Now more than ever, clients need brokers to close deals fast

Time is running out for first-time buyers looking to save thousands on stamp duty, and brokers play a crucial role in getting these deals over the finish line before the March 31 deadline.

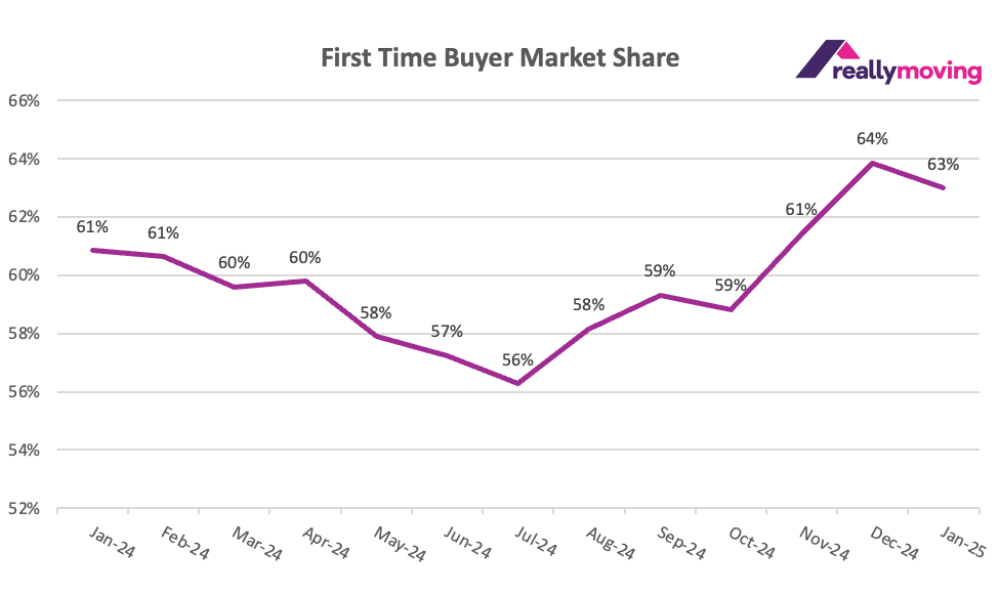

New data from comparison site reallymoving shows that first-time buyers accounted for a record 64% of home mover activity in December 2024 and 63% in January 2025, as buyers rushed to complete before higher tax bills kick in.

Despite affordability challenges, falling mortgage rates and the looming tax changes have driven a surge in demand. However, with average conveyancing times now stretching to 151 days — nearly five months — those not already deep into the process may struggle to complete in time. That means brokers should be urging clients to move quickly and ensuring all paperwork is in order to avoid delays.

Despite affordability challenges, falling mortgage rates and the looming tax changes have driven a surge in demand. However, with average conveyancing times now stretching to 151 days — nearly five months — those not already deep into the process may struggle to complete in time. That means brokers should be urging clients to move quickly and ensuring all paperwork is in order to avoid delays.

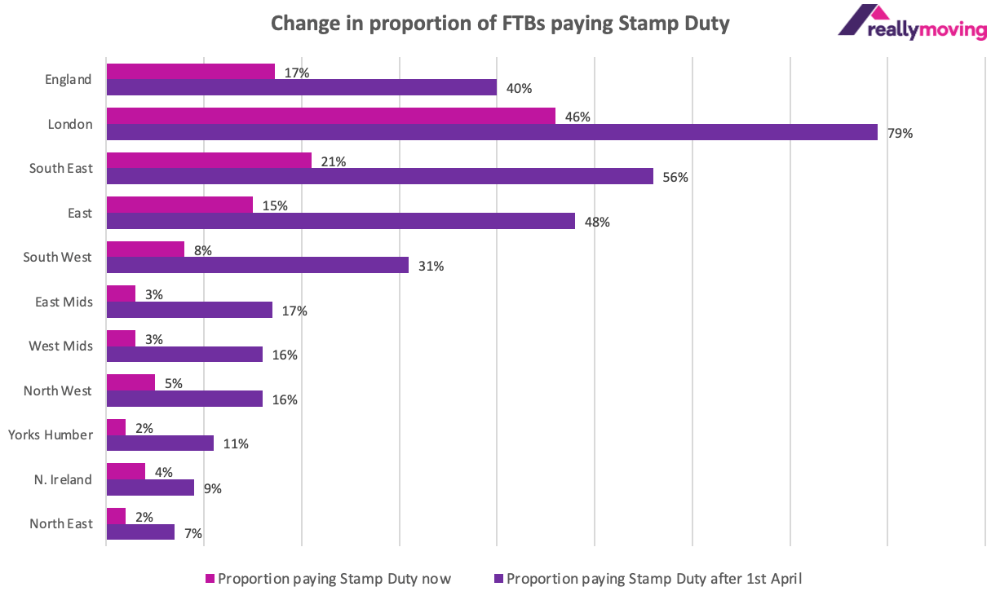

From April 1, the stamp duty threshold for first-time buyers will drop from £425,000 to £300,000, significantly increasing the number of buyers liable for the tax. Nationwide, the proportion of first-time buyers paying stamp duty is expected to rise from 17% to 40%.

The impact will be even more pronounced in high-cost areas. In London, where the average first-time buyer property costs £438,442, stamp duty bills will jump from just £672 to £6,922. The proportion of first-time buyers paying the tax will soar from 46% to 79%. In the South East, where the average price for first-time buyers is £330,441, stamp duty costs will increase from zero to £1,522, affecting 56% of buyers.

The impact will be even more pronounced in high-cost areas. In London, where the average first-time buyer property costs £438,442, stamp duty bills will jump from just £672 to £6,922. The proportion of first-time buyers paying the tax will soar from 46% to 79%. In the South East, where the average price for first-time buyers is £330,441, stamp duty costs will increase from zero to £1,522, affecting 56% of buyers.

Brokers should be preparing clients for these changes now — whether that means expediting current applications or advising new buyers on budgeting for higher costs.

While stamp duty changes add pressure, mortgage conditions are improving. Rates fell throughout 2024, with the lowest available two-year fixed rate currently at 4.2% and five-year deals at 4.07%. A potential base rate cut in February could push borrowing costs even lower, increasing lender competition as the spring market heats up.

There’s also speculation that regulators may ease lending rules to support the government’s pro-growth agenda. If debt-to-income caps are loosened, first-time buyers could access larger loans — an important development for those struggling to save enough for a deposit.

First-time buyers already face a tough challenge, with research from reallymoving showing it takes an average of 6.5 years to save for a home — assuming a 10% monthly savings rate. With the UK’s average first-time buyer home priced at £293,174, that means scraping together £25,554 for a 10% deposit, plus additional costs for conveyancing, surveys, and removals.

Rob Houghton (pictured), founder and chief of reallymoving, warned that delays in the homebuying process could leave many first-time buyers disappointed.

“The homebuying process continues to take much longer than it used to, and conveyancers have a very busy and stressful few weeks ahead of them,” he said. “If you’re buying at over £300,000 and you’re not already well advanced in the conveyancing process, don’t just hope for the best. Make absolutely sure you have flexibility in your budget to accommodate higher bills.”

For brokers, this is a critical moment to step in and guide clients through the final stretch. With significant savings on the line and time running short, proactive support can make all the difference in getting these deals completed before the deadline.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.