Rising costs, shrinking order books and borrowing headwinds push sector deeper into contraction

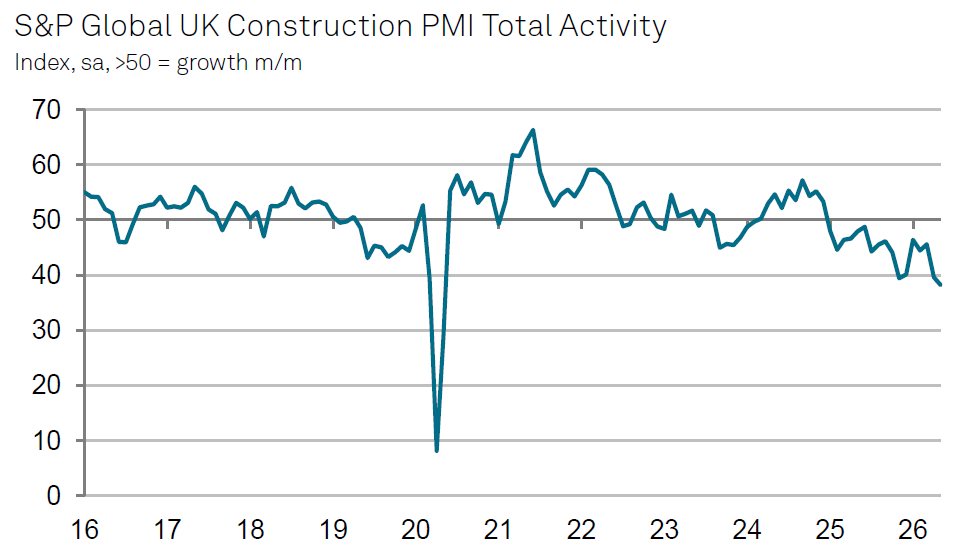

UK construction activity fell sharply in May 2026, with the pace of decline accelerating to its steepest since May 2020, according to the S&P Global UK Construction Purchasing Managers' Index (PMI).

The headline PMI dropped to 38.2 in May from 39.7 in April, remaining below the neutral 50 mark for the 17th consecutive month. Excluding the early pandemic period, the reading represents the sharpest contraction since March 2009.

Source: S&P Global PMI

Source: S&P Global PMI

Housing was the weakest segment, with its activity index registering 36. Survey respondents pointed to difficult market conditions and the continued drag from elevated borrowing costs — a factor of direct relevance to the mortgage sector, where reduced housing starts and transactions have downstream implications for lending volumes.

Commercial construction followed at 39, weighed down by client caution amid geopolitical tensions and inflationary pressure. Civil engineering recorded an index of 36.2.

New orders fell at the fastest pace in six years, with firms citing project deferrals, reduced client budgets and fewer tender opportunities. Some respondents also noted that domestic political uncertainty had dampened demand. Energy sector and power networks projects were identified as a positive exception for infrastructure work.

Input price inflation accelerated to its highest rate since June 2022, driven by fuel surcharges, rising energy costs and higher transportation bills. Subcontractor charges rose at the steepest rate in nearly three-and-a-half years. Almost two-thirds of the survey panel reported higher input costs in May, with only 1% recording a decline.

Supplier delivery times lengthened for the third successive month, with the deterioration in vendor performance the most marked since December 2022. International shipping delays and raw material shortages were cited as the principal causes.

Employment fell and input purchasing declined sharply, with the drop in procurement activity the steepest since November 2025.

Forward-looking sentiment remained technically positive — around 31% of respondents expect output to rise over the next 12 months, against 25% forecasting a decline — but overall business confidence fell to its second-lowest level since December 2022.

"UK construction companies reported a steep downturn in business activity during May, with the speed of contraction accelerating to its fastest for six years," said Tim Moore (pictured right), economics director at S&P Global Market Intelligence. "House building remained especially subdued, and there were fresh challenges in the construction sector from a considerable softening of commercial activity since April.

"UK construction companies reported a steep downturn in business activity during May, with the speed of contraction accelerating to its fastest for six years," said Tim Moore (pictured right), economics director at S&P Global Market Intelligence. "House building remained especially subdued, and there were fresh challenges in the construction sector from a considerable softening of commercial activity since April.

"Anecdotal evidence suggested that economic uncertainty and rising inflation in the wake of the Middle East conflict had triggered the steepest drop in new work since the beginning of the pandemic. Elevated borrowing costs were also reported to have impacted market conditions. Fuel surcharges and rapid increases in prices for energy-intensive raw materials continued to be felt across the construction supply chain. Overall purchasing costs rose to the greatest extent since June 2022, while international shipping delays meant that suppliers' delivery times lengthened for the third month running.

"Concerns about a prolonged decline in construction order books, alongside unfavourable near-term UK economic prospects, weighed on business optimism in May. This index has fallen sharply since the start of 2026, and confidence levels are now almost as low as those seen ahead of last autumn's Budget."

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.