Jump to winners | Jump to methodology | View PDF

Mortgage Introducer’s 5-Star Lenders of 2023 are delivering crucial service and support for their broker partners despite persistent market volatility. This year’s best mortgage lenders have earned the trust and confidence of the broking community, whose ratings across various metrics most vital to them catapulted the top performers onto the 5-Star podium.

In a highly competitive mortgage landscape, the 5-Star Lenders are thriving while driving broker satisfaction by prioritising:

fair pricing for clients

streamlined processes

reasonable turnaround times

comprehensive and responsive underwriting

exceptional customer service

“Ultimately, we are looking for good outcomes for our clients in the quickest and simplest way possible,” says one of MI’s Top Brokers of 2022, Rebecca Shuttle, principal at MIMA Mortgage and Protection Advice. “Lenders who can provide all-around good service and products with clear and concise lending policies mean we are better positioned with the tools we need to support our clients.”

The Society of Mortgage Professionals’ vice chair and CEO of Connect for Intermediaries, Liz Syms, adds that brokers will typically start with the following when assessing a lender:

matching their client’s criteria and needs

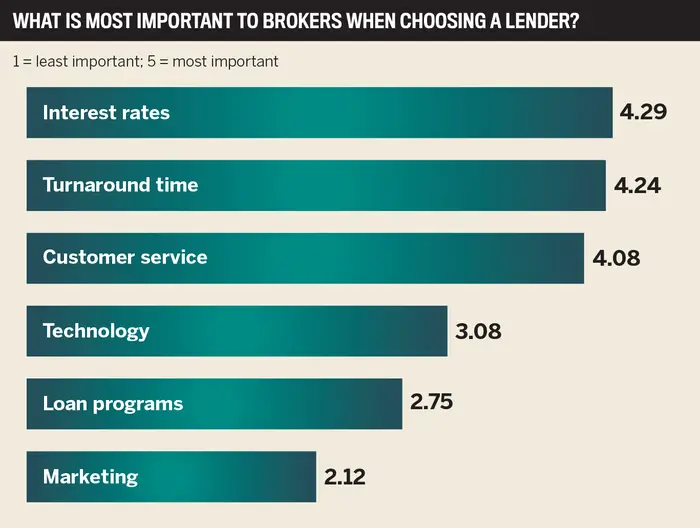

comparing interest rates

speed of service and consistency

“It is essential that 5-Star Lenders offer the whole package,” she says.

Regarding speed and willingness to lend, brokers noted that West One has excelled on both counts, prompting them to give more business to the 5-Star Lender in the past 12 months.

But it isn’t just agility and appetite that keep West One at the leading edge, as the mnemonic CREDIT underpinning its culture demonstrates:

customer-first approach

results-oriented

energy

development

invention

teamwork

“We’re not a bank or a scorecard-driven lender; we’re all about listening to what the borrowers want our money for, and we have an inventive approach to solving problems,” says COO Stephen Hogg.

“We keep lending, and we’ve been running the business through the pandemic, Brexit and all sorts of dislocations in the market,” he continues. “Relative to our peers in the non-bank lending space, we’re large, profitable and stable. It isn’t clever or sexy; it’s repeatable, reliable and trustworthy. If we say we’ll lend money on a certain day and time, we’ll do that.”

The specialist lender in the property mortgage space has grown exponentially over the last decade, attracting several institutional shareholders. The company now boasts its most prominent sponsor, Elliott Advisors, one of the world’s largest money managers.

While West One isn’t a small shop any longer, it has continued to strengthen its competitive edge by maintaining a small-business mentality and prioritising its nimbleness, speed and efficiency.

That can best be seen in its approach to the following, emphasised by Hogg:

Customer service: “We look at it two ways: there are the basics like answering the phone and responding to emails promptly. But this is entirely a relationship business; people buy people. And we are adamant that our people serve our broker community well.”

Tailor-made solutions: “We’re here to fill a role in the industry, listening to people, working out what they need and finding inventive and creative solutions to fit that.”

Pricing: “We try to price fairly; we don’t lend money at a loss, and we’ve made very few losses historically. We price for risk, a fair return and the service and speed we can deliver. We’re not trying to be a massive corporate bank smashing out thousands of homogenous widgets.”

Valuing and nurturing its broker partnerships keeps West One at the forefront of its niche lending space. Building those long-standing relationships is a thread that runs through all of its business strategies, from marketing and campaigns to client service and everything in between.

“We’ve been working with brokers consistently for many years, and they keep coming back,” says Hogg. “We’ve also pushed to bring in new communities of brokers as we broadened our product range and got into new areas.”

The best mortgage lender in the UK plans to continue building out its product range, possibly including semi-commercial and commercial mortgages. At the same time, the recipe that fueled its success will inform its forward-looking ambitions.

Its commitment to fostering a positive work environment and investing in the development of its people stands it in good stead to continue setting new standards of industry excellence.

“We will keep going and be a reliable lender the whole way through,” Hogg says. “We’ll continue to be a one-stop-shop for people’s difficult, interesting, slightly quirky, off-the-high street financing needs.”

Pricing volatility has been an ongoing challenge for the industry, and the best mortgage lenders have acted quickly to reprice and communicate proactively with their broker partners. They have also leveraged technology to streamline the lending process and improve turnaround times, with the following improvements mentioned by broker respondents:

AI-powered verification

open banking

digitising document submissions

desktop valuation systems

In commenting on brokers’ top reason for choosing lenders – interest rates – the Society of Mortgage Professionals’ Syms says, “Brokers want to be able to secure the most competitive options for their customers without compromising on service.”

Former Top Broker Shuttle agrees. She says, “Lenders should offer fair pricing that reflects market conditions, is cost-effective for the client and is inclusive of arrangement fees.”

Several broker respondents didn’t pull any punches on the issue:

“It’s all led by interest rates and what’s most cost-effective for the client. Then we look at criteria, so it depends on who is offering what.”

“I’m fiercely independent, and each case is individually placed.”

“We only support lenders that meet our clients’ requirements based on criteria and interest rates.”

“A lender deemed 5-Star adds a competitive element, but they need to back this up through consistency and, ultimately, in this market, competitive pricing, which has the client’s best interests at the centre,” Shuttle says.

The intermediary-only specialist lender and mortgage servicer has built its reputation on a passionate commitment to great broker experience, which drives its culture. The 5-Star Lender’s agility and ability to adapt quickly have enabled it to excel in its niche of manually underwritten residential and buy-to-let mortgage criteria for borrowers with more complex needs.

Two years ago, the organisation identified the main drivers of the Net Promoter Scores that brokers gave them after doing business, identifying the areas noted as most important and where the lender believed there was room for improvement:

speeding up the processing of mortgage offers

increasing the desire for more direct underwriter contact after case submission

“Taking a risk-based approach, we overhauled our process, removing the automatic need for bank statements, for example, and creating the TCM team, who are there specifically to liaise with the broker to get the documents required to get the case to offer,” says Kelly Pallister, managing director of operations.

The simplification of its underwriting process and significant investments in some new systems kept Foundation Home Loans’ turnaround times extremely sharp through 2023, freeing up staff from manual tasks to spend more time talking to brokers and offering more automated case updates to eliminate call wait times.

“The other important thing to remember about specialist lenders is that it’s the breadth of criteria on offer, which is the most relevant offering, combined with the ability to manually underwrite against a real understanding of the borrowers’ situation,” says George Gee, managing director of commercial.

Foundation Home Loans’ experienced staff is also at the cutting edge due to initiatives such as:

broadening its lending criteria, especially in the owner-occupier segment, to meet the ever-evolving needs of borrowers who don’t meet mainstream criteria

combining the widened lending criteria with its culture of personal engagement with mortgage brokers to expand the range of mortgage customers whom intermediaries can assist in their business

To uncover the best lenders in the eyes of the UK’s broker community, Mortgage Introducer reached out to brokers across the country, asking them to rate the lenders they work with across three key areas: tracker mortgages, fixed-rate mortgages and standard variable rates.

Mortgage Introducer also asked brokers to weigh in on important aspects of the broker-lender relationship, such as interest rates, turnaround times, customer service, technology, loan programs and marketing. Lenders that earned an average score of 4 or higher were recognised in the second annual 5-Star Lenders.

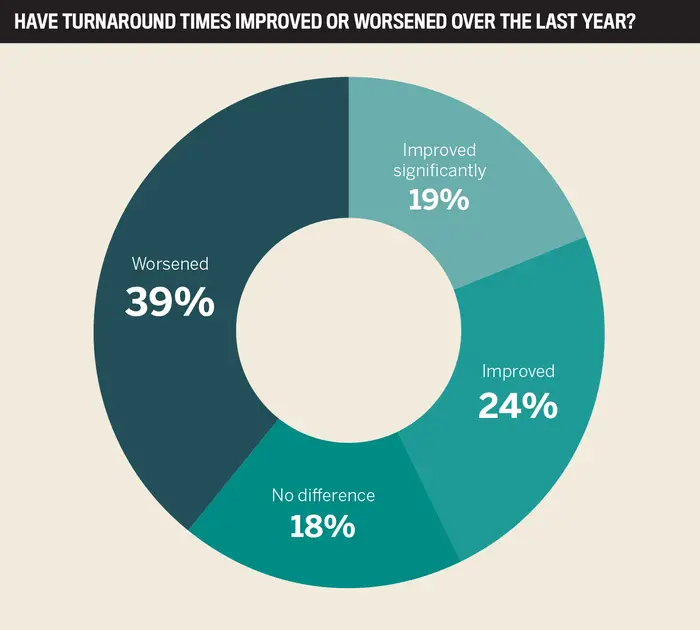

42% of brokers said turnaround times had improved significantly

26% of brokers said lenders could improve service levels through better communication

19% of brokers said lenders could improve service levels by having more BDMs or credit assessors, a simpler income verification process and better technology (a three-way tie)