High street banks increasingly favour large corporate and M&A lending

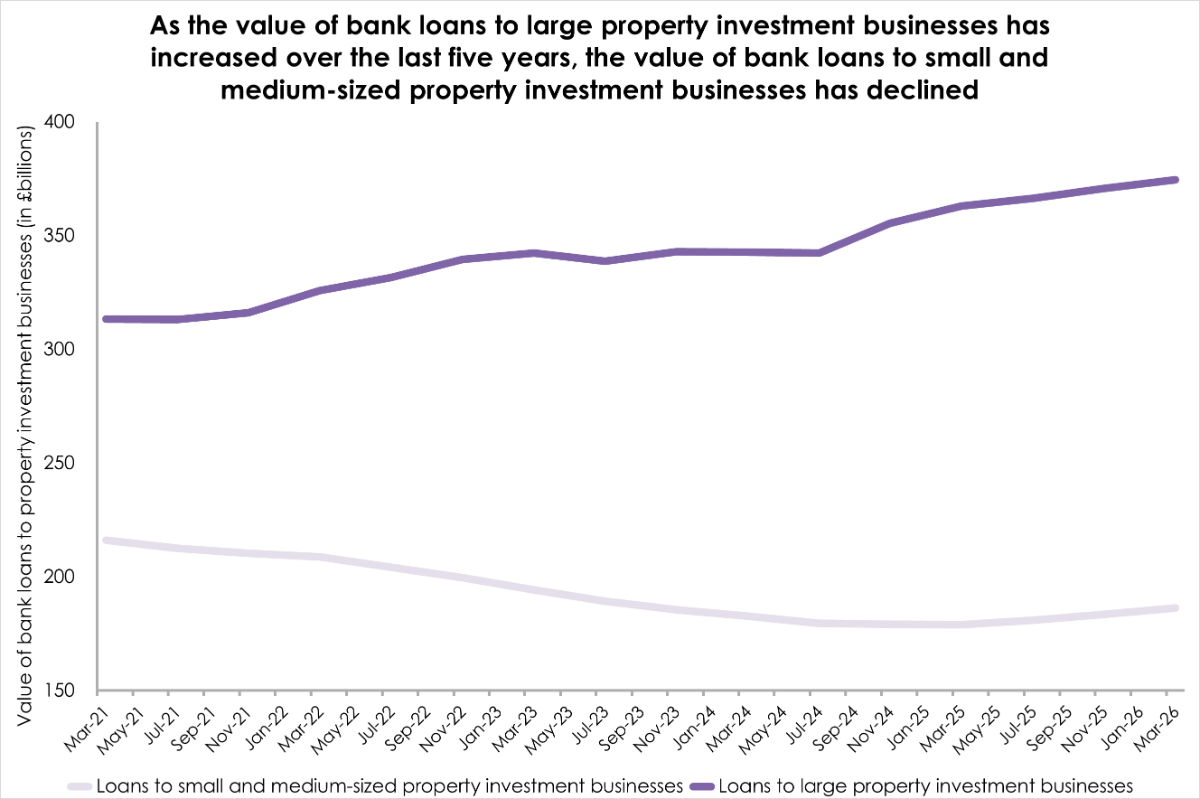

Lending from UK-regulated banks to small and medium-sized property investment businesses fell by 14% over the past five years, according to new research from specialist real estate debt and insurance advisory firm Karis Capital.

The sutdy shows that bank lending to this segment stood at £186 billion as of 31 March 2026, down from £216 billion on the same date in 2021.

Karis Capital said the decline reflects how banks' internal risk models tend to classify smaller property investors as higher risk, restricting their access to finance. This applies across high-street, challenger and boutique banks.

Much of the lending that has moved away from small investors has gone instead to large property investment firms, whose bank borrowing increased by 20% to £375 billion over the same five-year period.

The fall in lending to smaller investors coincides with a period of declining property prices, which the firm said has created buying opportunities. In the year to 31 March 2026, average property prices dropped by 20.2% in the City of London, 11.3% in Westminster and 7.5% in Kensington and Chelsea.

Karis Capital also noted that over the same five years, high-street banks have increasingly focused their lending on large corporate transactions and major mergers and acquisitions, often working alongside private equity firms.

“Smaller property investors should look beyond banks to take advantage of falling property prices,” said Nicholas Christofi (pictured right), chief executive of Karis Capital. “The market is currently offering very attractive buying opportunities but many smaller property investors are finding their usual lenders are less willing to lend

“Smaller property investors should look beyond banks to take advantage of falling property prices,” said Nicholas Christofi (pictured right), chief executive of Karis Capital. “The market is currently offering very attractive buying opportunities but many smaller property investors are finding their usual lenders are less willing to lend

Christofi said non-bank lenders that commonly provide finance to property investors include specialist lenders, bridging lenders and family offices.

“Non-bank lenders are often happier to lend in smaller lot sizes and are much more open to bespoke finance deals,” he said.

“Our view is that if you want to get the most competitive finance then you need to look at all the lenders and not just the bigger banks. Many banks prioritise larger lending deals and they see that as a more efficient way of deploying their capital.”

Separate figures cited by Karis Capital show that outstanding bridging loans in the UK rose by 30% during 2025, reaching £13.4 billion, up from £10.3 billion the previous year. Bridging loans provide short-term finance and are typically used by borrowers who have limited access to mainstream bank funding.

The specialist mortgage market is forecast to grow by 68%, from £32 billion in 2023 to £54 billion by 2029. Specialist lenders generally serve borrowers with non-standard circumstances, including the self-employed and those with impaired credit histories.

“The boom in the UK bridging market and specialist mortgage market shows that alternative funding providers are willing to step in for smaller investors,” Christofi said.

Karis Capital also pointed to reports that a number of buy-to-let landlords have been selling properties at reduced prices following the introduction of the Renters' Rights Act.

“Specific events in the property market mean a significant number of property assets are currently being sold at reduced prices,” Christofi said. “That window of opportunity is unlikely to remain open indefinitely.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.