Find out much about home mortgage rates in Canada. Read this article now

For most Canadians, buying a home is one of the most important decisions and biggest investments they will make in their lifetime. That’s why you need to do your research on mortgage rates and shop around.

Depending on your decision, you could spend—or save—thousands of dollars during the life of your home loan.

To help you on your journey to homeownership, here is everything you need to know about mortgage rates in Canada, from what affects rates to how to find the best one for you.

How do I get the best mortgage rate in Canada?

Since buying a home and taking on a mortgage are such major commitments, it is important that you get the best mortgage rate possible. When shopping for the best deal, you will want to consider not only the amount borrowed but the interest rate as well. Doing so may save you tens of thousands of dollars over the life of your loan.

Here are 10 tips to getting the best mortgage rate in Canada:

- Research interest rates

- Lower your DTI ratio

- Improve your credit score

- Stabilize your income

- Employment history

- Increase your down payment

- Use cash reserves

- Interest rate fluctuations

- Low-ratio vs. high-ratio mortgages

- Shop, shop, shop

To give you a better idea what to look for, here is a closer look at each:

1. Research interest rates

When shopping for the best mortgage, there is no one-size-fits-all approach. The best mortgage for you is the mortgage that best suits your financial situation. Not only are there different mortgages to choose from, but each one will affect your interest rate. Use the tool below and you will see that there are many different options for how you can approach your mortgage:

If you are a borrower that lenders consider less risky, you will likely qualify for a prime mortgage—one of the better mortgage options. To qualify for a prime mortgage, you will need a credit score of 670 or higher, pay between 10% and 20% for a down payment, and have a lower debt-to-income (DTI) ratio. One reason prime mortgages are so sought after is the lower interest rate, which could potentially save you thousands of dollars over the life of the loan.

Subprime mortgages, on the other hand, are for borrowers who have a low credit score, usually between 580 and 669. Subprime mortgages are for borrowers who lenders consider riskier and carry higher interest rates.

2. Lower your debt-to-income ratio

In Canada, lowering your debt-to-income (DTI) ratio is an easy way to get the best mortgage rate. Your DTI is the percentage of your gross monthly income that goes toward paying off your debts. A lender will look at your DTI to determine the level of risk you carry when borrowing money.

Most industry experts also recommend that you keep your:

- Gross Debt Service (GDS) ratio below 39%

- Total Debt Service (TDS) ratio below 44%

To lower your DTI, you can increase your income, reduce debt by buying only what you can afford in cash, or make bigger payments on your debts. Doing any or all of these things will show lenders that you are less of a risk.

3. Improve credit score

Improving your credit score is a possibility, even though it may take you some time. One easy way to accomplish this is to make more substantial payments on your credit cards. A few other ways are to pay your bills, keep outstanding balances on any credit cards low, or pay off any collections on your credit report.

4. Stabilize your income

The way lenders view it, you will be less likely to default on your mortgage if you have income stability. To accomplish this, you need to look at how much money you earn each month compared to how much you spend. After this review, you can then determine how you can earn more money and spend even less, which is typically done by limiting frivolous expenses, taking on a side hustle, or requesting more work hours.

5. Compile your employment history

Compiling your employment history prior to meeting with a mortgage lender is crucial. Doing so will signal to lenders that you are serious about repaying the loan and are low risk for defaulting on your mortgage payments. Your employment history will indicate that you have been consistently employed and will likely be employed for the foreseeable future.

6. Increase your down payment

You can reduce the size of your mortgage and potentially get a better interest rate if you pay more on your down payment. Whether or not this will make financial sense for you requires a sound knowledge of your own financial situation as well as your down payment options. A good starting point, however, is that making a down payment of at least 20% will likely secure you a better interest rate than if you put down 5%, for instance.

7. Use cash reserves

A lender will review your savings account to determine if you have enough money in reserve to pay for your mortgage if you lose your job. Ideally, you will have a few months’ worth of mortgage payments in the bank, which will also indicate to lenders that you are fiscally responsible and therefore are a good candidate for a mortgage loan. To get a better mortgage rate, you should consider saving up to three or four months’ worth of home loan payments.

8. Account for interest rate fluctuations

You may want to time the buying of your home when interest rates are exceptionally low. That will lower your monthly payments and the interest you pay throughout the life of your loan.

9. Low-ratio mortgages vs. high-ratio mortgages

Paying below 20% as a down payment on a property will require you to get mortgage loan insurance, which is an added layer of protection for lenders in case you default on the loan. Mortgage loan insurance can be added to your home loan payments each month or can be paid as an up-front fee. If you want to avoid it, you can save up to make a down payment of at least 20%. Typically, however, your lender will drop mortgage loan insurance after you have built up 22% equity in your home.

10. Shop, shop, shop

After finishing each of these steps to getting the best mortgage rate, you will want to shop around. Since some lenders can offer you better rates than others, it is imperative that you are aware of every available option prior to committing. Remember—this is likely to be the most significant investment that you will make in your life.

Also consider working with a mortgage broker, which will act as a third-party intermediary between you, the borrower, and your lender. In fact, brokers usually collect your financial information and do most of the shopping for you, to secure the best rates and terms. To aid them in this, most brokers have their own pool of lenders to choose from. These services do not cost you anything.

You can find a great broker by reviewing our annual Special Reports on the mortgage industry, where we poll industry experts and apply our own specialist knowledge.

What is a mortgage rate hold?

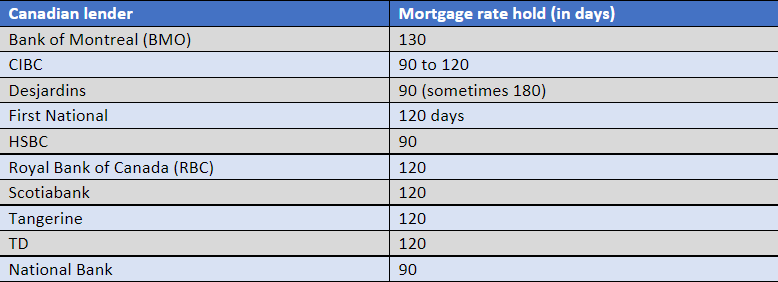

A mortgage rate hold is the amount of time that a lender will hold your quoted rate. Put another way, a mortgage rate hold is a sort of guarantee of the agreed-upon rate, in the event you qualify for it. Typically, mortgage rate holds last anywhere from 30 to 120 days.

In Canada, a couple exceptions are Desjardins, which sometimes offers rate holds of up to 180 days, and Bank of Montreal (BMO), which offers rate holds of 130 days. Here is a breakdown of how Canada’s largest lenders compare:

Because the average Canadian closes their mortgage within 45 days, most borrowers do not require the maximum mortgage rate hold offered by most lenders. These maximum mortgage holds may offer a peace of mind, but if you do not need it, you should not pay for it.

A couple of scenarios where it might make sense to utilize a mortgage rate hold are as follows:

- If you have a far-off closing date

- If you are pre-approved but have yet to find a home to purchase

It is important to remember that you are not necessarily guaranteed to be approved for the mortgage even if the lender guarantees a rate for the hold period. First, lenders will verify your credit history and any other financial details to make sure you qualify for the home loan. If you fail to meet the minimum requirements, lenders may still refuse your application despite the rate hold.

What affects mortgage rates in Canada?

There are multiple factors that affect mortgage rates, or interest rates, in Canada. Some of these factors include your own financial situation, while others are determined by external factors. We looked at credit score above; here are five other factors that affect mortgage interest rates in Canada:

- Location of home

- Loan amount and home price

- Down payment

- Loan term

- Interest rate type

Let’s take a closer look at each to better understand the different factors and how they may impact your bottom line:

1. Location of home

Location can impact your mortgage interest rate. Not only does the province or territory play a role, but so does living in a rural area or a city. For this reason, you will want to shop around between lenders, including local lenders, since each will offer different rates and loan products. Speaking with lenders will help you grasp the various options available to you, regardless of where you want to live.

2. Loan amount and home price

Your loan amount will follow this basic formula:

Home price + closing cost – down payment = loan amount

Your mortgage insurance and closing costs might be included in your home loan depending on your financial circumstances or mortgage loan type. You may also know the price range of the property you want to purchase, if you have already started shopping. If, however, you have just started, real estate websites can be a good source to get you started, providing you with an idea of what typical prices are in each area.

3. Down payment

The larger down payment you make, the lower your interest rate is likely to be. The reason is lenders view you as less risky when you have more stake in the home. If it makes financial sense to make a 20% down payment, you will get a lower interest rate and avoid having to pay for private mortgage insurance.

A lower interest rate will likely save you money in the long run. However, it is important to look at your total cost to borrow instead of just the interest rate because you may end up paying as much or more in monthly mortgage insurance payments, depending on how much under 20% you go on your down payment.

4. Loan term

Your loan term is the amount of time you have to pay the loan back. Generally, a short loan term equals lower overall costs and lower interest rates—but higher monthly payments. Like your down payment, your loan term is a balancing act to determine how much you stand to save (or spend). It is important to speak with a professional to figure out the right balance between your monthly payments, your interest rate, and your loan term.

So as of half an hour ago...

— Little Saint Nic 🎄 (@RoseAndMe95) October 1, 2020

MY MORTGAGE WAS APPROVED 🎉🎉🎉 pic.twitter.com/oA8GdOwWte

5. Interest rate type

When we say interest rate type, we’re essentially saying a fixed-rate or an adjustable-rate mortgage. Fixed rates stay the same over time; adjustable rates have an initial fixed period and then fluctuate depending on the market conditions. When choosing between the two, it is important to know that your initial rate may be more favourable with an adjustable-rate mortgage than a fixed-rate mortgage, but then rise significantly in the future.

What is a high ratio mortgage?

A high-ratio mortgage is when you make a down payment that is under 20% of the purchase price, meaning that it has a loan-to-value (LTV) ratio of over 80%. Your LTV is a risk assessment lenders make when looking at your mortgage application. Lenders calculate your LTV by dividing the amount you are borrowing by the purchase price, then express it as a percentage.

A low-ratio mortgage (or conventional mortgage), on the other hand, is when you make a down payment that is 20% or more of the purchase price, meaning that it has an LTV ratio of 80% or less.

As we have seen, there are many factors that affect mortgage rates in Canada, from your credit score to your down payment to your loan term. While striking the right balance depends on what makes financial sense to you, it is achievable. Seeking expertise can help—as can knowing how to shop in the first place. Knowing what is required of you beforehand is a great way to get the best mortgage rate for you.

Read more: Is it better to get a high ratio mortgage?

Those of us here at Canadian Mortgage Professional know that mortgage rates in Canada are tough right now. Is there anything you would like to share in the comments section below? We would love to hear from you.