Older homeowners do not expect to retire without mortgage obligations

Nearly a quarter, or 22%, of UK homeowners with mortgages, amounting to 2.8 million individuals, report that their mortgage repayments are hindering their ability to save for retirement, a joint study by the Equity Release Council (ERC) and Canada Life has revealed.

This figure marks a significant increase from 2021, when 14% shared this sentiment. The data includes over half a million (515,067) homeowners aged above 55 still burdened by mortgage payments.

Among this older demographic, 16% state that their mortgage debt is delaying their full retirement, a rise from 14% in 2021. Additionally, 10% claim that their mortgage obligations prevent them from reducing their working hours, a figure that has more than doubled from 4% in 2021.

The Home Advantage study, based on the financial attitudes and experiences of 5,000 UK adults, underscores the growing challenge of managing mortgage debt. This burden, often characterised by larger sums and longer terms compared to previous generations, is negatively impacting people’s financial wellbeing and plans, further strained by rising interest rates.

Around 21% of all UK homeowners with a mortgage feel that their debt restricts their day-to-day comfort, an increase from 13% in 2021. Additionally, mortgage concerns cause sleepless nights for 13%, prevent 11% from moving homes, and lead 7% to postpone family plans.

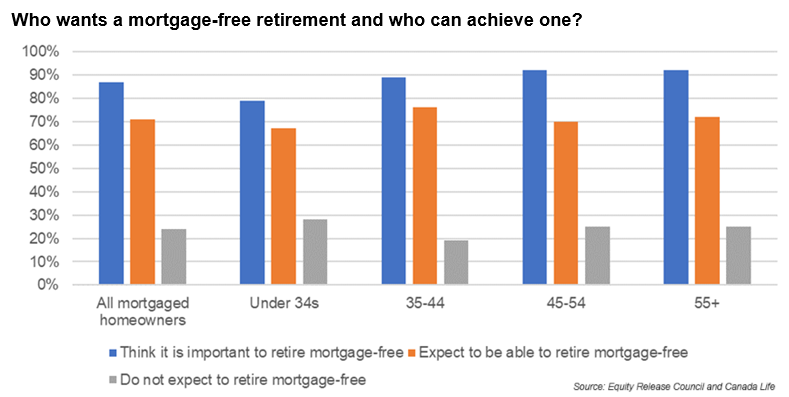

Despite 90% of homeowners deeming it important to retire without a mortgage, only 66% believe they will achieve this goal. This scepticism is even more pronounced among those aged 55 and over, with 60% feeling confident about retiring mortgage-free. Furthermore, 20% of homeowners in this age group, equivalent to 572,297 individuals, do not expect to retire without mortgage obligations, and an additional 19% are uncertain.

The shifting financial landscape has increased interest in later life mortgages and property wealth as tools for managing finances in retirement. Approximately one in three UK consumers now recognise the potential financial benefits of accessing property wealth in later life, a notable increase from 25% in 2021. Additionally, 26% see the value in later life mortgages as a means to enhance their retirement income, up from 21% in 2021.

Over the past five years (2019-2023), more than 201,575 equity release plans have been initiated by individuals over 55 to support their finances in later life, marking a 30% increase from the previous five-year period (2014-2018), which saw 155,082 new plans.

These figures highlight a growing reliance on equity release products, which offer homeowners a way to access the equity in their property, subject to a regulated financial advice process and additional safeguards provided by the ERC.

“With higher interest rates leading many people’s monthly mortgage payments to rise, this harsh reality is making it difficult for homeowners to prioritise retirement savings alongside their mortgage and wider bills,” said Jim Boyd (pictured left), chief executive of the Equity Release Council.

“Rather than struggle against the tide, we need to recognise we are in a new era where the goal of becoming mortgage free will, for some people, be less important than the practical need to access property wealth in later life. With approximately £2.63 trillion of net housing wealth in homes owned by people aged 65 or over, there are clear signs that a shift in the national conscience is underway and property wealth is stepping into the spotlight for retirement planning conversations.”

Tom Evans (pictured right), managing director of retirement at Canada Life, stressed that while the prospect of altering retirement plans might be daunting, there are various options available.

“Lifetime mortgages now offer greater flexibility to individual needs, and so more people may consider the prospect of using property wealth alongside other assets to fund retirement,” Evans said. “Our customer data shows that paying off an existing mortgage has been the top reason for releasing equity for the past six years, but this is just one of many drivers for customers releasing value from their homes.

“For those considering releasing equity, it’s important to do lots of research, discuss it with your family first, and then engage with a professional financial adviser.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.