But value of outstanding mortgage balances with arrears significantly rises

The total value of all residential mortgage loans in the UK has seen a slight quarterly decrease of 0.1% in the fourth quarter of 2023, settling at £1,657.6 billion, the Bank of England (BoE) has reported.

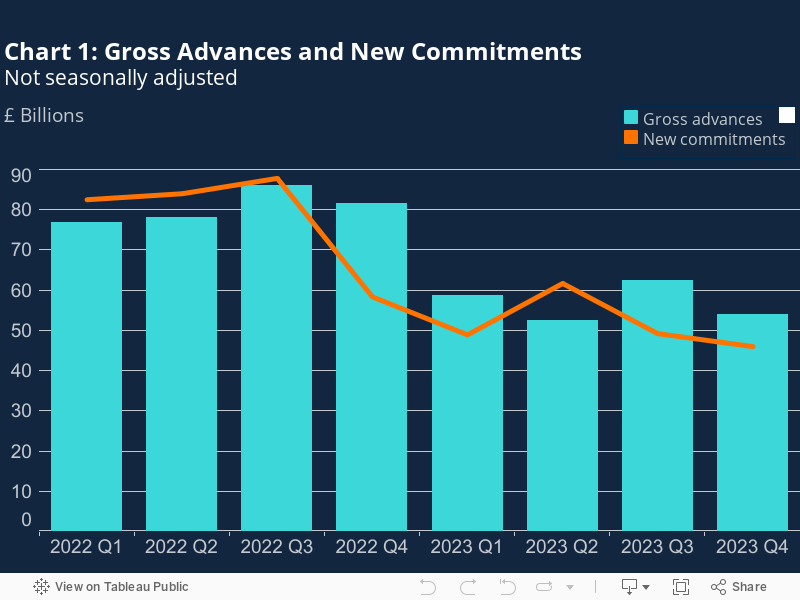

The value of gross mortgage advances fell by 13.4% to £54 billion from the previous quarter, marking a significant 33.8% decrease on a year-on-year basis.

New mortgage commitments, which represent future lending, dropped by 6.6% to £46 billion from the previous quarter. This is 21.2% lower than figures reported last year, marking the lowest level since the first quarter of 2013, excluding the initial impact period of the COVID-19 pandemic.

BoE’s latest Mortgage Lenders and Administrators Return also highlighted changes in lending patterns, noting a decrease in the proportion of lending to borrowers with high loan-to-income (LTI) ratios by 2.6 percentage points to 42.7%, which is 6.6 percentage points lower than the previous year.

In contrast, the share of gross mortgage advances for house purchases for owner-occupation saw a marginal increase of one percentage point to 58.7%, indicating a slight rise in homeowner activity.

Meanwhile, the share of gross advances for remortgages for owner occupation decreased slightly by 0.8 percentage points to 29.7%, albeit still 2.3 percentage points higher than last year.

The share of gross mortgage advances for buy-to-let purposes fell by 0.5 percentage points to 7.0%, the lowest recorded since the third quarter of 2010, and a 4.9 percentage points decline from the previous year.

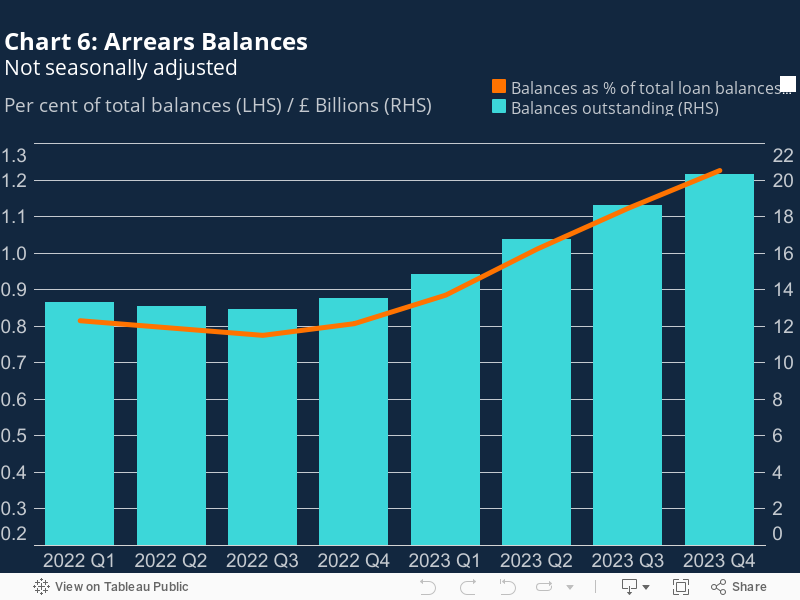

The report also addressed mortgage arrears, revealing a decrease in new arrears cases by 2.6 percentage points from the previous quarter, accounting for 13.2% of the total outstanding balances with arrears.

However, the value of outstanding mortgage balances with arrears rose by 9.2% to £20.3 billion, which is 50.3% higher than the figures reported last year. This increase has led to the highest proportion of total loan balances with arrears relative to all outstanding mortgage balances since the fourth quarter of 2016, now standing at 1.23%.

“New Mortgage Lenders and Administrators statistics for Q4 2023 paint a very worrying picture of the mortgage market,” commented Karen Noye (pictured), mortgage expert at Quilter. “The statistics show that the value of outstanding mortgage balances with arrears is over 50% higher than it was a year ago and has shot up nearly 10% (9.2%) in just one quarter.

“This shows that the large increase in mortgage rates seen over the last couple of years is really starting to bite for some borrowers and this is unfortunately causing them to fall into arrears as they simply can’t afford to keep up with their increased payments.

“Positively, the statistics show that new arrears cases decreased by 2.6% from the previous quarter, to 13.2% of the total outstanding balances with arrears, but remained 0.2% higher than a year earlier. This may well continue to climb again though as more people come off fixed term mortgages set when rates were low.”

According to Noye, recent government actions aimed at reducing the appeal of the buy-to-let market are showing results, as indicated by the decrease in the proportion of gross mortgage advances for buy-to-let purposes.

“The changes to the holiday let rules at the Budget may also make things even worse for landlords who have been hit with numerous changes to the buy to let tax landscape in recent years making it a less attractive option,” she said. “This has resulted in many leaving the market.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.