Rate outlook hinges on Middle East conflict resolution, says economist

A Bank of England interest rate rise in July remains a live possibility even as the prospect of a June hike has faded sharply, according to analysis by ING.

The bank says a prolonged blockade of the Strait of Hormuz could yet force policymakers to act next month, despite energy price movements and weakening wage growth having reduced the immediate pressure to tighten.

Six weeks ago, a June base rate increase appeared probable. At the April 30 meeting, policymakers were judged to be edging toward tightening, though they appeared less inclined than their European Central Bank counterparts, and were operating on a more benign energy price assumption than ING's own base case at a time when the Middle East situation remained uncertain.

"Back then, we thought a June hike had become marginally more likely than not," said James Smith (pictured right), developed markets economist at ING. "That’s no longer the case. Markets are right that the odds of a hike this month have faded."

"Back then, we thought a June hike had become marginally more likely than not," said James Smith (pictured right), developed markets economist at ING. "That’s no longer the case. Markets are right that the odds of a hike this month have faded."

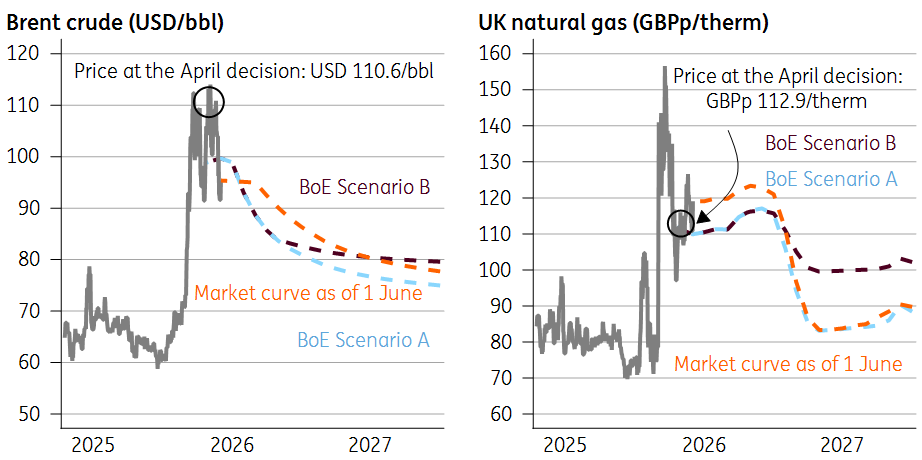

While oil futures for late 2026 and 2027 have drifted upward, this has been offset by a fall of approximately $15 per barrel in spot prices. Natural gas prices have also remained subdued — a significant factor for Britain given its continued reliance on gas and liquefied natural gas.

Current energy prices now sit between the Bank's April "scenario A" and "scenario B". At the time of that meeting, most officials judged that neither scenario automatically required rate rises, on the basis that holding rates steady — as would likely not have occurred absent the Iran conflict — already constitutes a form of tightening.

Energy prices are somewhere between the BoE's "scenario A" and "B"  Source: Macrobond, Bank of England, ING

Source: Macrobond, Bank of England, ING

Futures prices for natural gas delivery in six to 12 months have fallen back close to pre-war levels. If sustained, the 12% rise in household energy bills forecast for July could be followed by an 8% reduction in October. Under this scenario, ING projects inflation peaking at around 3.7% in September before settling near 3.5% into next spring, with lower household energy costs into winter offset partly by rising food price inflation.

"That matters because the Bank has effectively drawn a line in the sand at 4%," Smith said. "Last summer, officials argued that inflation is more likely to persist if headline CPI breaches that level for any sustained period. Right now, it’s not obvious that it will."

The inflation outlook increasingly resembles the second half of last year, when CPI peaked at 3.8%. Despite earlier hawkish concern that price pressures could entrench — and a sharp rise in inflation expectations at that time — those risks did not materialise. April's inflation data, which captures annual price resets at the start of the financial year, came in without significant surprise.

Labour market data has also weakened. Payrolled employment fell sharply, though the figures are expected to be revised upward. Wage growth has slowed markedly: private sector pay rose by only 0.6% annualised over the past three months, compared with approximately 8% in 2023. Pay expectations among chief financial officers responding to the Bank's "decision maker" survey have shown little movement since the conflict began, even as output price forecasts edged slightly higher.

"It all serves as a reminder that the UK economy is much less susceptible to second round effects than it was during the last energy shock four years ago," Smith said. "The economy is more fragile – and we put very little weight on the eye-popping 0.6% growth figure in the first quarter, which we think was amplified by seasonal adjustment issues."

The outlook for rates, Smith added, depends in large part on whether a resolution to the Middle East conflict is reached in the coming weeks and whether energy flows recover. "The longer the crisis drags on, the greater the risk of second-round inflation effects," he said.

ING anticipates that more Monetary Policy Committee members will vote for a hike at the June meeting. "BoE members Megan Greene and potentially Catherine Mann look likely to join Huw Pill in advocating for higher interest rates, even if Governor Andrew Bailey appears much less convinced," Smith said.

"We’ll be taking a fresh look at our global house view on the Middle East and energy prices over the next week or so. But on our existing base case, which factors in a significant recovery in energy flows by July – and based on the current level of spot prices – the more likely scenario is a prolonged pause from the Bank of England."

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.