The big four banks discuss turnaround times, improvements to lending processes and why they are investing in the broker channel

The major banks have been under heavy scrutiny over the last few years, as mortgage brokers and customers lost trust following the banking royal commission. Not afraid to acknowledge that, the heads of third party at the big four joined MPA at a virtual roundtable to discuss how they are working to rebuild relationships.

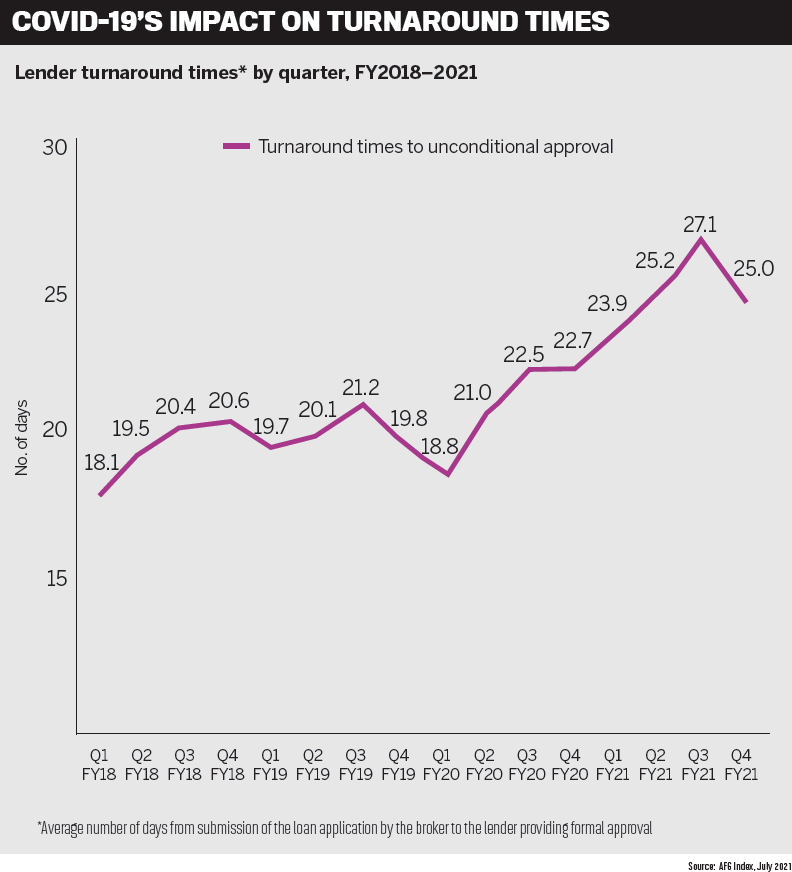

For mortgage brokers, this lack of trust has extended beyond the royal commission. They have accused the major banks of making it harder for their customers to get loans approved due to tightening credit appetites and an increase in paperwork – and they have also been frustrated by long turnaround times, which hit an average high of 27.1 days to unconditional approval in the third quarter of FY21.

The surge in homebuyer activity throughout 2020 did nothing to reduce the strain, and brokers were left questioning whether their borrowers were better off elsewhere. In fact, MPA’s recent Brokers on Non-Banks survey showed a 20% increase in the proportion of brokers who said their customers were open to using non-banks.

The top three reasons for choosing non-banks over banks were the wider view they take of a customer’s circumstances, their faster turnaround times, and banks tightening of their policies.

Asked how they would respond to this, the major banks all said that competition was good for the industry but they were trying to improve their service levels and provide easier loan options for their customers.

Turnaround times were the subject of one of the biggest conversations of the day, with the four banks determined to convey how focused they were on improving times to approval. Much of what they were doing involved improving technology and digital processes, creating simpler forms, and better prioritisation of applications.

For the second year, the Major Banks Roundtable was forced online as both Victoria and NSW battled lockdowns and travel restrictions. This did not stop the group from discussing the biggest topics of the last 12 months, and MPA would like to thank the four bank executives for taking time out of their busy schedules to come together virtually.

Q: Are you seeing more borrowers come to you through mortgage brokers? How is the third party channel a valuable partnership?

If at last year’s Major Banks Roundtable we thought this year would be different, we were wrong. Forced back online due to the lock-downs in Melbourne and Sydney, representatives of four major banks gathered last month to discuss the areas they had been putting a particular focus on in the last 12 months, and how they were supporting brokers.

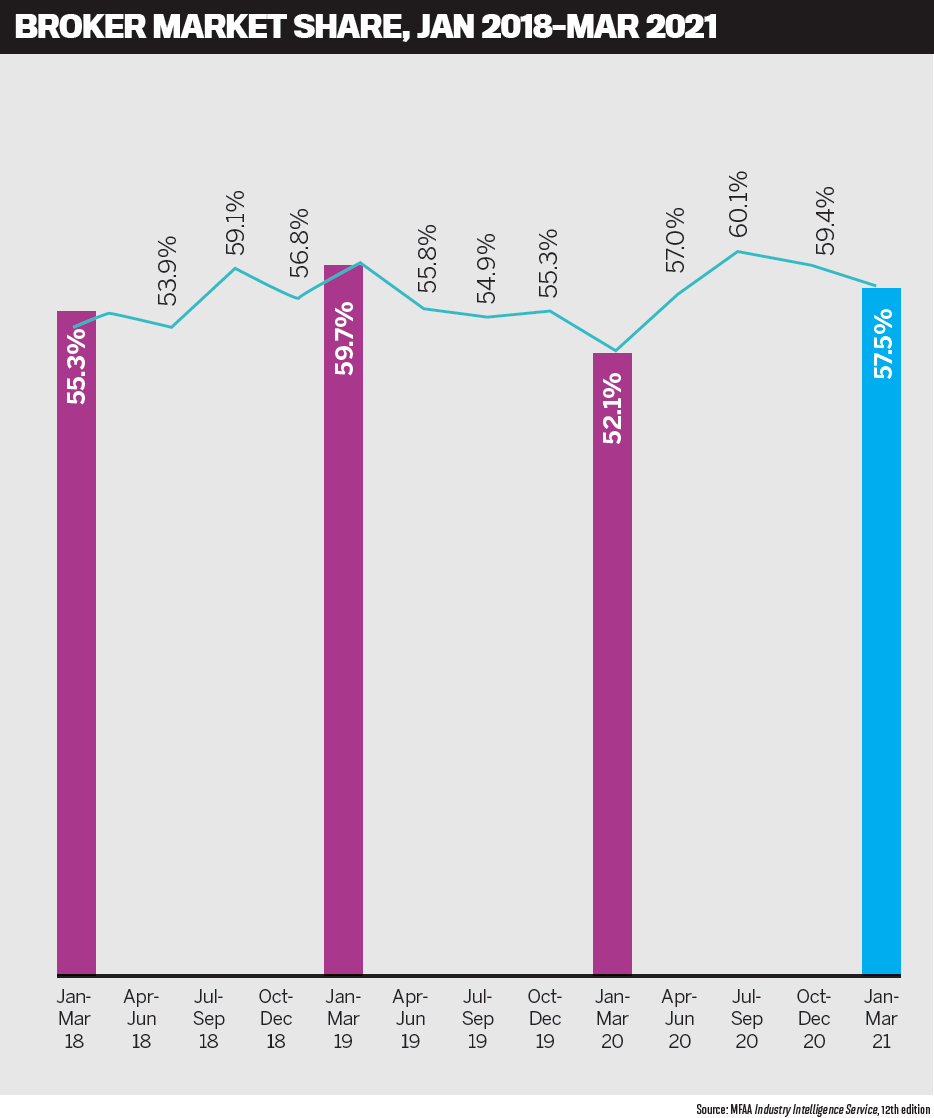

With broker market share surpassing 60% for the first time in 2020, it is clear that growing numbers of consumers are turning to the third party channel.

The record growth in broker applications has been “phenomenal to witness and be a part of ”, said Sarah Willsallen, acting head of broker distribution at Westpac.

Reflecting on her own homeowner-ship journey, she pointed out that she had had a longer relationship with her mortgage broker than with her hairdresser, her GP and her personal trainer.

“I don’t think you can work in broker and not love it or believe in what we do,” she said.

“We respect the customer’s channel of choice, and it’s great to see that more customers are tapping into the powerful resource that comes with a mortgage broker to help them navigate through their home-ownership journey.”

Seeing mortgage brokers as valuable partners to Westpac, the bank conducts regular research to gain feedback from them.

“The feedback we gather from brokers, whether it be through our research and our quarterly NPS surveys or via our many BDMs, is used to build out our strategy for improvements and changes,” Willsallen said.

“Ultimately we want to do whatever we can to help make it easier for brokers to do business with us.”

At Commonwealth Bank, loans coming through the third party channel have remained strong throughout the year, with funding increasing by 30% year-on-year.

Adam Croucher, CBA’s general manager of third party banking, said the broker channel was hugely important to the bank, which was focusing on a new strategy to make the partnership with brokers even stronger by ensuring that it was easier and simpler to do business with.

CEO Matt Comyn also reiterated CBA’s commitment to the channel following its recent full-year results.

“We’ve really been focusing on making sure our broker partners are supported every step of the way through our increasing investment in full-time resources across the value chain, especially through our operations,” Croucher said.

“Simplification is really important to us, processing, and investing in new technology. So, as we emerge from the lock-down our focus is to continue to support and remain extremely relevant in the third party channel for our brokers and our customers.”

ANZ has also been seeing an increasing number of home loans coming through the broker channel.

Head of retail distribution Simone Tilley said the bank recognised that there were aspects of the broker experience it needed to improve on. ANZ participates in groups like the Combined Industry Forum and the MFAA’s lender forums.

“I just want to iterate that every rock is being lifted so that we can propel forward quickly,” Tilley said.

“We want to maintain a strong relationship with brokers, provide a compelling proposition, and continue working better together into the future.

“We acknowledge that we have work to do. From experience, what gets focus often gets results; and I know that everyone has been patient, but we are committed to improving the overall service proposition as fast as we possibly can.”

Government incentives like the First Home Loan Deposit Scheme have also helped bring mortgage brokers to the major banks. NAB’s executive, broker distribution, Phil Waugh, said the bank had secured 62% of the FHLDS places available to major lenders in 2021.

Waugh said NAB had seen “enormous growth” through the broker channel of around 10.5% over the past year. He added that the bank understood the importance of the channel and supporting customers, no matter which channel they came through.

“We’re looking at the customer having a choice as to how they interact with our organisation, and ensuring that we service and support that customer consistently, no matter which channel they come through for a home loan,” Waugh said.

“Certainly, a competitive mortgage broker market is essential to maintain competition in the home loan market and enable access to credit for Australian homebuyers.”

Q: How are you working through issues like turnaround times, which have been a particular pain point for brokers?

Q: How are you working through issues like turnaround times, which have been a particular pain point for brokers?

In the first quarter of FY20, the time taken to receive an unconditional approval was around 18.8 days. Since then, turnaround times have only got longer, reaching a peak of 27.1 days in the third quarter of FY21, according to AFG figures.

The major banks said they understood the difficulties brokers had faced and had been working hard over the past 18 months to resolve the problem.

Willsallen said there had been unprecedented housing demand and growth across the industry, and Westpac had spent the last six months investing in people and changing and reviewing its policies to speed up its processes.

“Our approval times are in line with the industry, and we’re committed to making it simpler and faster to do business with us, including hiring a large number of additional people to help process the home loan applications we’ve been receiving,” she said.

At NAB, times to unconditional approval have remained the “highest priority”, Waugh said. One thing the bank has been working on is simplifying forms, as well as ensuring it has forecasts of application numbers and appropriate resourcing to support these by bringing on extra credit assessors.

Waugh said NAB’s turnaround times now sat at around five days, and as the bank’s SLAs had improved, so had its Net Promoter Score.

“We’re really proud that we’ve made significant improvements on our time to unconditional,” he said.

“When we think about our decisioning and our SLAs, it’s largely around the speed, clarity and consistency and ensuring that we’re as convenient as possible for our brokers. It’s something we will continue to focus on, and we know it’s highly valued by brokers and customers.”

Simplifying processes and introducing automation has been key to the banks’ success in improving their SLAs. As part of ANZ’s effort in this area, it is looking at mandating the submission of certain documents and leveraging machine learning to automate verification of documents.

Acknowledging that response times were not where the bank wanted them to be, Tilley said ANZ intended to be as open and transparent as possible, communicating its assessment times each week to its aggregator partners.

Adding that home loans were the “heart of the bank”, she said: “I think it’s easy to lead and smile when the sun is shining and everything is smooth sailing, but I’m incredibly proud of the ANZ team.

Adding that home loans were the “heart of the bank”, she said: “I think it’s easy to lead and smile when the sun is shining and everything is smooth sailing, but I’m incredibly proud of the ANZ team.

“Everyone has had the courage to be visible, communicate openly, iteratively and transparently each and every time we’ve been engaged.

“I have every confidence that ANZ will respond strongly from this period with a more streamlined data-led approach to the way we automate and simplify processes across all home loan applications.”

CBA has seen a direct correlation between its investment in streamlining processes and its improved service levels after boosting its resources throughout the year, including increasing its number of full-time employees by 25%.

The bank’s investment included introducing new products and services, and even in the last few months it has seen turnaround times improve to one to two days for simple deals and two to four days for complex applications.

“FY21 results showed that 85% of our applications via the broker channel were decisioned within two days, which is a direct result of our focus on operations and the execution of the channel,” Croucher said.

“So we’ll continue to focus and run extremely hard when we need to, to make sure that the sustainability and consistency is there.”

Q: Brokers are saying it is easier than ever to move away from major banks, because the non-banks have greater appetite and more flexibility. What is your response to that?

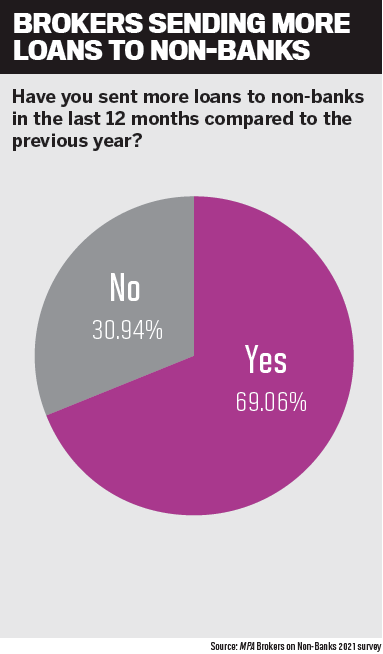

In MPA’s recent Brokers on Non-Banks survey, 70% of brokers said they had written more loans through non-banks in the last 12 months than in the year before.

There is no doubt the lending landscape has become more competitive, said Waugh, but NAB prided itself on being “the bank behind the broker”, so it was continuing to invest in technological support for the broker channel to ensure it could offer competitive turnaround times and consistent service.

He added that the major banks had a responsibility to support the industry, and to be able to keep leaning into it was paramount to NAB’s success.

“I think there’s greater responsibility for us to ensure that we’ve got market-leading processes as well,” Waugh said.

“On top of that, [there’s] our support for the industry – supporting brokers as a broker family, but also supporting the broker industry through the transition to BID.”

The competition created by the non-banks was welcomed by CBA’s Croucher, who said it ensured the major banks continued to be innovative.

He pointed to CBA’s “industry-leading features”, like its Home Loan Compassionate Care, its Property Share loan and its CommBank Green Loan.

CBA has also partnered with energy retailer Amber, which offers customers access to renewable energy at wholesale prices to complement the home loan.

“We relish that competition to make sure that we stay relevant and deliver on what we can for our customers,” Croucher said.

“Customer preferences are constantly changing, so we need to continue to be innovative with our products and services to meet those changing needs.”

In order to maintain its competitive edge against non-banks, Westpac has made a number of policy changes and investments to make things simpler for borrowers.

The major bank has increased options for self-employed applicants, expanded its fast-track eligibility, improved its loan processes for high-value properties, and is offering LMI waivers for a wider range of professionals.

Willsallen said she was especially proud of Westpac’s expansion of its medico policy to include waivers for physiotherapists and chiropractors.

“They’re some of the few medical special-ties that actually have a higher proportion of women participants than men, and it’s a really important part as we look at women in homeownership,” she said.

“I was really pleased to get that through, but we’ve got so much more work to do, and we’re working on how we can help improve our time to decision.

“There’s a really, really long list [of changes], and there’s a lot of one percenters in that list, but they all add up to make it simpler and faster for brokers to work with us.”

Countering the perception that non-banks are more flexible than the major banks, Tilley explained that ANZ was constantly reviewing its policy settings to ensure they were fit for purpose.

“Across the market there’s a prevailing perception that major banks have rigid eligibility criteria for borrowers, with no niches or ability to navigate complexity,” Tilley said.

“At ANZ we have a suite of competitive and flexible policies that allow us to better serve customers across a wide variety of niches, alongside our broader ANZ offering of course.”

Understanding, too, that predictability is a key driver for brokers when placing a loan with a lender, Tilley said the bank was focusing on the consistent application of policy settings.

Another way that banks like ANZ could differentiate themselves was through open banking, she added.

“The portability of data means that customers are likely to expect lenders to provide more personalised services and tailored offerings, and this will provide an opportunity for lenders to further differentiate themselves in the future,” she said.

Q: Are you focusing on any specifi c areas now and over the next 12 months? (for example, tech, products, education)?

Australia is moving away from lock-downs, but the focus on transparency and simplicity continues at the major banks.

Westpac has been working on its customer onboarding journeys with the aim of “bridging the gap” between the bank, brokers and customers. It is also continuing to focus on its time to decision, introducing a new mortgage origination platform that will be key to achieving this over the next 12 months.

The bank is also making improvements in areas such as its e-valuations and desktop valuations, and redesigning its escalations model to identify simpler deals where it can provide faster approval.

Improving communication has been a high priority for Westpac over the last several months, particularly with respect to how the bank communicates mandatory updates to brokers.

“We understand that a broker may receive several emails from lenders every day, and we wanted to simplify our emails to mini-mise the amount of time a broker requires to digest the information,” Willsallen said, explaining that the bank had seen a signifi -cant lift in email opening rates.

“We understand that a broker may receive several emails from lenders every day, and we wanted to simplify our emails to mini-mise the amount of time a broker requires to digest the information,” Willsallen said, explaining that the bank had seen a signifi -cant lift in email opening rates.

“We’ll continue to improve our communications because we recognise [brokers] are engaging with a lot of lenders, and they’re trying to run a business and support their customers. It’s important information, but how do we get it to them in a way that actually really works for them and respects their time and investment?”

Coming out of lockdown – when the importance of its relationships with the broker community has been paramount – much of NAB’s focus will be on continuing to strengthen those relationships.

As a new leader at the bank, Waugh intends to work on building those relationships for himself, and earning brokers’ trust.

NAB has set up a new broker experience team to support the sales teams, which will focus on end-to-end governance of the broker business and fast-tracking digital enhancements, “with the aim of being the most reliable bank for brokers”.

Waugh added that the introduction of NAB’s new mortgage origination process for all origination channels would be an important part of its eff ort to support the broker community going forward.

“I do think that being out there and amongst our broker community over the next 12 months is going to be critical to our success and to delivering on what we say we’re going to deliver, and that’s largely around consistency, clarity, simplification and digital,” he said.

For ANZ, improving processes and technology will continue to be a focus, but the bank also wants to help brokers with their professional development. One way it will continue to do this is through its Doyenne Program, which was established in 2018 to raise the visibility of female brokers and drive more balanced representation in the media.

“I think it’s driven a natural ripple effect of change,” Tilley said. “Since the program has begun, we’ve seen a demonstrable shift in how female brokers are represented across the entire Australian landscape, and it’s a program that hopefully will continue for many years to come.”

ANZ will also continue to evolve its education and training in the broking industry.

“Lenders have a strong role to play in supporting the education and training needs of brokers. These opportunities are critical as the third party industry grows in complexity and sophistication,” Tilley said.

Still on the theme of education, Croucher said CBA had invested in its BDMs and relationship managers with a particular focus on onboarding new customers. He said this would be important over the next six months, particularly in terms of helping brokers through the constant changes in the market.

As part of its investment in technology, CBA has released the second version of its home loan pricing tool, enabling brokers to get real-time and more accurate pricing for individual needs; as well as enhancements to the connection and data flows between its own systems and CRMs.

“Ultimately, [we’ll be] improving the timeliness of data in ‘time to yes’ information to be made available to brokers,” Croucher said.

“This is an ongoing engagement and will be a real focus area for us over the next 12 months – and also enhancements to our ApplyOnline service, in particular improving the document upload and check-in process to really reduce effort and reduce duplication from the brokers.”

Q: With all those technological improvements, do you still see a place for the broker?

The major banks have all talked about their strong focus on technology and how they can make processes easier to use. But they are not the only lenders doing this: second-tier banks, non-banks and fintechs have all been offering digital tools to make things simpler and quicker. Does this mean it will become easier for the customer to go directly to those lenders?

The major banks all dismissed this idea, with Waugh jumping in first to say there was “absolutely” still a place for brokers. He pointed out that NAB was making these improvements with both customer and broker at the forefront of any discussions and decisions.

“We’re absolutely focused on what it means for a broker and how we can support that broker to grow their business,” Waugh said.

“All of our solutions are designed with the broker in mind and to ensure that we make their business and the relationship with their customers better and stronger, and more convenient for them to grow.”

Looking at customer-driven growth of the broker market over the last 20 years, Willsallen said it was clear customers valued the service provided by brokers. They bring relationships and expertise, and she did not see this changing.

“Lending is incredibly technical and complex,” she said.

“We have spent an hour talking about how we’re all trying to listen to feedback and do it faster and make it simpler and do it better; that’s all true, but every customer’s circumstances are still unique.

“A broker is able to use their expertise in mapping out for that customer what their options are, the pros and cons of each alternative, and to help navigate what can be a really tricky and complex environment at a time that’s deeply important to the customer if it’s a home purchase.”

With brokers currently spending as much as 30% more time on processing an application, this comes at a cost. Croucher said CBA was digitising its processes in order to reduce that time and expense for brokers.

He also pointed out that the improvements the major banks were making were designed to simplify processes in order to help brokers, not replace them. For neobanks with a full digital end-to-end process, he said it was about respecting the customers’ channel of choice, regardless of what channel that was.

“We need to make sure that we connect the customer to the channel that they want to deal with,” Croucher said. “And right now over 60% are coming through mortgage brokers, which is fantastic for us, fantastic for the industry.”

Acknowledging that the home loan process is more complex than ever thanks to changes in regulation, Tilley agreed that brokers were spending more time on due diligence and fact-finding.

She said it was lenders’ obligation to simplify, automate and digitise their processes so they were easier to deal with and more predictable.

“As long as the market is demonstrably clear about the digital service proposition and the functionality of the digital service proposition, I think the two can work hand in hand,” Tilley said. She added that digital offerings could work better for refinances, given that these customers were more experienced with the home loan process and may require less support.

“During times of uncertainty, customers particularly value the ‘navigator’ role that brokers play in their home loan journey.”