can help them the sooner we can help the economy get going, the sooner we can get people back to work, re-employ people, get repayments going again. So we have thrown in all of our resources to work with our business partners and make life as simple as possible.”

In working with brokers at Bluestone, Angus said the non-bank had learnt quickly to change the way it communicated with the channel, and to provide tools to help brokers become more efficient.

“We believed that it’s not a good customer outcome if you’re settling customers one month and then they go into hardship the next,” he explained.

“What was really important for us was how do we communicate those decisions in a way that brokers can understand, and they understand why you’re making the decisions and support them.”

Cory Bannister, La Trobe Financial:

Cory Bannister, La Trobe Financial:

“For us at La Trobe Financial it’s leveraging history. We’ve got almost seven decades’ experience of operation, so in terms of when customers ask the question ‘How do we trust your brand?’, well, it’s been around for 68 years now. When I look around this group, this is a good representative set of the non-bank financial institution space, in which cumulatively we probably manage in the order of $60bn–$70bn of mortgage assets under management, so we’ve all got a long history and track record in the space, and that in itself speaks volumes.” Joanna James, Mortgage Ezy:

Joanna James, Mortgage Ezy:

“We go through a whole onboarding, educational program with brokers to make sure they really understand the products. It’s not just who we are, but how do we do what we do? How does securitisation work? How do you explain it to clients? What are the benefits of working with a non-bank lender that’s different to a mainstream lender? We’ve done a lot of work in communicating that clearly, because there’s still a lot of confusion in the marketplace around how that actually works.” John Mohnacheff, Liberty:

John Mohnacheff, Liberty:

“If brokers are talking about above-the-line sort of stuff, Liberty has just signed up with the WBBL and BBL Melbourne Renegades teams to drive brand awareness. But we also have our own branded network, Liberty Network Services, and our cars are always branded; we’ve got lots and lots of vehicles and billboards all over the place, so people are more familiar. So our brands are out there. When you talk to people, prompted awareness is pretty high for non-banks.”

Q: After this year, how important is it that non-banks can look at a customer’s wider situation?

Over the years, non-banks have always prided themselves on their ability to look closely at individual borrowers and their situations. This year has seen that become more important than ever.

“I definitely agree that at the heart of non-banks is that ability to understand a client’s individual needs, and that’s something we do very well” Joanna James, Mortgage Ezy

Bannister said that major economic events like COVID-19 underscore the importance of non-bank financial institutions, and he called out a couple of themes from this year to support that.

Firstly, he pointed to the tightening of the major banks’ credit appetite and their focus on a “very narrow aspect of the credit market”, adding that while it made sense because of the demand for refinancing, it left a significant portion of the mortgage market overlooked.

Then he highlighted the trend that has been playing out for a couple of years, of consumers turning to brokers.

“Where there’s complexity and confusion in the marketplace – and there’s no more complexity and confusion than in a pandemic – that only provides tailwinds to brokers and then also into non-bank financial institutions,” he said.

With the continuing impacts of the COVID-19 restrictions, Bannister said it would not be a linear recovery and could possibly play out for the next two to three years. This is when he believes non-banks will really come into play.

“I think for many businesses it’ll be five steps forwards and maybe half a step back from time to time,” he said. “That’s where you’ll see non-bank institutions come to the fore, because the customer may not pass an automated credit assessment process; they will require a conversation.

“It’s a totally legitimate scenario; it’s a credit event that’s played out post the fact, and that’s what we do best.”

Seconding that, James said non-banks didn’t take a “cookie-cutter approach”; credit assessors would call brokers to follow up with questions and talk through the deal.

“Our credit assessors will get on the phone and ring a broker and say, ‘this is what I’m looking at, this is how I’m seeing the picture; can you please expand on this part’,” she said.

“That was evidenced dramatically during the immediate hit when COVID happened and we had to reassess every loan. Every single client that was going through, we were looking at the picture of their forward forecast, so I definitely agree that at the heart of non-banks is that ability to be able to understand a client’s individual needs, and that’s something that we do very well.”

Carde commented that it was not the fault of the consumer that they were in this position, pointing out that everyone was caught up in the crisis and impacted differently. In fact, he said his wife was one of the self-employed whose businesses had shut down pretty much overnight.

“Supporting our existing customers was our priority, and so we mobilised people out of underwriting roles, out of collection roles into hardship” James Angus, Bluestone

- Aaron Milburn, Pepper Money:

“[The borrowers] found the house, the kids have already picked out the bedroom, and lenders are the ones that get in the way. So we’ve got to smooth that path. That’s the whole ethos of the Product Selector that Mario [Rehayem, CEO] created: in two minutes you give a customer a conditional approval. Our job is to make that realisation of a dream seamless and make the broker look like a hero, because it’s repeat business that builds broker businesses, and we cannot forget that.” - Cory Bannister, La Trobe Financial:

“Customer expectations are always around a solution focus; it’s key to everything at this stage. What we saw throughout the pandemic is that speed became a very close second. Having a quick approval and clear path to settlement has always been what our customers seek generally, but more so through this period of confusion and complexity. They want that uncertainty removed, and they’re willing to go with the lender that can give them that level of certainty, and we’ve been a beneficiary of what I would call ordinarily vanilla loans purely because we can settle them within a week.” - Daniel Carde, Resimac:

“It’s actually put brokers in a much better position because there is uncertainty in the market. We’ve gone through regulatory change in the last five years which created opportunity for brokers; we’ve just gone through a global pandemic and some consumers are concerned and disillusioned about what they can and can’t do. That’s where a broker jumps in. The timing is absolutely perfect for brokers to take advantage of the opportunity to help those people.”

- Joanna James, Mortgage Ezy:

“Another thing the pandemic has done is it’s broken down traditional structures. So a lot of clients want more flexibility around when and how they are communicated with. We’re all getting more and more comfortable with digital platforms, so I can see that for a lot of brokers that’s going to be important. “Above and beyond that, there are just a lot of people who need a lot of support right now. So one of the things you can do is really upskill your ability to be that person to guide somebody through, and whilst it may not be appropriate to offer personal counselling guidance, you’re basically walking them through what is a very stressful situation at a very stressful time.” - James Angus, Bluestone:

“[Customers] want an easy process, a great experience underpinned by great people, and that’s what non-banks do really well. Where customers and brokers are getting very disappointed and in many cases feel let down is when they get an automated decline of sorts and the broker rings the bank to find out why and they’ve got to wait on hold for two hours. That’s what’s shifted. I don’t think the expectation has changed, but in some cases the delivery has changed, which has forced a lot of brokers and customers to reset what they want in this transaction.”

“We’ve always asked questions; we’ve always assessed loans on a case-by-case basis, and that’s the way we’ll continue,” he said.

“The only way you can get an understanding of everyone’s individual circumstances is to ask those questions.”

Particularly in the context of 2020, having that focus on individual circumstances had allowed the non-banks to have conversations with borrowers at all stages – even those who had not settled their loans yet.

“When [the pandemic] did hit we had to look at some of those loans we’d approved that were due to settle, and I’m pleased to say there wasn’t one single purchase loan that we didn’t settle,” Carde said.

“But we did have the conversation with the borrowers; some borrowers may not have wanted to settle and may have had an opportunity to get out of the contract if they were in dire circumstances, like they’d completely lost their job. We found for most of our borrowers it was just a slight change in circumstances.”

Saying that “people are people”, Milburn pointed out that if brokers lined up 20 people a year ago and the same 20 people this year, far more of the latter group would be unable to fit a major bank’s requirements this year.

“We’re all different, so we cater to that,” he said. Pepper doesn’t have a monoline credit policy that provides just one opportunity to fit a box, he added.

Remembering the MPA roundtables of a few years ago, Milburn said that back then he had to explain what non-banks were and why brokers should use them. Now, the conversation has gone beyond that, and using nonbanks is woven into the fabric of what brokers do every day.

“The share of deals that brokers are doing for non-banks has grown, because as a broker you get one opportunity when you sit in front of a family to show them you’re the person that can deliver their hopes and their dreams for that purchase or that investment or commercial property,” Milburn said.

“A lot of the selfemployed were dramatically hit, and it would have been the worst time in the world to pull away and not help those people” John Mohnacheff, Liberty

“Do you roll the dice and put it through a monoline solution that continues to change and is archaic in its view? Or, do you go with an organisation like Pepper or one of the brands that my colleagues are with today where you’ve got more than one opportunity to help that family and get them on a product that’s absolutely right for them today?

“That’s why non-banks are here to stay, because we look at people as people, not as a credit policy.”

Agreeing that non-banks think differently about their customers, Angus compared his time at Bluestone with his previous experience at Macquarie.

“At a major bank you’re talking a different language. You’re focused on numbers; settlement numbers, net interest margin, cost to income, return on capital and so on,” he said.

“As a broker you get one opportunity when you sit in front of a family to show them you’re the person that can deliver their hopes and their dreams” Aaron Milburn, Pepper Money

“It’s been a revelation for me coming into Bluestone, because it’s all about the customer. We talk about customers; we talk about customer satisfaction and how we help customers. It’s just a completely different mindset.

“We’ll always take the time to understand a customer’s situation and provide them with the best solution, rather than say, ‘I don’t like your credit score, I’m not even interested in who you are, I don’t even know your name, but it’s a decline’.”

James added that the non-banks took a “common-sense approach”, looking at situations from more than one perspective.

She also called out how the non-banks worked to support brokers, as this is how the non-banks grew in the first place; she said this cohort of lenders really cared about their individual customers and brokers.

“I had clients that had loan applications going through who were locked out of the country and couldn’t get back in in the middle of the pandemic and were posting social media messages at 11.30 on a Friday night, and I’m answering them,” she said.

“That’s not something you would get in a major institution, so we really do care. It’s a personalised approach not only to the client but also to the broker, because it’s their business and it’s their reputation that we represent when we do what we do.”

While a decade ago consumers would approach home loans with the intention of getting the lowest interest rate, Mohnacheff said there had been a dramatic shift, and that was because of the way brokers were now helping borrowers.

“This is where the non-banks are masters,” he said, adding that these lenders had always worked to support brokers in finding solutions.

“Cookie-cutting does not work. That approach is archaic, and I think more and more ascendancy from the non-banks will just go to prove that it’s not about just rate; it’s about finding the right solutions for those humans.

“And it’s not just the solution for today, but it’s a long-term solution. We’ve got home loans that are going out for 30 years; it’s an enormous commitment, so let’s make sure we get the solution right first time at the start.

Q: How do brokers make sure they are working in the customer’s best interests as they help borrowers navigate their options?

Many questions sent in by brokers for this year’s panel discussion were related to the best interests duty, which comes into force in January. When asked what brokers need to do to prepare for it, Milburn said his answer was one that may not be popular: essentially, read the guidance.

The final regulatory guide was released by ASIC in June and provides guidance on the effect of the range of credit providers and products brokers can access, recommending packages of credit products and the types of records that may be kept to demonstrate compliance. That final point on keeping records is one that brokers have been particularly concerned about.

Milburn said brokers should not be waiting for someone to tell them how it was going to work; they needed to read and understand the guidance themselves.

“Slow down, is the first thing I would say, and have a really detailed conversation,” he said. “If it was me, I’d include notes everywhere, just to articulate why I’ve made the recommendation that I’ve made.

“It’s been a revelation for me coming into Bluestone, because it’s all about the customer. We talk about customers; we talk about customer satisfaction and how we help customers” James Angus, Bluestone

“This shouldn’t be feared. This is guidance for what 99.9% of brokers do today. You’ve got to document; you’ve got to ensure you’ve really articulated why you’ve made the recommendation. But don’t let it frighten you or change your natural style, because that’s why you’re successful as a broker.”

Carde agreed that this wasn’t a new thing for brokers. He said they had “been doing it forever and a day”, so the only thing that had changed was that it was regulated, and detailed notes needed to be kept to justify brokers’ recommendations.

Many in the industry are already prepared for BID, and Carde spoke of a recent fact-find he had read, in which the broker had recommended a Resimac product.

“We weren’t the cheapest, but if you read the notes underneath, the broker actually went to the trouble of saying, ‘I’ve chosen this particular product because they’re in this circumstance, and that fits this lender’s policy’, Carde explained.

“So it wasn’t the cheapest, but it was the most appropriate loan, given that individual borrower’s circumstance. So if brokers keep taking that approach you’ve got nothing to worry about.”

“We made the decision very early for those customers who entered into a repayment holiday that we would continue to pay broker trail” Daniel Carde, Resimac

To align recommendations to a customer’s best interests, Mohnacheff said the broker’s first step was to properly understand the customer when it came to filling out the application forms. He said brokers just needed to take their time, complete the application carefully and accurately, and include all the notes and documentation.

Do it once; do it right the first time. That’s all we’ve ever asked of our broking partners. We will be there to support you all the way through. If you’re stuck somewhere, pick up the phone; assessors, BDMs, we’re all there to help, and it should not be feared. It shouldn’t be feared if you’re doing the right thing.”

It comes back to having the confidence to make the call about what is in the client’s best interests, James added. She said that if brokers chose something on rate but the customer was going to lose their deposit the following week, would that really be in their best interest?

If the loans are like for like, the cheaper product is probably right, but James said it was not always that simple.

“As we’ve talked about today, lending is not black and white, in fact it’s not even grey; it’s all sorts of colour rainbows in the middle,” she said.

“As businesses we’re there to support you in understanding what information you need to really be clear that you’re making the right judgment call, that you’re choosing something based on policy or service and is that appropriate, and then how do you make your notes around that? As opposed to guessing from a computer program that’s letting you know you’ve got a choice of this, this and this. There’s a lot more depth to it.”

Q: We’re all becoming more reliant on technology. What are you offering brokers to help make their jobs easier?

The topic of technology naturally came up during the hour-long discussion, but as several brokers had also asked about what innovations the non-banks were bringing to the table, we turned to the topic again.

Aside from the well-known offerings like digital identification, e-signatures and online platforms, Mohnacheff pointed out that what the panellists were doing there and then, meeting in a virtual environment, was a sign of how everyone has been forced into a digital world.

COVID-19 has brought faster change to technology and the way brokers conduct business than would have been seen otherwise, but he added that he was not sure how much more digitisation could be brought in without taking away the human element.

Using technology to speed up processes is a given for all lenders at the moment, but Mohnacheff warned about taking it too far.

“I don’t think most people, when we’re making a big financial decision, are all that comfortable just to rely on a conversation with a machine without having some reassurance about, have I made the right decision here, do I know all my options, am I aware of all my opportunities?” he said.

“We have to be very careful that we don’t push too far into the digital world and push customers away. I think what we need to do is find the right balance between the human interface and machine assistance.

We’ve all said we are here to support person-to-person. But the new norm is here, and what we’ve created is an opportunity to do it this way or face-to-face – but we’re still looking at the faces; we’re not just listening to voices. So I think there’s probably enough change already without thrusting more change until we’ve become comfortable in this new environment.”

The sudden thrust into a mostly digital environment has actually benefited brokers and businesses, Bannister added. With the border closures and lockdowns, he says technology has “fast-tracked businesses’ ability to become borderless”.

“It’s all pretty much run of the mill now what we can do on the loan processing side, but using technology to become borderless has been great” Cory Bannister, La Trobe Financial

He said he had already heard of brokers being able to expand beyond their usual patches using tools like Zoom to reach customers and referral partners, and pointed out that it was the same for non-banks.

“It’s a real boon for us in the non-bank financial institution space because we don’t have the huge marketing budget that a major bank would, or even the size of the sales force,” he said.

“It allows us to cover more territory than we’ve ever done before, so I think that’s been a really interesting observation. It’s all pretty much run of the mill now what we can do on the loan processing side, but using technology to become borderless has been great.”

Angus said this was an interesting point and called out Bluestone’s sales team, which had to pivot very quickly from being out on the road doing face-to-face meetings to being inside on phone calls and Zoom meetings.

He said technology had allowed for “tremendous efficiencies” in the way nonbanks operate, and brokers would see these lenders’ sales teams continue to leverage technology, but not at the expense of traditional relationships.

“They will of course meet face-to-face with brokers at their request; they’ll do everything they’ve done really well historically. I just think you’ll start to feel like the sales teams within these organisations have suddenly grown,” Angus said.

“It’s not that they have; they’ve just leveraged technology to be more productive and to cover the needs of more brokers throughout a given period of time.”