Analysis and commentary in the aftermath of the final report, which recommended changes to broker pay

Analysis and commentary in the aftermath of the final report, which recommended changes to broker pay

UNLESS YOU have been living under a rock, you will know that the final report of the royal commission was handed down earlier this month, with some strong recommendations affecting broker pay.

Speaking after the release of the report, Treasurer Josh Frydenberg confirmed the government would be taking action on all of the recommendations, including the complete abolition of trail commissions and volume-based bonuses for brokers.

The report also recommended eventually removing upfront commission, and Frydenberg said this would be reviewed in three years to determine the potential impact of doing this, considering that previous reports have all recommended otherwise.

While there is still a lot to be done before the 1 July 2020 cut-off of trail commission, brokers, industry associations and wider supporters are understandably concerned about the impact these changes will have.

Steve Mickenbecker, Canstar’s group executive of financial services, has said mortgage brokers won’t be going anywhere, but he raised concerns that their numbers could reduce.

“The two intermediary groups – financial planners and mortgage brokers – look to be taking the brunt of the whole formal recommendations approach,” he added.

“The fees and trails people have been getting from banks – try justifying that and getting that from the borrower who’s already stretched. It’s going to get a lot tougher.

“With the level of commissions that brokers might have earnt in the past, it’s going to be very difficult to stay in this environment.

That must lead to the law of supply and demand; it’s going to be a less lucrative industry, so the number of brokers must decline, and that will push people back into the bank channels.” Mickenbecker said smaller banks and lenders were reliant on the broker channel, so they might have to make some changes in order to survive.

.jpg) “There will be brokers around, there’s no question. I think we do have to test just how many consumers are prepared to pay a broker,” he added.

“There will be brokers around, there’s no question. I think we do have to test just how many consumers are prepared to pay a broker,” he added.

“We would have to think that online origination platforms are going to have to get better and get better fast to survive in a declining distribution model.

“Then obviously we don’t want to see a destruction of competitiveness; we want to see competitiveness increasing.

I think people will have to invest heavily and fast in online originations.”

Melos Sulicich, CEO of MyState Bank – which relies heavily on mortgage brokers as a distribution channel – is hoping that any legislation will not skew in the direction of the big banks.

“It’s a pivotal point to ensure that consumers’ best interests are looked after in the future.

Smaller lenders like MyState rely on mortgage brokers for our distribution.

Without them the playing field is skewed towards the big banks,” Sulicich said.

“Mortgage brokers are very pro competition, and as a consequence of that the mortgage broking industry has to be financially viable for all the participants in that industry.

If it’s not financially viable and the industry starts to shrink, then the cost of mortgages for the Australian public will go up.”

In order to help level the playing field for smaller lenders, Commissioner Hayne recommended a Treasury-led working group that would look into whether banks should also charge a fee for facilitating a loan and how that would work.

The recommendations for mortgage brokers did not stop there. Hayne also suggested the establishment of a best interest duty.

The Combined Industry Forum has already been working towards developing and implementing a ‘customerfirst duty’.

Hayne acknowledged the CIF’s efforts in his report, but said it was not clear what would be the content of the customer-first duty.

He said it appeared to be a duty that would give preference to the customer’s interests only in cases where their and the broker’s interests did not align.

Mark Haron, director of Connective and deputy chair of the CIF, said, “We’ve always supported a movement towards a customer-first duty, and therefore fundamentally support Hayne’s recommendations for a best interest duty.

“The devil is in the detail, however, and we are particularly interested to see how the best interest duty will extend to all lenders, including the banks. Improving customer outcomes requires a level playing field..PNG)

“Rather than recommending sweeping change for the sake of change in every sector of financial services, we believe the existing laws and CIF’s reforms should be given a chance to have an impact. “The unintended consequences of Hayne’s recommendations in relation to the mortgage broking industry is reducing competition and handing yet another free kick to the big banks.

Competition needs to be fiercely protected now more than ever. Reducing choice is not the answer.”

AFTER MONTHS of wondering what Commissioner Hayne would recommend in his final report, the industry has to think about what will happen now that we know.

While Treasurer Josh Frydenberg has said he will accept the recommendation to ban trail commission and volume-based bonuses for mortgage brokers, there is more to be done before that point.

According to a senior lecturer at the University of New South Wales, the implementation of these recommendations could be “watered down” by the time they are legislated, particularly with the lobbying being carried out by the industry.

Marina Nehme explained, “There will be a public consultation within the sector just because it’s a controversial move.

Then a bill will be put forward in front of the Parliament, and with support it will pass.

“Some of those recommendations do not need legislation, like the ones that deal with the regulators like ASIC enforcement, because this is something that can be done internally.

“[For broker remuneration] you need to regulate how much remuneration is paid, so to make it clear that you can’t get paid by the banks, then probably yes, we would need legislation.

But there’s strong lobbying from the industry, because the question is, how will the industry survive if the remuneration will be paid by the clients? Will they be willing to pay this remuneration to mortgage brokers? That’s a big question, and there is this issue that if you remove the remuneration structure, will that affect competition in the banking industry?

.PNG)

Asked whether there was a chance the legislation affecting broker remuneration would not make it through Parliament, Nehme said, “There’s always a chance.

Nothing is set in stone yet. How watered down it will be down the track is just a case of wait and see and how much lobbying there is, because there will be a consultation.”

Speaking of lobbying, there are already a number of campaigns underway to defend mortgage brokers, including from industry association MFAA.

The group launched a national advertising campaign within days of the final report being released. Working with a number of industry partners, the group is encouraging consumers across Australia to search for and write to their local MPs using the ‘Your Broker Behind You’ campaign website. Brokers are encouraged to share the link with their customers, who MFAA CEO Mike Felton expects will also feel disappointed at the result of the final report.

Voicing concerns echoed by many, Felton questioned how brokers had come out of the final report so badly, when the royal commission was called to review the behaviour of the banks.

“The royal commission was set up to protect them from big bank power, but has simply entrenched it further,” Felton said.

“How mortgage brokers can be front and centre of the recommendations is inexplicable to me.

A massive new bank fee added to the cost of buying a home cannot be a good outcome for Australians.”

He added, “Brokers are critical to competition in home lending. As such, the MFAA is leading a campaign to call attention to this issue and help Australians understand that low interest rates, competition and the services they receive from brokers for just under six out of every 10 new home loans are under threat.

“We have launched a national advertising campaign this week, and we are calling on everyday Australians to join us in a grassroots campaign to protect competition by letting their local representatives know they support the broker channel.

Broker mental health

While many brokers may feel like they are in limbo and are concerned for their businesses as a result of the changes, Lifeline said it was perfectly common to feel uncertainty and stress.

Last year the group began working with the MFAA to run sessions on mental health.

“Mortgage brokers will justifiably feel uncertainty and fear about how their businesses and livelihoods will be impacted, so it is important for workplaces and communities to be sensitive and alert to the mental health and wellbeing of its members during these turbulent changes in the industry,” Lifeline said.

“It’s important to understand that it’s OK to feel any to all of the emotions that anyone might feel at the potential loss of their business, livelihood and customers’ trust – shock, fear, anger, helplessness, anxiety, a sense of injustice, depression and even feeling suicidal.

“These are all understandable responses to the uncertainty and stress people might experience, so it is vital that we learn how to recognise when these emotions arise and to know when and how to reach out for help.”

WHILE THE recommendations of the royal commission’s final report were not entirely unexpected, the revelation that Commissioner Hayne had actually included a recommendation to switch to a borrower-pays fee for service was still a kick in the teeth for most.

The biggest concerns are how the broking industry will survive, how smaller lenders will be able to compete with the larger players, and how those issues combined will affect the borrower. Commentators are warning of higher interest rates and increased difficulty in accessing finance.

What do brokers think?

In an interview with MPA, two seasoned brokers gave their thoughts on the possible consequences the decision would have for both brokers and customers.

According to Graeme Holm, Infinity Group Australia director and 2018 MPA Top 100 Broker finalist, the recommendation was made “with a complete lack of understanding of the ongoing service provided to consumers”.

Find out the winners for the best mortgage brokerages in Australia here.

He believes the move will only hand back monopoly to big banks and remove that customer focus brokers pride themselves on.

“It’s a huge concern, and I worry it will turn a customer-service-based profession into a transactional-based sales industry, which is the exact opposite of the intent of the RC.

The recommendation really did not consider the consumer,” Holm said.

“It shows the urgent need for actual case studies of why the majority of consumers look to brokers.” For Calculated Lending director Bianca Patterson, the most concerning unintended consequence of the commission’s recommendation is that it could cause small businesses to re-evaluate their teams or service propositions to keep their doors open.

“If these changes come into effect, we run the risk of losing great brokers with years of invaluable experience, experts that we hoped would mentor the next generation of brokers.

This is a loss that clearly was not considered and just can’t be quantified until it is too late,” Patterson said.

“It is truly a sad day for our industry and consumers.”

Patterson said abolishing trail and replacing it with a fee-for-service model would render broking a service only the wealthy could afford, when in reality it was needed more by first home buyers and low-income earners.

Another 2018 MPA Top 100 Brokers finalist, Anthony O’Flynn from IFA Mortgages, echoed this concern, saying he had asked his clients whether they would pay a fee for service, and even his most loyal clients said they would not if the banks could offer it for free.

“The issue I see is that banks don’t care about any product other than their own, and this type of change would ravage the industry, reduce competition, and divert all power away from consumers and towards the big four,” he added.

What have the associations said?

The MFAA and FBAA have slammed the recommendations, both being concerned about the level of power going back to the big four banks.

They warned of decreasing competition and higher interest rates with poor outcomes for borrowers. MFAA CEO Mike Felton said it was effectively a “multi-thousand-dollar tax on borrowing”, adding that it would “put the broker channel at severe risk, damaging competition and access to credit and entrenching bank power.

“As reviews by ASIC, the ABA and the Productivity Commission have found, brokers drive competition by providing a shopfront for smaller lenders, particularly for rural and regional customers.

We are critical to the health of Australia’s mortgage lending market,” Felton said.

“I fail to see how decimating the broker channel, leaving Australians with a handful of lenders to choose from, is good for competition, or good for customers.”

The managing director of the FBAA, Peter White, accused the royal commission of failing to understand the role of mortgage brokers, in particular the competition they brought to the market. “Commissioner Hayne wants to hand even more power to the big banks and eliminate competition, which is a ridiculous scenario and shows just how out of touch he is when it comes to brokers,” White said.

“If a user-pays model was implemented, we know that most borrowers wouldn’t pay, and banks would make more money and standards would drop further.

“It’s very disappointing that the royal commission wants to destroy some 20,000 small businesses for the monetary gain of the big banks, and we trust the government will see clearly on this and continue to work extensively with our industry to improve consumer outcomes.”

.jpg) How do the lenders feel?

How do the lenders feel?

Also affected by any changes to the mortgage broking industry are the smaller banks, digital banks and non-banks which do not have the branch presence that the big four do.

Most of them rely on brokers as their main distribution channel and now face concerns about how they may have to adapt in order to reach borrowers.

The Customer Owned Banking Association (COBA) immediately responded to the report, urging caution regarding any policy changes and the need to ensure that the focus on competition was not lost. COBA CEO Michael Lawrence said, “The broking channel is an important one for many smaller lenders.

We are keen to proceed with caution to ensure that there is no adverse impact on consumers’ access to lenders and that competition in the home lending market isn’t eroded.

“It is critically important that the focus on competition is not lost. We have a banking market that is dominated by four major players, who throughout the royal commission have proved that their focus is not always on the customer’s best interest.”

Echoing concerns over competition, the CEO of SME lender Scottish Pacific, Peter Langham, said that although the report was aimed at mortgage brokers, he was worried about the impact it would have on the whole broking sector.

“Adding a broker fee for service is likely to be detrimental to anybody who can’t get funding from the banks,” he said.

“Brokers play a major role in putting non-bank lending alternatives to their clients, providing real solutions for business owners when the banks can’t or won’t lend to them.

“Fee-for-service is likely to drive borrowers straight to those with the biggest advertising budget. “Brokers have helped drive lending competition and increased the visibility of non-bank lenders. Australia’s ability to provide diverse lending options for consumers and SMEs could go backwards if the fee for service is implemented.

Whatever happens to brokers will be critical to the whole consumer and SME lending space.” Pepper Money has also voiced its support of the broking industry.

“Many brokers we have spoken with say they are being forced to reassess their futures in the industry,” CEO Mario Rehayem said.

“Pepper Money supports the broker channel because we believe they provide a wide variety of loan choices to borrowers from all walks of life, something the banks frequently do not do.

“By taking the time to understand a customer’s individual borrowing needs and sourcing appropriate loans, expert and customer-centred brokers are part of the process of creating wealth for first home buyers, young families and professionals.

“Pepper Money also believes brokers play a vital role in supporting competition in the financial services industry.

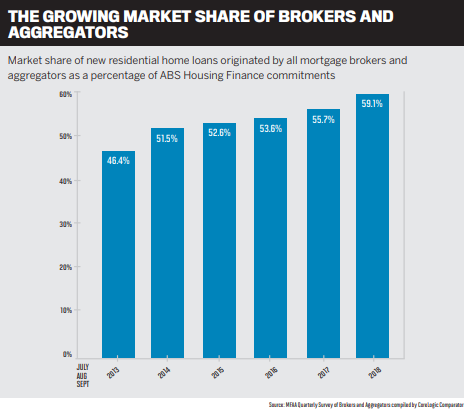

It is no coincidence that brokers’ market share has grown to close to 60% of all mortgages written. Australians have voted with their feet to support the broker channel.”

Voicing concerns that the recommendations were forcing brokers to reassess their futures in the industry, Rehayem concluded, “Pepper Money expects to play a leading role driving a regulatory outcome on the remuneration model issue that is both in the best interests of borrowers and sustainable for brokers.