As homeowners roll off fixed rates, banks are working with brokers to assist with refinancing

In 2021, Reserve Bank governor Philip Lowe said interest rates wouldn’t rise until 2024, and many homebuyers – reassured by Lowe’s words – purchased property believing they had plenty of breathing space financially. But pent-up consumer demand and ages and supply chain problems pushed inflation beyond the target range of 2% to 3%, forcing the RBA to act far earlier than anticipated and increase the official cash rate in May 2022.

Since then, the cash rate has been lifted a dozen times – a rapid succession of hikes not seen for almost 30 years. It’s a hard pill to swallow for mortgage holders, when combined with the rising cost of living and wages not matching inflation.

Higher interest rates have encouraged many homeowners on variable mortgage rates to seek a better loan deal through their existing lenders or to explore other lenders. There are also an estimated 800,000 borrowers whose fixed rate loans are due to end over the next six to 12 months.

Mortgage brokers play an integral role as borrowers looking to refinance their home loans need the expertise of brokers to help them navigate a complex market.

To discuss current trends in refinancing, MPA spoke to ANZ Retail Broker general manager Natalie Smith; CommBank executive general manager home buying Michael Baumann; ING Australia head of sales and distribution Glenn Gibson, NAB executive broker distribution Adam Brown and Suncorp Bank head of broker partnerships Troy Fedder (pictured below).

Interest rates and inflation

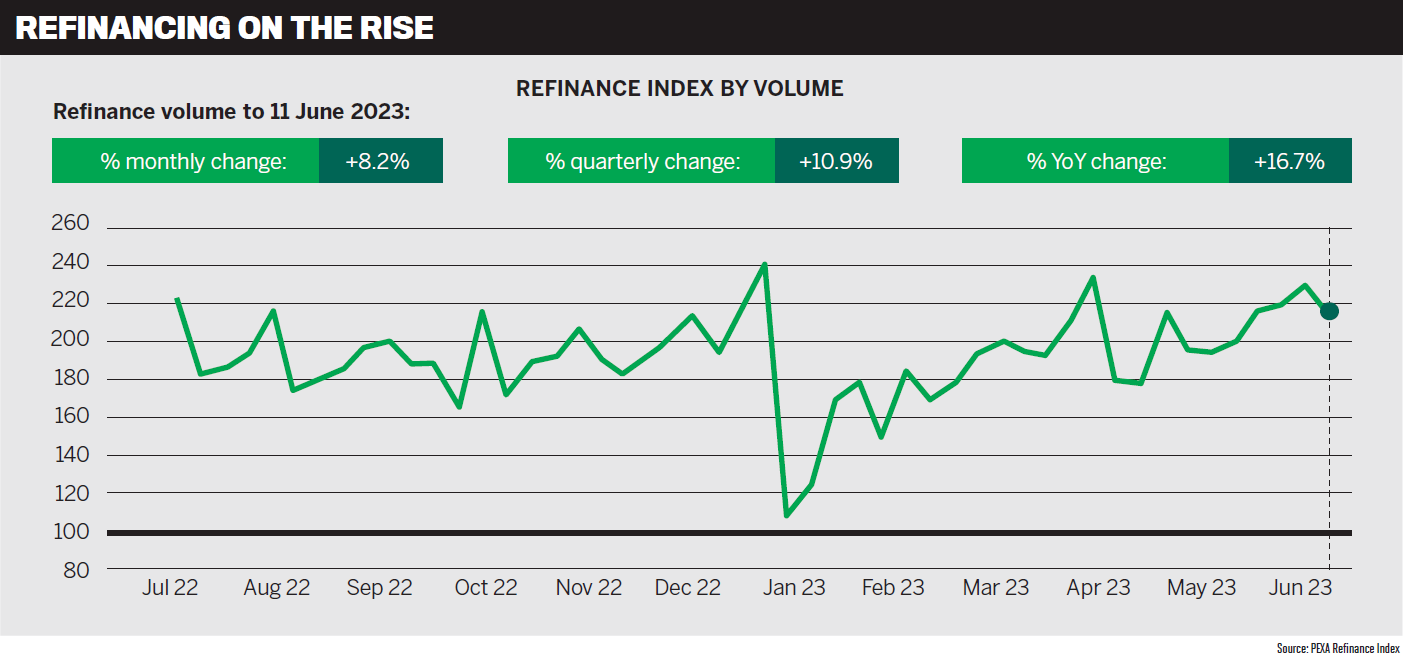

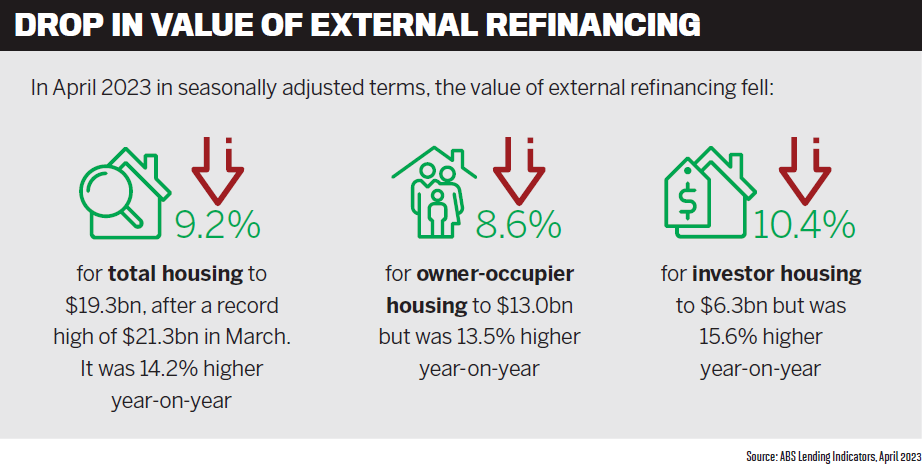

Refinancing volumes have lifted significantly compared to last year. The PEXA Refinance Index for the week ending 11 June 2023 shows volumes were up 8.2% for the month and were 16.7% higher than the same week in 2022. ABS lending indicators for April show that the value of refinancing for housing fell 9.2% but was still 14.2% higher than in April 2022.

So, what impacts are rising inflation and interest rates having on the demand for refinancing?

“Australians feeling the higher cost of living may have already taken steps to ease the pressure on their household budget by reducing discretionary spending or delaying major purchases,” she says.

Smith says many mortgage holders are expected to roll off fixed rates throughout 2023, with more to follow in 2024. “These customers may be looking for additional guidance now, to ensure that they have the right product for their situation and property goals in the future.”

CommBank’s Michael Baumann (pictured below) says that, with interest rates rising, customers have placed “a heightened focus on their home loan and the value they are getting from that loan and their lender more broadly”.

“Customers with fixed rate home loans are continuing to mature, with many taking the opportunity to reassess their needs and how their home loan supports their long-term goals,” he says.

Baumann says there has been a greater focus on cashbacks recently, but customer research shows that borrowers’ refinancing considerations go beyond cashbacks.

At ING, Gibson says great interest rates are certainly important but not the only thing borrowers consider when refinancing. Borrowers who refinance could also be:

- consolidating other debts (credit card, personal, car or other higher-interest loans) into one monthly repayment

- seeking a different product or home loan that better suits their needs in the current environment, for example with interest-only repayments or an account with or without an offset

- needing access to equity

Adam Brown (pictured below) says NAB’s Consumer Sentiment Survey for Q1 2023 shows consumer stress about rising living costs is at its highest level since late 2018, and in this environment “customers are looking to get a better deal where they can”.

Also, many fixed rate mortgages signed two years ago are reaching their expiry dates. NAB forecasts that refinance activity will peak at about $32bn in the six months to September 2023.

“As customers consider refinancing, many are turning to mortgage brokers for support in assessing their options, and brokers are doing a great job of helping customers to navigate the changes,” says Brown.

Fedder says Suncorp Bank is a net refinancer, “so we’re talking with brokers every day about refinance options for their customers”.

“Customers rolling off fixed rates are taking the opportunity to review their rates at this time, and Suncorp Bank has experienced an increase in customers refinancing across our home lending segments,” he says.

Broader cost of living impacts are also prompting some homeowners to shop around for a better home loan deal.

Fedder says the bank’s refinance options receive great feedback, and brokers and their customers are encouraged to consider loan features that also save money.

“For example, our Home Package Plus option provides a range of features, including a 100% offset facility with up to nine sub-accounts. Eligible home loans can also save with our Home Package Plus Annual Fee Refund, saving customers up to $11,250 over the life of a 30-year loan.”

Support for customers rolling off fixed rate loans

Brown says NAB continues to focus on building relationships with its existing customers to offer them the right support and products for their financial goals and needs.

NAB has been making check-in calls to broker-introduced customers, Brown says. Customers also receive communications from NAB at key milestones for their mortgages, including in the lead-up to their fixed rate or interest-only expiry.

“The message conveyed in each of these interactions is for customers to get in touch with their broker to discuss their options,” Brown says. “This is all backed up with targeted proactive pricing offers for customers who are about to roll off their fixed rates.”

Fedder says Suncorp Bank is supporting brokers and their customers with competitive rates, fast turnarounds and clear decisions. “As customers rolling off fixed loans are taking the time to compare their options, providing a fast time to decision is important for good customer outcomes.”

Suncorp Bank provides a response in 48 business hours for its SunLight loans – sometimes much faster, says Fedder. The system automatically identifies loans that meet the eligibility criteria and fast-tracks them for assessment.

Baumann says CommBank offers a range of flexible options at maturity to help meet customers’ needs and goals. These include rolling onto a personalised Standard Variable Rate product, refixing all or a portion of the loan, or considering other repayment types. Information and access to these options are available to customers through their brokers or directly through self-service options, says Baumann.

“To help support our broker partners, we have continued to invest in our digital capabilities, including launching Your Loans earlier this year,” he says. “Through the CommBroker platform, brokers can quickly and easily see their customers’ fixed rate maturity dates as well as any discounts a customer might be eligible for post fixed rate maturity.”

Access to this information helps brokers have “detailed and robust discussions with their clients” to help them understand what’s next on their homeownership journey with CommBank.

Gibson (pictured below) says ING started reaching out to its fixed rate customers last year, following a well-thought-out process that involved preemptively talking to customers about budgeting and other helpful tools.

“As the time to fixed rate expiry drew nearer, the contact centre made outbound calls, talking to affected customers,” he says. “This was an important investment the bank wanted to make to ensure customers knew what interest rate they were facing, what the process involved and what options they had.”

Smith says it’s important that ANZ continues to provide a compelling proposition – for existing customers as well as those looking to refinance through a broker.

“Our existing customers want confidence that they’re receiving a good deal, so ANZ proactively contacts broker-introduced customers with expiring fixed rates at different points of their journey,” she says.

Eligible customers can opt to receive a discount on the applicable variable rate once their fixed rate expires, or to take advantage of ANZ’s current fixed rate offers. Smith says where customers seek to increase their loan or apply for further lending, they’ll be referred to their broker in the first instance. For new customers exploring a better home loan deal through their broker, Smith says ANZ has a streamlined OFI (Other Financial Institution) refinance process for home loans.

ANZ Simpler Switch is available to eligible customers switching to an equal home loan amount, where the minimum repayments on the new ANZ home loan are less than the current repayments on their OFI loan. “The process is now available to both eligible PAYG borrowers as well as self-employed customers who meet ANZ’s Company Wage Policy.”

More lenders end cashbacks

There’s a growing trend of banks ceasing their cashback offers. At the time of print, ING, CommBank, Suncorp Bank and NAB had already stopped providing cashbacks, with ANZ the only major bank still offering them.

ING recently announced that its cashback offer would end on 30 June. “This is in response to changing market conditions and also a result of feedback received as part of our ongoing engagement with brokers,” Gibson says.

In terms of other benefits or tools to attract customers to refinancing, Gibson says ING offers competitive interest rates, new LVR bands that give customers more flexibility, great customer service, simple and straightforward home loan products that suit customers’ needs, equity, cash-out (top-up or increase), and the reassurance of banking with one of Australia’s most recommended banks.

Baumann says that in response to customer, broker and lender feedback, and with customers now focused on value, simplicity and certainty, CommBank decided to end cashback payments on new applications for home loan products from 1 June.

When considering their next home loan, CommBank customers are encouraged to think about the features they might need over the long term – “whether that’s flexibility around their repayment date, or access to multiple offsets to save on interest, or leading digital tools and insights in the CommBank App” – as well as how their chosen home loan can help them achieve their property goals.

He says White pointed out that “although cashbacks drove a lot of enquiry for brokers, they made the job of comparing loans less transparent. We [LMG] would rather advocate for lower overall rates that enable all customers to benefit, rather than some receive a ‘sugar hit’ up front.”

Suncorp Bank withdrew its cashback offer from the market in June, Fedder says. “We believe we can offer our customers and broker partners value beyond a cashback and still help them to save. We will continue to offer them leading service in the home lending space with consistently fast turnaround times and innovative products and services that meet their needs.”

Smith says ANZ continues to monitor the market to ensure that “our proposition, including products, price and other incentives, is appropriate and well placed to meet the needs of our customers”.

She adds that every borrower has a different set of circumstances and a different view of what the best-value loan looks like for them. Borrowers want to know whether a particular lender is the right match in terms of product and policy before they look at pricing and other incentives.

Brown says the market is changing quickly, with cashbacks having grown bigger and bigger over the last six to 12 months, favouring new-to-bank customers over existing ones. “They introduced complexity into the proposition that can influence our customers from making the right financial decisions in favour of short-term incentives.”

Brown says the focus is on like-for-like refinancing and using technology to ensure a fast and seamless process for brokers and their customers.

Customer retention and acquisition

Fedder’s advice to brokers is to ensure they are guided by the best interests duty framework when seeking to retain or attract new customers. “By doing this, you make sure the customers’ priorities are always front of mind,” he says.

“Don’t underestimate an early discussion with your BDM. They’re your best resource to confirm the lender’s offering is the right fit for the customer. BDMs also support brokers to structure the loan to deliver a great experience for their customer.”

Brown says customers are increasingly turning to brokers as trusted advisers who can assist them in sourcing a home loan that suits their needs. “Brokers have been doing a great job of supporting customers in getting great outcomes for their home lending needs.”

Brokers working to attract and retain customers in this evolving environment need tools and support from lenders, Brown says, so NAB has invested in technology to ensure fast and seamless processes, great products and policies, and competitive pricing and offers for every customer.

Smith points out that no matter their circumstances, customers want to deal with brokers who understand their needs, provide accurate information and explain loan options clearly. “Whilst borrowers are reviewing their loans more regularly, they still value the support, choice and convenience that brokers have to offer,” she says.

“We’ve seen that some brokers are increasingly working with self-employed customers,” Smith says. “Where these customers have a home lending need, we have a range of income verification options for self-employed applicants.”

For new customers, Baumann says brokers also add value through their knowledge and ability to consider various lenders that might suit a customer’s needs. “This knowledge extends past just home loan products and includes knowledge of the unique offerings from different lenders.”

Gibson says brokers are always conducting health checks with their customers, and he highlights the importance of doing this on a regular basis.

Gibson says brokers who provide excellent pre- and post-settlement customer service invariably get referrals for new business from their existing clients.

Technology boosts speed and efficiency

Baumann says CommBank has a range of tools to help broker partners best serve their customers. The bank recently launched FASTRefi® for brokers, which means eligible OFI loans can be refinanced within a few days of receiving a customer’s signed loan documents.

“Thanks to FASTRefi®, customers can obtain their new CommBank home loan within days of the bank receiving the customer’s signed loan documents.”

For existing customers, brokers can take advantage of Your Loans – a new self-service tool in CommBroker providing greater port-folio visibility, including each customer’s key post-settlement information all in one place. Baumann says recent Your Loan enhancements allow brokers to filter their customers based on their fixed rate maturity dates and get an overview highlighting any discounts customers may be eligible for.

Smith says ANZ has several streamlined processes for brokers to ensure fast and efficient refinancing. These include Simpler Switch, which provides a faster turnaround time for brokers’ customers, with less paperwork. Using comprehensive credit reporting to verify the customer’s ability to repay their existing commitments means there is no need to supply any income documents as part of an eligible application.

Self-employed customers with both business and home lending needs can take advantage of ANZ’s Rapid Refinance process, providing a single decision point for assessment when refinancing both business lending (up to $1m) and home loans, Smith says.

“We’ve also introduced new tools for brokers so that we can continue working better together to deliver for home loan customers. For example, ANZ’s Broker Chat service is now available to support broker home loan enquiries from submission to post-settlement.”

Brown says NAB has made significant investments in technology. “Our investment in a digital self-serviced capability enables customers to make simple changes such as fixing and splitting loans on their own via the NAB app.”

Recent enhancements to the Instant Pricing Tool streamline the process for brokers repricing NAB home loans by pre-filling existing customer and account information to make submissions more accurate and quicker to complete.

With economic conditions and customer circumstances changing rapidly, Brown says brokers have an important role to play in ensuring their customers continue to get great outcomes from their home lending.

“As the bank behind the broker, NAB is constantly improving its processes to make life easier for brokers so they can focus their energy on their businesses and building long-lasting relationships with customers.”

Fedder says Suncorp Bank offers FASTRefi®, an alternative to traditional refinancing that helps eligible customers move to their new loan sooner by funding the outgoing loan prior to settlement.

“Customers can start experiencing the benefits of the new loan sooner, be that a more competitive rate or loan features that are better suited to their needs,” Fedder says. Suncorp Bank also offers an Instant Pricing Tool, he says. This is available on the Suncorp Broker Portal and helps brokers quickly access the best discretionary price for new personal home lending.