"LendHub was born out of a need for speed"

This article was produced in partnership with LendHub.

Desmond Devoy, of Canadian Mortgage Professional, sat down with Shay Shnet, CEO and founder, LendHub, to discuss their new, soon-to-be-launched app and how technology is speeding up the mortgage application process.

LendHub has launched a new app that could speed up the mortgage application process by getting money into the hands of clients quicker.

After two years in development, the app has already been launched with one broker in the beta testing phase but will be ready for a larger roll-out this January.

The app will “allow brokers to process their deals even faster and receive auto approvals instantly,” said Shay Shnet, the company’s founder and CEO. “We’re very excited about this added feature.”

Ease of use and speed have always been part of the LendHub’s operating mantra.

“LendHub was born out of a need for speed,” he said. “It’s based on the idea that a $30,000 or $40,000 mortgage shouldn’t have the same process as a $500,000 or $1 million mortgage.”

Instead, the company focuses on micro mortgages of up to $100,000, but also as low as $10,000, with funding typically happening between 48 to 72 hours after approval. (There are exceptions to the loan size – just that day, Shnet had signed off on a loan for $112,000.)

Technology leap

The company uses banking software that is used by large institutions like banks to validate critical pieces of borrower information.

“As you can imagine, no technology is perfect and requires our people to interpret, piece together the entire picture,” he said. “Sometimes this is where the human touch is also critical.”

While some clients might still be intimidated by technology, Shnet said the company is ready to lend a helping hand.

“Technology is not everybody’s friend,” he said. “We’re here to assist. Anybody calls, we pick up the phone and we’re always here to help.”

He said that brokers benefit from this technology, especially through savings of both time and money.

“We are able to underwrite and fund very quickly and efficiently, making it a pleasant experience for both the broker and their clients as they avoid jumping through the additional hoops needed on a private mortgage transaction,” he said.

The whole process is done in-house, meaning that outside lawyers do not have to be involved.

“We control the process in-house from beginning to end,” he said. “Typically, there is no lag time for appraisals, nor are we waiting, begging for lawyers to move us to the front of their line or to instruct the process and process the deal… Any broker who has worked with a traditional [lender] can share frustrations about time-consuming deals that get delayed and get lost in the shuffle.”

LendHub has its own underwriting and compliance departments, allowing them to “communicate directly with the client and with the broker.”

Most residential properties do not need an appraisal from his company, but some may require one on a case-by-case basis.

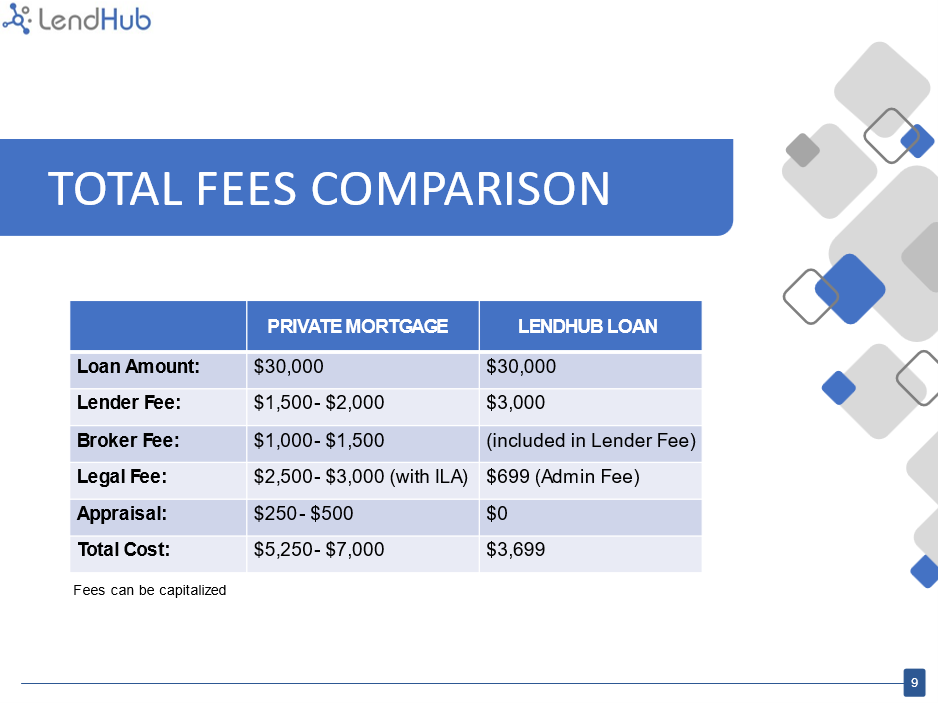

|

PRIVATE MORTGAGE |

LENDHUB LOAN |

|

|---|---|---|

|

Loan Amount: |

$30,000 |

$30,000 |

|

Lender Fee: |

$1,500 - $2,000 |

$3,000 |

|

Broker Fee: |

$1,000 - $1,500 |

(included in Lender Fee) |

|

Legal Fee: |

$2,500 - $3,000 (with ILA) |

$699 (Admin Fee) |

|

Appraisal: |

$250 - $500 |

$0 |

|

Total Cost: |

$5,250 - $7,000 |

$3,699 |

Lending realities

There are two things that Shnet would like people to know about his company and his line of work.

Firstly, it is not to be confused with a UK firm of the same name, if you Google the company as this writer did.

“We had the same issue with LinkedIn!” he said with a laugh. “We adjusted our LinkedIn to just clarify that we are not them.”

Shnet’s firm is headquartered in Toronto.

The other part of the perception problem is how private lenders like him are seen.

“Private lenders are not liked because the rates are higher,” he said. “There’s a lot of different fees and people aren’t happy to be in a position to even need private funds.”

But they do serve as an important piece of the puzzle, which lenders may only recognize later in the process.

“We’ve received really positive feedback from borrowers who are very grateful for a quick and easy process.”

LendHub