Mainstream momentum powers ahead for alt-doc financing, with rising self-employment and narrower pricing gaps creating fertile ground for volume growth

Alt-doc lending is having a makeover. It's shedding its image as a high-risk category to reveal what is, at its core, an essential lending pathway for millions of hardworking Australians.

While this is a trend with a few years behind it, shifting borrower behaviours and a more conservative traditional credit market have further entrenched alt-doc into the lending mainstream.

Take Brighten Home Loans, where application volumes for alt-doc residential products rose 195% over the past 12 months. Chris Meaker (pictured, top of page, right), head of sales and distribution at Brighten, argues the growth is being driven by two converging forces: a steady rise in non-traditional employment and an increasingly narrow credit appetite among the major banks.

"Recent Australian Bureau of Statistics (ABS) data shows a 4.9% increase in non-employing businesses, reflecting the continued expansion of the self-employed segment, including sole traders, contractors, consultants and owner-operators," Meaker says. "At the same time, lending standards across the major banks have continued to tighten, particularly around income verification and serviceability for self-employed borrowers." The result, he says, is that alt-doc has shifted from being a niche workaround to a mainstream tool. Brokers who once viewed it as a last resort are now reaching for it as the most logical first option for clients whose income structures simply don't fit a standard PAYG assessment.

At ORDE Financial, co-founder and managing director Ryan Harkness (pictured, right) says demand has remained strong over the past 12 months, driven by a self-employed borrower base with income that simply doesn't present neatly under standard full-doc assessment.

The scale of that market is substantial. ORDE's Outlook Australia research, developed alongside demographer Bernard Salt, points to approximately 1.97 million tradies nationally, with around 374,000 operating as owner-managers.

These borrowers are often financially strong, Harkness says, but their cash flow moves with jobs, invoices, materials and payment timings in ways that don't always align with conventional assessment models.

"The opportunity for non-banks is not just to provide the product but to provide brokers with a clearer, faster and more practical way to assess these borrowers responsibly and deliver better customer outcomes," says Harkness.

Around one in three customers at Pepper Money uses an alt-doc loan option – a statistic that reflects just how central the product has become to the lender's core proposition. Barry Saoud (pictured, top of page, left), chief executive of mortgages and commercial lending at Pepper Money, explains that more Australians are working for themselves, contracting, juggling multiple income streams or earning through gig work and side hustles, and conventional income verification simply hasn't kept pace.

"The workforce isn't standing still, and neither should lending," Saoud says. "Brokers need lenders who can keep pace with that change, with flexible options that help them support more customers who sit outside traditional lending boxes."

Alt-doc momentum has continued at Liberty, driven by a structural shift in how Australians earn income. With approximately two million Australians self-employed, and many more generating income through contracting, gig work or multiple streams, financially sound borrowers may still present as complex on paper. But that complexity is precisely what the alt-doc framework was built to address.

"Supporting self-employed and irregular-income borrowers isn't new," says Liberty group manager – residential Caesar Ibrahim. "Our income-assessment approach is designed to reflect true capacity."

Thinktank general manager sales Belinda Wright (pictured, top of page, centre), who works closely with brokers across Thinktank's Commercial Mid Doc and Quick Doc, Residential Mid Doc, SMSF Mid Doc and Private Loan products, says the growth isn't simply a function of banks pulling back. It reflects a more considered shift in broker behaviour – one where alt-doc is being selected because it genuinely fits the borrower's structure.

"Brokers are increasingly using alt-doc not as an exception but as a deliberate structuring choice," Wright says. "In many cases, our experienced BDMs and credit team are working alongside brokers early to help validate that fit, align verification requirements and provide clearer pathways before formal submission."

Bank credit appetite for self-employed borrowers has become increasingly selective, while borrower profiles have grown more complex – particularly among those operating through company or trust structures. That combination has pushed volumes towards specialist non-bank lenders equipped to assess income in ways that reflect how modern SMEs actually operate.

Tim Lemon, national sales manager at MA Money, notes that broker education has been central to the lender's alt-doc growth. "More brokers are recognising that alt-doc lending is not a one-size-fits-all product and that different types of self-employed customers require different approaches," he says. "Whether it's sole traders, company structures or trust borrowers, every alt-doc application is different. Understanding the different dimensions of self-employed income and assessing each scenario on its merits has helped build broker confidence and contributed to continued momentum in the space."

Responding to rate pressures

"Higher rates haven't dampened the appetite for alt doc – they've sharpened it," Ibrahim says. He explains how the borrower profile has shifted towards consolidating, restructuring or refinancing for serviceability, rather than buying for the first time. "While it may be a more complex customer profile than a standard PAYG purchase, that's exactly who the alt-doc framework was built to serve," Ibrahim continues. "Verification methods such as BAS, bank statements and accountant declarations help us underwrite confidently when the cash rate is moving, and a previous tax return doesn't tell the full story of where a small business is in 2026."

On the product side, Liberty has made several adjustments over the past year. Higher loan limits were introduced to reflect growth in property values, alongside an alternative to traditional lenders mortgage insurance. Longer loan terms were also brought in to improve serviceability for borrowers with fluctuating income streams.

Self-employed borrowers have become more purposeful in how they approach lending decisions, notes Harkness. They are focusing on refinancing, debt consolidation, business investment and cash flow management rather than simply chasing competitive pricing. "Alt-doc is a practical alternative-income-verification pathway that allows strong self-employed borrowers to access the same range of lending solutions as other borrowers, without being disadvantaged simply because their income is more complex," he says.

That framing – alt-doc as an income-verification pathway rather than a risk category – runs through ORDE's entire credit policy. The non-bank recently extended its residential prime offering to 85% LVR for both alt-doc and full-doc borrowers, a change Harkness says reflects a straightforward principle.

Meaker says the rate environment has shifted what borrowers care most about. Speed of approval, certainty of outcome and flexibility in income assessment have overtaken headline pricing as primary concerns for this cohort. "Demand for alt-doc solutions has increased as borrowers and brokers look for assessment methods that better reflect real-time income and business performance rather than historic financials," he says.

Saoud adds that higher rates have refocused borrower priorities sharply on the fundamentals: cash flow, repayment comfort and whether their current loan structure still fits their circumstances. For many, that means turning to alt-doc as a vehicle for refinancing, consolidating higher-cost debts, managing Australian Taxation Office (ATO) payment obligations or restructuring lending to create more breathing room.

"In a higher-rate environment, getting the assessment right really matters," Saoud says. "For us, flexibility is about having more ways to understand a customer's income and what their overall financial picture looks like, so we can structure lending that genuinely works for them."

Where product design still has room to improve

Much of the advancement of the alt-doc space is a result of the pricing gap between alt-doc and standard lending products narrowing sharply.

"The days of alt-doc ra tes sitting 2% above standard lending are largely gone," says Lemon (pictured, left). "Increased competition and greater confidence in self-employed lending have significantly narrowed the gap between bank and alt-doc pricing. As a result, more borrowers are considering alt-doc solutions, particularly self-employed customers who have strong income but don't meet traditional income-verification requirements."

tes sitting 2% above standard lending are largely gone," says Lemon (pictured, left). "Increased competition and greater confidence in self-employed lending have significantly narrowed the gap between bank and alt-doc pricing. As a result, more borrowers are considering alt-doc solutions, particularly self-employed customers who have strong income but don't meet traditional income-verification requirements."

Furthermore, alt-doc's flexibility around income assessment has become a feature rather than a footnote. Brokers are increasingly framing discussions around cash flow sustainability, interest-only options and buffer management – considerations that matter particularly where business income fluctuates across the rate cycle.

"Alt-doc products that provide flexibility around assessment and realistic servicing assumptions are more often positioned by brokers as a considered solution rather than a higher-risk alternative," Wright explains. Early scenario workshopping – often in collaboration with Thinktank's BDM team – helps ensure the lending solution remains appropriate across different rate environments, not just at the point of approval.

But despite the segment's maturity, Meaker acknowledges that alt-doc product design hasn't fully caught up with how modern Australians generate income. Income assessment for newer business models – contractors with multiple streams, rapidly scaling operators – remains one of the more persistent challenges.

"The opportunity lies in improving how real-time income and cash flow data is applied, rather than relying on static snapshots," says Meaker. "From Brighten's perspective, the next phase of innovation is about refining simplicity rather than adding features – delivering clearer policy settings, faster decisioning and more consistent outcomes."

Alt-doc construction lending is one area in which Brighten has invested. The lender has built a dedicated capability with defined progress payment processes and structured credit assessment, aimed at self-employed borrowers building homes or undertaking small-scale developments who lack the documentation to satisfy major bank requirements.

Lemon points to inconsistency across the industry as an ongoing challenge, particularly around specialist loan amounts, LVRs and self-employed policy settings. He says differing approaches to ABN history requirements – specifically how long a borrower needs to be self-employed before qualifying – remain one of the most significant gaps.

Accountant letter requirements are another friction point. "Accountants often need to work with different wording and formats depending on the lender, which can create unnecessary complexity for brokers and customers," Lemon says. Greater consistency across the industry, he argues, would meaningfully improve the alt-doc experience and broaden accessibility for self-employed borrowers.

Saoud acknowledges that while the industry has made significant strides, the friction in alt-doc hasn't been fully eliminated – it's just moved. The question is no longer whether lenders can support self-employed borrowers but how smooth and efficient that process is in practice. Pepper Money has targeted that gap directly with the launch of AltDoc Xpress – a fully digital workflow for self-employed financial declarations and accountant letter documentation designed to reduce paperwork and back and forth.

"The next stage for alt-doc is really about improving accessibility and usability, making it feel just as straightforward and intuitive as full-doc lending," Saoud says.

Misconceptions

The perception that alt-doc carries inherently higher risk has been tested by the sector's arrears performance, which has remained relatively contained across non-bank lenders. Liberty's view is that this reflects the maturity of the industry's assessment frameworks, not a loosening of standards.

"Alt-doc refers to the documentation type, not the rigour," Ibrahim says. "The verification methods used could provide a more current view of a borrower's cash flow than an older tax return alone."

Ibrahim points out that alt-doc loans have also typically been written at lower LVRs, with more selective property policies, and that stronger broker capability has played a significant role in maintaining portfolio quality.

The Australian Securities and Investments Commission's (ASIC) increased scrutiny of responsible lending in the non-bank space is, in Liberty's view, a reinforcement of what disciplined lenders already do. The focus on making the right credit decisions aligns with how Liberty approaches complex lending scenarios.

"Stronger scrutiny reinforces that alt-doc is a disciplined credit product, not a shortcut," says Ibrahim. "We embrace complex scenarios which drive us to work harder and help borrowers emerge in a stronger financial position after credit."

Saoud has the receipts to debunk the misconception that alt-doc loans carry higher risk.

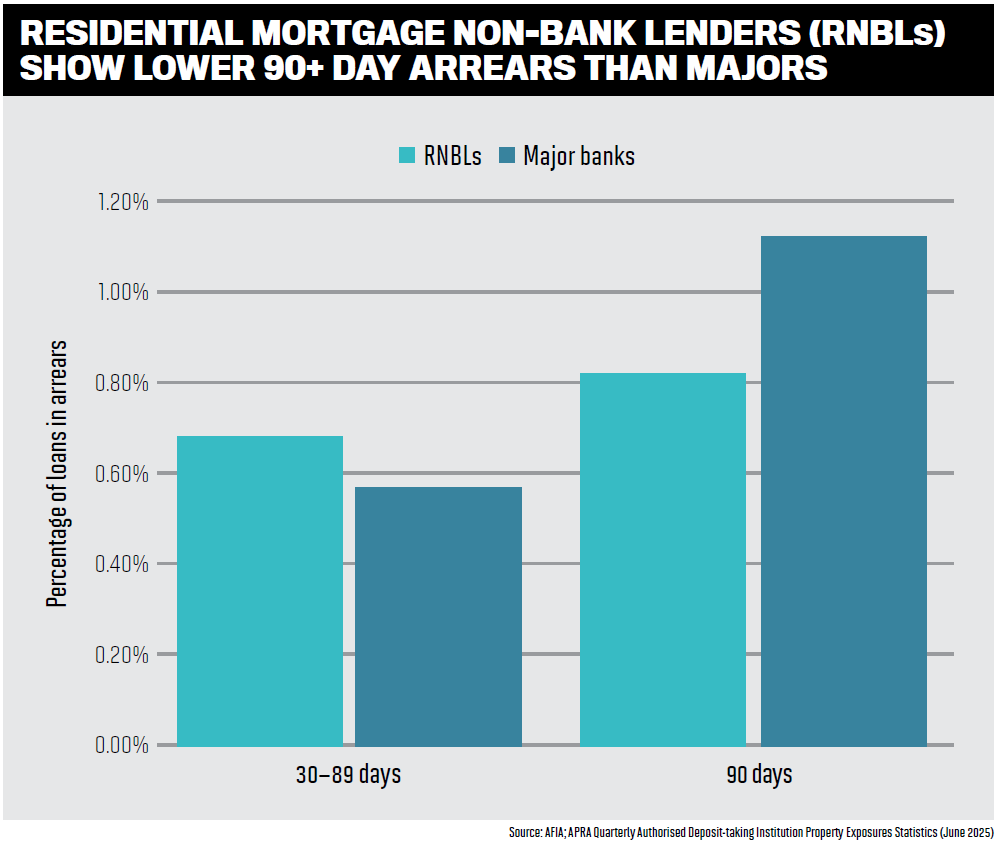

The Australian Finance Industry Association (AFIA) report on residential mortgage non-bank lenders, published in December 2025, shows registered non-bank lenders have an arrears profile broadly in line with the major banks, with 90-plus days' arrears and non-performing loans sitting at 0.81%, compared to 1.10% for the majors.

For Saoud, that performance reflects something important about how alt-doc works in practice. "Alt-doc lending isn't about relaxing credit standards," he says. "It's about having more ways to verify income and understand the customer properly, especially when someone's financial situation doesn't fit the standard traditional income documentation requirements."

If anything, alt doc demands more rigour, not less. "You need to understand the customer's business, their cash flow and overall financial position to make sure the loan is set up right from the start," says Saoud.

One of the more persistent misconceptions about alt-doc lending is that its different verification pathway implies greater borrower risk. Harkness pushes back on that characterisation, noting that arrears across the non-bank sector have remained relatively contained and that performance is shaped more by the nature of self-employment than by how income is documented.

Self-employed borrowers, Harkness argues, often have more capacity to respond to changing conditions than PAYG employees, even if their cash flow is less predictable at any given moment. Brokers are a critical part of that equation. Their understanding of the customer, loan purpose and broader circumstances helps educate clients on their obligations and supports appropriate structuring.

"The arrears experience suggests the industry is handling alt-doc distribution well where lenders stay close to brokers, maintain clear policy and focus on genuine borrower need rather than volume," he says.

The non-bank sector's relatively contained arrears performance in alt-doc has, in Wright's view, less to do with favourable conditions than with how risk is being managed. When borrower income is properly understood, structures are aligned from the outset and brokers engage early with lenders, alt-doc loans tend to perform consistently.

"Risk in alt-doc lending is more about holistic assessment discipline than product, policy or documentation labels," Wright says. That discipline is increasingly being supported by open banking and data-sharing tools, which Thinktank uses as complementary verification inputs rather than primary determinants. Wright says these tools can help verify assumptions and reduce submission friction, but "human review, context and professional judgement remain essential, particularly where multiple entities or irregular income streams are involved".

Responsible lending obligations, she adds, haven't altered that equation, and flexibility in alt-doc doesn't mean reduced accountability. "We place significant emphasis on understanding the purpose of the loan, the sustainability of income and the appropriateness of the structure," says Wright. "Clear documentation, early engagement and transparent assessment pathways all support compliance with everyone's responsible lending obligations. In practice, that balance is best achieved through collaboration."

How brokers can strengthen alt-doc submissions

"One of the biggest things we encourage brokers to remember is that it's a low-doc loan, not a low-information loan," says Lemon. "The more context and detail provided up front, the better the outcome can be for the customer."

Lemon often sees a lack of information around what the applicant actually does for a living and how their income is generated. Thorough notes around declared income, number of employees, online presence, business assets and the overall business profile "can make a significant difference in helping our credit team assess the scenario efficiently and accurately".

The most common submission errors at Brighten involve incomplete documentation, particularly accountants' letters where key fields – including confirmation of what documents were reviewed and how long the accountant has acted for the business – are left blank.

But "brokers shouldn't hesitate to submit alt-doc deals", Meaker says. "As long as the supporting documents are clear, complete and aligned with the scenario, the process is designed to be smooth and efficient."

Meaker also points to a broader responsibility that comes with the segment's growth. As Australian mortgage brokers increasingly rely on non-bank alt-doc as a default solution for complex self-employed clients, lenders must apply consistent credit discipline, not just chase volume. "Alt-doc lending needs to balance access with accountability, ensuring borrowers are not only able to get lending today but are well positioned to perform through different stages of the economic cycle," he says.

The most common submission errors Harkness sees aren't about documentation volume; they're about narrative clarity. "Good alt-doc lending is not about providing less information; it's about providing the right information to help us understand the borrower's real income, conduct and capacity," he says.

Wright's message is that the most successful alt-doc submissions start before the application, with a focus on structure rather than product. The most common causes of deal friction are incomplete disclosure or a misalignment between how a borrower actually earns income and how that income is presented on paper. Echoing Harkness's comment, she says, "Alt-doc isn't about less information – it's about the right information."

"When brokers engage early and work in collaboration with our BDMs and credit team, submissions always progress more efficiently, with clearer expectations and fewer surprises through the assessment process."

Ibrahim (pictured, right) adds that there remains a perception in the market that alt-doc loans are slow or difficult to execute – a view he believes doesn't reflect the reality. "With the right support, they're often very workable. Early engagement between the lender and broker makes the difference and gives brokers greater confidence when presenting options to borrowers. Brokers who workshop structure and servicing up front with our experienced BDM team could move forward with greater clarity."

Looking ahead

The Federal Budget has outlined an intention to support productivity and reduce regulatory burden for small businesses, highlighting the role the self-employed play in Australia's economy.

Self-employed Australians like those served by ORDE – tradies, contractors, owner-managers, business owners – are the same people contributing to Australia's productive economy.

"Once they have demonstrated capacity, conduct and a sustainable income position, they should be able to access appropriate lending solutions across a full range of purposes," Harkness says.

"The opportunity in alt-doc is therefore bigger than a product category."

Speaking of the Budget, Saoud points to the changes to discretionary trust minimum tax thresholds as a prompt for many small and medium businesses to reassess their broader financial structures – and an opportunity for brokers to have deeper conversations with self-employed clients about their long-term positions.

As the self-employed segment continues to grow, Pepper Money's view is that alt-doc lending won't recede. It will become an increasingly essential part of how brokers serve the modern Australian borrower.

Meaker expects demand to keep building as Australia's self-employment base grows and income structures become more varied. The lenders that will lead the next phase, he argues, will be the ones that combine specialist expertise with consistent, disciplined execution at scale. "Experience, consistency and service will separate the top lenders from the rest."

"Alt-doc will likely continue as a specialist solution within the broader lending landscape," continues Ibrahim. "It's an offering that requires skilled underwriting and should be entered into with consideration. As the category evolves, better data and verification tools may expand access. However, maintaining discipline in how they are applied will remain critical to long-term performance."

Lemon echoes that sentiment. "While alt-doc lending has become more mainstream as rates and fee barriers have reduced and lenders have become more comfortable with self-employed lending, it will likely remain a specialist category because no two self-employed borrowers look the same. For it to scale further, there would need to be greater consistency in assessment processes across the industry, although that's challenging given the range of business structures and income types involved."

Wright agrees. "Growth that is compliant by design, well structured and well understood will be far more sustainable than rapid expansion driven purely by market gaps."

On a final note, Lemon points to the market's expanding appetite as evidence of how far the segment has come.

Five years ago, many lenders capped alt-doc lending at around the $1.5 million mark – a ceiling that has since moved dramatically. "Today, we're lending up to $15 million," he says. "That reflects both growing demand and greater confidence across the market in assessing complex self-employed borrowers and larger-scale lending scenarios."

Lemon also flags open banking and data-sharing tools as a significant force shaping the next phase of alt-doc assessment. As real-time financial information becomes more accessible, he says, these tools are likely to play an even bigger role in simplifying the process for both brokers and borrowers.