Examining the challenges of homeownership and a possible solution

The following article has been provided by Nicolas Singh, co-founder at Jrny.

The challenges of homeownership

It is more than just a popular sentiment – homeownership represents real financial security for those who purchase property. For many, it forms a core part of life’s journey. A recent government survey* revealed that 90% of Britons shared the dream of owning their own home, yet 60% of renters and adults believed that they never would.

Several barriers have made homeownership out-of-reach for some, ranging from rising property prices and stagnating wages to a, some would say, outdated mortgage system. The UK is facing an unprecedented homeownership crisis, with no obvious solution. This has given birth to various new homeownership alternatives, the latest being rent-to-own.

What is Rent-to-Own?

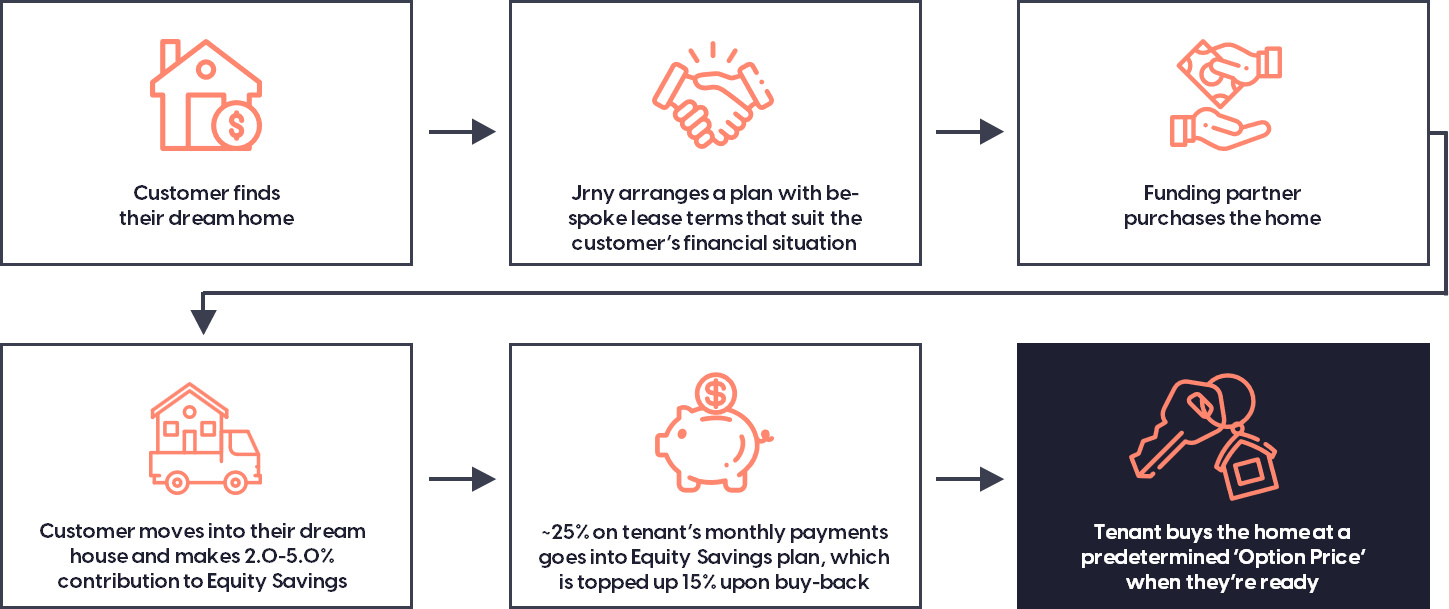

Rent-to-own (using Jrny’s Accelerated Ownership Plan as an example) allows aspiring homeowners to choose their dream home with a 2% deposit, whereby the platform’s funding partner will cash-buy the home and subsequently rent it back to them for a period of three to eight years. A portion of the customer’s monthly payments (about 25%, depending on plan design) go into an ‘Equity Savings’ account, helping them save towards their mortgage deposit. The plan is preparing customers to be mortgage ready and buy the home back from Jrny’s funding partners at a pre-agreed price at the end of the lease.

The model has seen widespread adoption in the US, for example, Divvy Homes and Home Partners of America, both of which have supported thousands of aspiring homeowners. It has proven to be a viable path to homeownership for customers who cannot buy their home using traditional means.

How can rent-to-own help mortgage advisers?

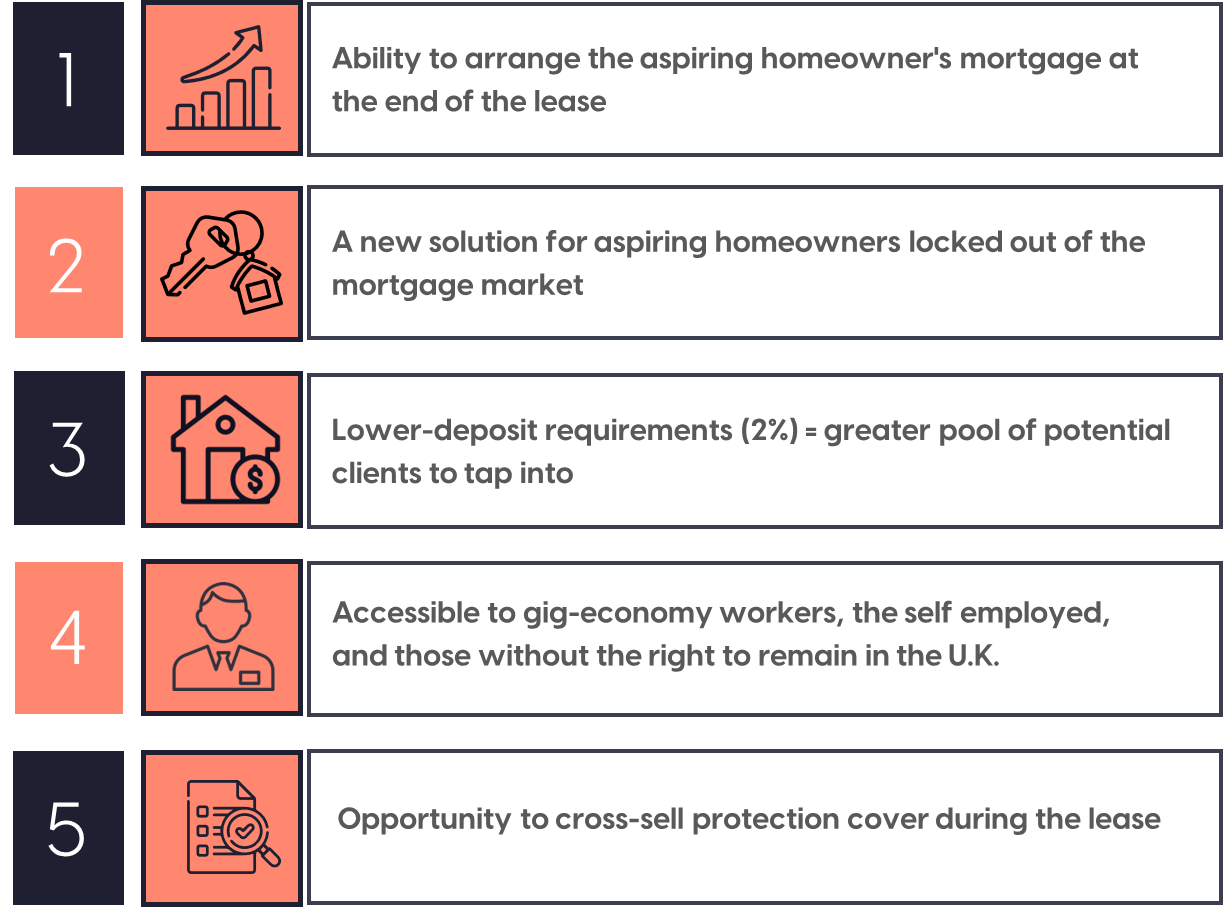

The scheme allows advisers to find a solution for aspiring homeowners who do not fulfil usual criteria. This includes those, despite being credit worthy, who are denied a mortgage from traditional providers as a result of their inability to meet minimum deposit requirements and/or access a sufficient mortgage loan amount due to affordability requirements. Additionally, rent-to-own seeks to help individuals who have been locked out of the standard mortgage system, such as gig-economy workers (**who, it’s estimated, represent 15% of the entire UK workforce today), the self-employed, and even customers who do not yet have the permanent right to remain in the UK.

The goal of the rent-to-own plan is to allow customers to live in their future homes already, while they save up towards affording a mortgage deposit. In the case of Jrny, customers initially need 2% and build up towards a 10% deposit, allowing them time to improve their credit or otherwise prepare for homeownership. Mortgage advisers would benefit throughout the duration of the plan from rent-to-own customers who require protection cover during their tenancy, and the arrangement of a mortgage at the end of it to purchase the home outright.

This is a real opportunity for advisers to serve more clients through rent-to-own in 2023, when deposit requirements & affordability are likely to continue to be an obstacle to homeownership.

Rent to own with Jrny

To get early access and find out more about Jrny, visit its website at www.joinjrny.com or send an email to [email protected].