What factors should you consider when getting professional indemnity insurance as a mortgage broker? Why is coverage important? An industry expert explains

- What is professional indemnity insurance and how does it work?

- Why do mortgage brokers need professional indemnity insurance?

- What does professional indemnity insurance cover?

- What does professional indemnity insurance not cover?

- How much does professional indemnity insurance for mortgage brokers cost?

- Where can mortgage brokers get professional indemnity insurance?

- What should mortgage brokers look for in professional indemnity insurance?

- Is professional indemnity insurance worth it?

As a mortgage broker, you play an important role in helping aspiring homeowners find a home loan that suits their financial situation. Your advice and expertise are crucial in helping clients make informed decisions.

Unfortunately, even with due diligence, mistakes can happen in your work. These lapses can prove costly, especially if the client decides to sue. This is why professional indemnity (PI) insurance is a must for mortgage brokers.

In this guide, MPA delves deeper into this form of protection. We will discuss how it works and how much coverage you need. We also talked to an industry expert who will explain why PI coverage is a vital part of the profession and what you should look for when choosing a policy.

What is professional indemnity insurance and how does it work?

To give homebuyers the best advice, you need to do your job without the fear of unintended outcomes. This is the purpose of professional indemnity insurance.

Professional indemnity insurance is a type of policy that protects mortgage brokers against claims of financial losses resulting from negligence in providing advice and services. Coverage comes in two types:

- claims-made policy: covers claims only if the error occurs and the lawsuit is filed while the policy is in effect

- run-off policy: covers claims that happen during the coverage period, even if the charges are filed after the policy has lapsed

Depending on the provider, professional indemnity insurance is also called errors and omissions (E&O) insurance or professional liability insurance. In the healthcare sector, this type of coverage is called medical malpractice insurance.

Why do mortgage brokers need professional indemnity insurance?

Professional indemnity insurance is a legal requirement set by industry associations and regulatory bodies in Australia.

The Australian Securities & Investments Commission (ASIC) requires a minimum coverage of $2 million per claim and $2 million in aggregate as a condition for your licence. The Mortgage & Finance Association of Australia (MFAA) imposes the same PI limits for its membership and at least 12 months of run-off cover.

Brad Miller, general manager at BizCover, says that even if it wasn’t mandated, PI insurance would still be essential for mortgage brokers.

“Providing expert financial advice to clients comes with great responsibility,” Miller explains. “Even a small error carries the potential for great financial loss, and affected clients would understandably be dissatisfied with the brokers’ service, actioning negligence claims against them if that were to happen.

“Professional indemnity insurance helps protect mortgage brokers in cases where their professional advice and service are called into question.”

Our guide on how to become a mortgage broker outlines other requirements set by regulatory bodies.

What does professional indemnity insurance cover?

Professional indemnity insurance for mortgage brokers covers legal and settlement costs from service-related mistakes. These include:

Professional negligence

This takes place when you fail to perform your duties and obligations to a required standard. Some instances of professional negligence include securing your clients a mortgage that doesn’t fit their finances and paperwork errors that cause them to lose money.

Actual negligence doesn’t need to happen for you to get sued. If your clients felt that your actions cost them money, they could file a lawsuit against you.

Breach of contract

This happens when you break the agreed-upon terms and conditions of a binding contract. This includes failure to deliver a specific service stated in the contract, causing your clients huge financial losses.

Misrepresentation

Misrepresentation is when a mortgage broker makes a false statement that leads a client to agree to a contract. One example is giving inaccurate information on interest rates. This can cause homebuyers to agree to a home loan that they can’t afford. If misrepresentation is discovered, the affected party can void the contract and seek damages.

Professional misconduct

Professional misconduct happens when a mortgage broker breaks the rules or standards set by an industry association or regulatory body. This includes:

- withholding important information from clients

- breach of confidentiality

- failure to get a client’s informed consent

- inadequate documentation and record keeping

- working while impaired

- infringement of intellectual property rights

- slander, defamation, or libel

What does professional indemnity insurance not cover?

PI insurance should not be confused with other forms of liability coverage. Such policies provide protection against events that professional indemnity insurance for mortgage brokers don’t cover.

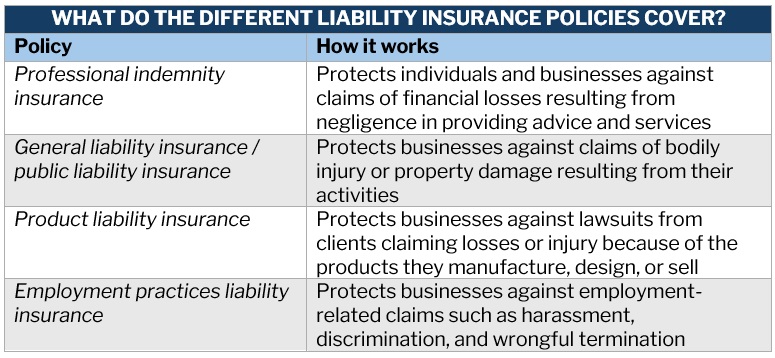

Public liability insurance

Also known as general liability insurance, this type of coverage protects businesses against claims of bodily injury or property damage resulting from their activities. These include accidents that happen within a business’ premises like slips and falls and spilling coffee on a client’s laptop.

Under this policy, businesses don’t receive compensation. Instead, the payouts are given to the affected parties. Without coverage, business owners would need to pay for the claims out of pocket.

Product liability insurance

Product liability insurance is designed for companies that manufacture or sell products. It protects them against lawsuits from clients claiming losses or injury because of their products. This policy pays for legal defence costs and covers third-party compensation if the company is found to be at fault.

Employment practices liability insurance

Also called EPLI, this type of coverage protects businesses against employment-related claims. These include wrongful termination, discrimination, and harassment. EPLI covers defence and settlement expenses.

Here’s a summary of the key differences between these liability insurance policies.

Professional indemnity insurance also doesn’t cover:

- intentional wrongdoings and criminal acts

- claims that occurred before the policy was issued

- regulatory fines and penalties

Getting professional indemnity coverage is one of the most important steps to protect your mortgage broking business. BizCover explains how.

How much does professional indemnity insurance for mortgage brokers cost?

Data gathered by BizCover shows that 90% of mortgage brokering services pay an average monthly premium between $68.46 and $82.07 for professional indemnity coverage. This is around $820 to $985 per year.

To come up with the figures, the Sydney-based online insurance brokerage analysed more than a thousand PI insurance policies it issued during the 2023 financial year.

BizCover considered business revenue, number of employees, and level of cover to get the cost estimates. More than four-fifths of mortgage brokers in the study have one or two employees and reported revenues of $250,000.

“Many factors can impact the pricing of a mortgage broker’s PI insurance,” Miller explains. “A quick and easy way for brokers to understand the cost of a policy for their business is to compare quotes from multiple insurers.”

Among the main factors that impact the cost of professional indemnity insurance for mortgage brokers, according to Miller are:

- business turnover and size

- the amount of insurance required

- the individuals being covered

- claims history

BizCover specialises in insurance for small businesses.

Where can mortgage brokers get professional indemnity insurance?

Most business insurance specialists in Australia offer professional indemnity coverage for different industries.

Many aggregators also offer group coverage for finance and mortgage brokers as part of their services and fee schedule. Some simply outline their requirements and refer you to an insurance broker or provider.

Professional indemnity insurance is just one of the several requirements for getting your mortgage broker licence. You will also need to get proper training. This guide to mortgage broker courses explains the different qualifications needed for the job.

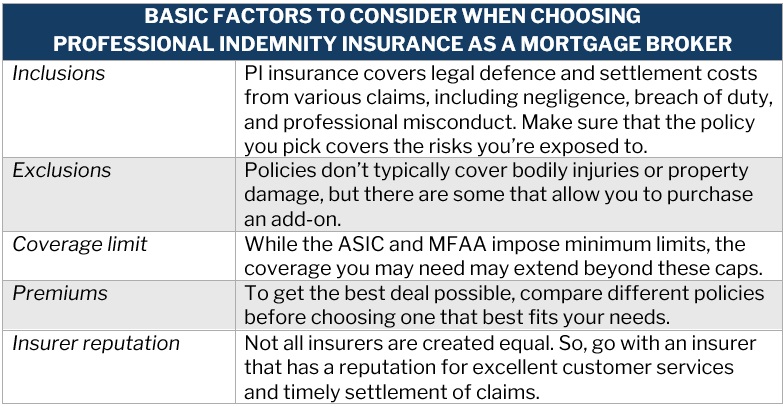

What should mortgage brokers look for in professional indemnity insurance?

BizCover offers professional indemnity insurance that meets ASIC’s RG210 and MFAA’s membership requirements. Each mortgage broker, however, faces a unique set of risks and may require coverage that extends beyond these industry minimums.

“Mortgage brokers should think carefully about their individual business risks and needs, rather than simply defaulting to cover minimums,” Miller says. “Some brokers could find themselves underinsured and [paying] out of pocket if they do not have enough cover for their business.”

Miller adds that when choosing a professional indemnity insurance policy, mortgage brokers should ask these questions:

- What are the potential risks to your business? What is the potential cost to fix any errors?

- If action is taken against you, how much would your legal fees and investigation costs be?

- Do any client contracts require a minimum level of cover?

- Is run-off cover included in the policy or available as an option if you stop trading?

Just like other types of insurance policies, there are several basic factors that you need to consider to find the right PI coverage for your needs:

Is professional indemnity insurance worth it?

Professional indemnity insurance is a requirement for getting a mortgage broker licence in Australia, so you don’t really have a choice. But even if it wasn’t required, industry experts recommend taking out coverage – and for good reason.

The nature of a mortgage broker’s job comes with several risks. Claims of negligence, inaccurate advice, and misrepresentation can result in massive costs. These can easily drain a company’s financial resources, whether they are proven liable or not. Professional indemnity insurance can protect you and your business financially from the huge expenses arising from lawsuits.

PI coverage also enables mortgage brokers to act in the best interests of their clients and businesses knowing they are protected even if they make a mistake.

Have you experienced relying on professional indemnity insurance as a mortgage broker? How did PI insurance help? We’d love to see your story below.