Assisted buyers buy younger, with bigger deposits and pricier homes

A new report from UK Finance has shed light on the growing role of family support in helping first-time buyers get onto the property ladder, revealing notable differences between those who receive financial assistance and those who don’t.

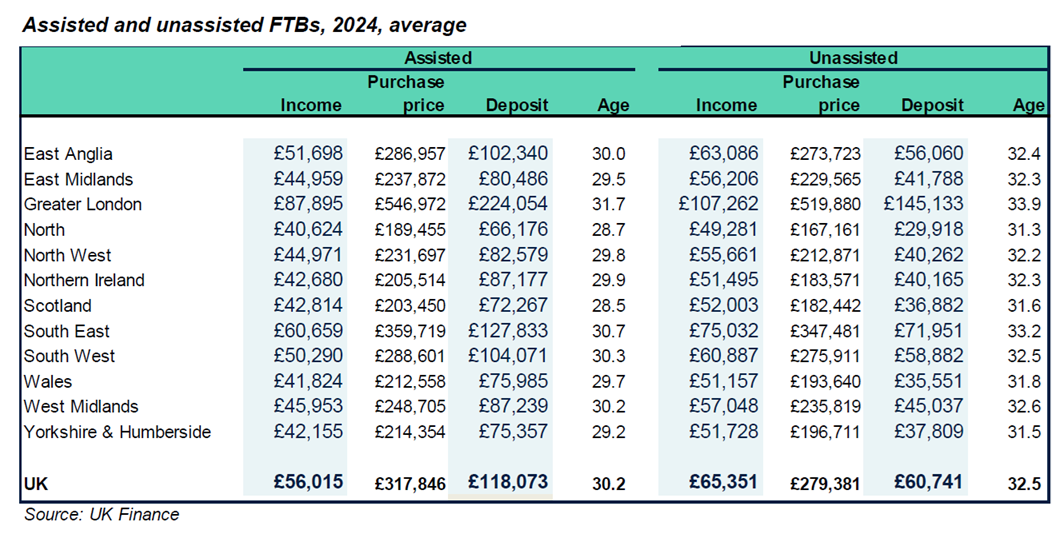

According to the analysis, first-time buyers who rely on help from relatives are generally able to buy earlier and secure more expensive properties than those who fund their purchase independently.

While unsupported buyers tend to have higher household incomes — averaging £65,000 compared to £56,000 for assisted buyers — those with help from family are purchasing homes with higher price tags, made possible by larger deposits.

This trend is reflected across all UK regions, though the capital shows the sharpest contrast. In London, the average deposit for unsupported buyers in 2024 was close to £150,000. For those benefiting from family contributions, the average climbed to nearly £225,000.

The average age of supported buyers is just over 30, compared to over 32 for those without assistance, the UK Finance report also revealed.

“These figures demonstrate that there is still much work to be done to help first-time buyers get onto the property ladder, and that for many people under the age of 30, home ownership is not a realistic aspiration without financial support from parents,” commented Toby Leek, president of NAEA Propertymark.

“With interest rates higher than many people are used to and the average deposit needed to purchase a home now sitting around £50,000, it is imperative that further support is available, and all governments across the UK fulfil their housing targets to help even out demand and supply levels in the long-term.”

“First-time buyers are essential to the UK housing market, helping to unlock transactions further up the chain and maintain overall liquidity,” stressed James Tatch (pictured), head of analytics at UK Finance. “While the majority of first-time buyers are still managing to purchase without help, the growing reliance on family support risks deepening inequality in the housing market.

“A balanced approach which addresses both supply and affordability issues is essential to ensure the door to homeownership remains open to all.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.