Curious about the highest and lowest mortgage rates in the UK? Here is everything you need to know about London’s historical mortgage rates

Updated 28 August 2024

When the Bank of England (BoE) makes an adjustment to its rates, the mortgage sector quickly responds. Banks and mortgage lenders make changes to their interest rates and their home loan products reflect the BoE’s fluctuations. In turn, mortgage brokers and homeowners in the United Kingdom are also greatly affected when the BoE makes a move.

Over the past decades, mortgage rates have continued to rise and fall as a reaction to London’s ever-changing economy. This also led to changes in the key players within the mortgage market and the real estate industry.

In this article, Mortgage Introducer will explore historical mortgage rates in the UK as well as the highest and lowest rates ever recorded. We will also discuss how the BoE’s base rate affects these figures and other important factors. Want to know why mortgage rates were skyrocketing in the ‘80s? Read on to find out.

Historical mortgage rates in the UK

The difference between the historical highs and lows of mortgage interest rates has fluctuated wildly over the past years. But most short-term changes do not impact mortgage borrowers since many of them are on a fixed-term mortgage.

In fact, more than half of mortgage borrowers in the UK are on a fixed-term mortgage. In 2019, for instance, more than 90% of new mortgage borrowers chose a fixed-term mortgage. Changes in mortgage rates for the following mortgage loans were made as bank rates go up and down:

- 2-year fixed rate mortgage

- 3-year fixed rate mortgage

- 5-year fixed rate mortgage

- 10-year fixed rate mortgage

- 2-year variable rate mortgage

Check out this table from 2000 to 2024 on changes in mortgage rates:

|

Year |

2-Year Fixed |

3-Year Fixed |

5-Year Fixed |

10-Year Fixed |

2-Year Variable |

|

2000 |

6.50% |

6.20% |

6.00% |

6.50% |

6.30% |

|

2001 |

5.80% |

5.60% |

5.50% |

5.90% |

5.70% |

|

2002 |

5.20% |

5.00% |

5.00% |

5.30% |

5.10% |

|

2003 |

4.80% |

4.60% |

4.50% |

4.90% |

4.60% |

|

2004 |

4.50% |

4.30% |

4.30% |

4.60% |

4.20% |

|

2005 |

4.40% |

4.20% |

4.20% |

4.40% |

4.10% |

|

2006 |

4.60% |

4.40% |

4.40% |

4.60% |

4.30% |

|

2007 |

5.00% |

4.80% |

4.80% |

5.00% |

4.70% |

|

2008 |

6.00% |

5.80% |

5.70% |

6.00% |

5.60% |

|

2009 |

4.00% |

3.80% |

3.70% |

4.00% |

3.60% |

|

2010 |

3.50% |

3.30% |

3.30% |

3.60% |

3.20% |

|

2011 |

3.80% |

3.60% |

3.50% |

3.90% |

3.40% |

|

2012 |

3.60% |

3.40% |

3.40% |

3.70% |

3.20% |

|

2013 |

3.50% |

3.30% |

3.30% |

3.60% |

3.10% |

|

2014 |

3.40% |

3.20% |

3.20% |

3.50% |

3.00% |

|

2015 |

3.20% |

3.00% |

3.00% |

3.30% |

2.80% |

|

2016 |

3.10% |

2.90% |

2.80% |

3.20% |

2.60% |

|

2017 |

3.00% |

2.80% |

2.70% |

3.10% |

2.50% |

|

2018 |

2.90% |

2.70% |

2.60% |

3.00% |

2.40% |

|

2019 |

2.80% |

2.60% |

2.50% |

2.90% |

2.30% |

|

2020 |

2.70% |

2.50% |

2.40% |

2.80% |

2.20% |

|

2021 |

2.60% |

2.40% |

2.30% |

2.70% |

2.10% |

|

2022 |

3.50% |

3.30% |

3.20% |

3.60% |

3.10% |

|

2023 |

3.50% |

4.80% |

4.70% |

5.10% |

4.60% |

|

2024 |

4.70% |

4.50% |

4.40% |

4.80% |

4.30% |

Table data source: Statistica

Find out more about fixed mortgages vs variable rate mortgages through our interview with a mortgage expert.

Fixed-rate mortgages

A fixed-rate mortgage is a home loan with an interest rate locked in for a certain period—usually two, three, five, or 10 years. In turn, homeowners in the UK with fixed-rate mortgages do not see any change to their mortgage payments in the short term. This is regardless of what is happening with the BoE and its interest rates overall.

Variable-rate mortgages

On the other hand, homeowners in the UK who have variable-rate mortgage will be most vulnerable to changes in the BoE’s interest rate. However, fluctuations in the market may not necessarily cost those homeowners a lot. Many variable-rate mortgage products in the UK include features like interest rate caps or collars. This limits how high the rate can rise and how much it can fluctuate.

In addition, the BoE tends to adjust interest rates gradually. The BoE also considers two things before making any changes: the potential impact on every UK mortgage borrower and the broader economy in general.

Learn more about variable-rate mortgages and other types of mortgages available in the UK by reading this article.

What is the highest historical mortgage rate in the UK?

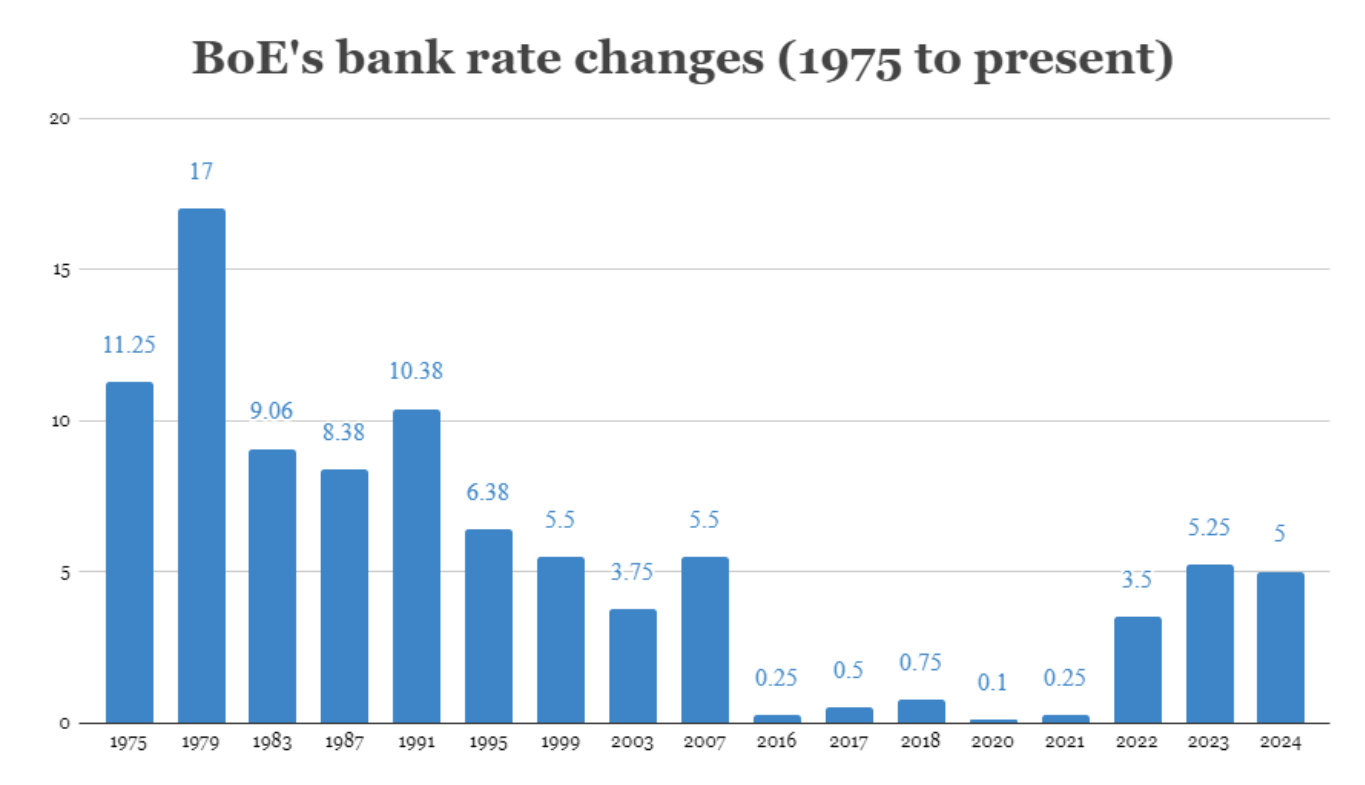

The highest historical mortgage rates in UK history were in 1979 when interest rates reached a whopping 17%. According to the BoE, the interest rate was at 5.5% in October 1977 before rising to 12.5% by the end of 1978. Throughout 1979, the interest rate rose gradually to 17%.

To understand why the highest historical mortgage rate came to be, one must understand how the UK housing market works. Watch this video to learn more:

Why were historical mortgage rates so high in the ‘80s?

Margaret Thatcher’s Conservative government raised the interest rates at the time to combat the rapidly rising inflation. These economic conditions led to a recession in 1980 and 1981. During this period, unemployment rose sharply. The manufacturing industries also took a significant hit. As a result of this crisis, the highest historical mortgage rates were recorded.

What is the lowest historical mortgage rate in the UK?

From the ‘80s until recent years, the average mortgage interest rate was at its lowest at 0.10% in March 2020. This is when the COVID-19 pandemic hit, and the UK real estate market was heavily impacted.

As the country and the rest of the world tried to go back to pre-pandemic times, the mortgage interest rates in the UK have fluctuated in accordance with the BoE base rate.

Historical mortgage rates in 2023

In May 2023, the BoE raised the bank rate by 25 bps to 4.50%, which was the 12th consecutive time and was in line with market expectations. Borrowing costs were at new highs which we have not seen since 2008, with the UK’s central bank battling double-digit inflation.

On June 2023, Nationwide Building Society and Atom Bank Plc announced increases in mortgage rates, joining a flurry of UK lenders who were hiking prices in response to inflation.

“With the continued upward trajectory of swap rates in recent times and lenders across the market increasing rates, we are having to make some increases across our fixed-rate mortgage range,” a spokesperson for Nationwide said.

“These changes are in line with the movement in swap rates and ensure that, as a building society, we can continue lending to all types of borrowers.”

The Nationwide Building Society has an exclusive platform for intermediaries. Check out this guide to Nationwide for Intermediaries.

What economic factors affect mortgage interest rates?

Your actual mortgage interest rate will result from various elements such as the mortgage product you choose as well as your mortgage lender. In addition, there are economic factors that have an impact on your mortgage rate.

The most notable among these factors is the BoE’s base rate, which is itself impacted by other economic factors. As we have seen during the pandemic, the movement of the BoE’s base rate is highly affected by the UK’s current inflation.

However, the BoE’s base rate does not only affect mortgage rates. It also affects a wide range of financial products from mortgage lenders and other related institutions. The base rates have an impact on the British pound as well.

When does the BoE review its base rate?

The BoE reviews its base rate on the first Thursday of every month. It could be changed depending on the rate of spending in the UK economy. For instance, if spending is deemed too low, the BoE will decrease the base rate. Conversely, if spending is deemed too high, the central bank will increase the base rate.

Here is a comparative bar graph of the BoE’s bank rate changes from 1975 up to the present:

How does the BoE’s base rate affect historical mortgage rates?

The BoE base rate is the rate of interest which it can charge to other lenders when they borrow money. That means when the BoE’s interest rate is higher, it will cost lenders more to offer products such as mortgages.

This means that the BoE’s base rate has the most prominent effect on mortgage rates. If the base rate climbs, so do the rates set by banks and mortgage companies. To simplify, the BoE base rate is reflected in the mortgage rate.

To know more about how the BoE bank rate affects the mortgage rate, watch this video:

Before committing yourself to applying for a mortgage to buy a house in the UK, do your research. You can check in on what the top mortgage brokers and lenders in your area can do for you. To start, find the right broker and lender for you on our Best in Mortgage page.

Impact of historical mortgage rates for mortgage professionals

The historical mortgage rates in the UK have a direct impact on mortgage professionals, particularly for mortgage lenders and brokers. When BoE sets the bank rates, banks and mortgage lenders follow suit. They adjust their interest rates based on the changes.

As for intermediaries, these changes in the home loan offerings from various lenders affect their work. They need to be updated with the latest mortgage deals to cater to their clients and maintain their level of service.

While it is important to keep up with the changing economic and mortgage markets, it is equally important to understand how we got here by learning about the historical mortgage rates in the UK. That way, home buyers will be able to make the most informed decision when it comes to getting a mortgage.

What do you think of the historical mortgage rates in the UK? Do you have any experience navigating fluctuating rates? Let us know in the comment section below