Jump to winners | Jump to methodology | View PDF

Ask any mortgage broker about the most critical aspects of ensuring their day-to-day work functions smoothly, and chances are that lenders will feature near the top of the list. As mortgage professionals strive to unearth the best possible deals for their clients, the value of having a lender that’s responsive, flexible, efficient and prompt can’t be overstated.

It’s been especially significant over the past 18 months, when an already heated housing market dialled up several notches and created an environment in which speed of response, turnaround time and swift issue resolution have proven paramount for brokers and their clients.

Each year, CMP puts lender performance in the spotlight, surveying brokers across Canada to find out how their lending partners stacked up in a variety of categories. This year’s survey proved especially informative, highlighting the lenders that were able to maintain smooth, effective service in the face of a relentless mortgage market.

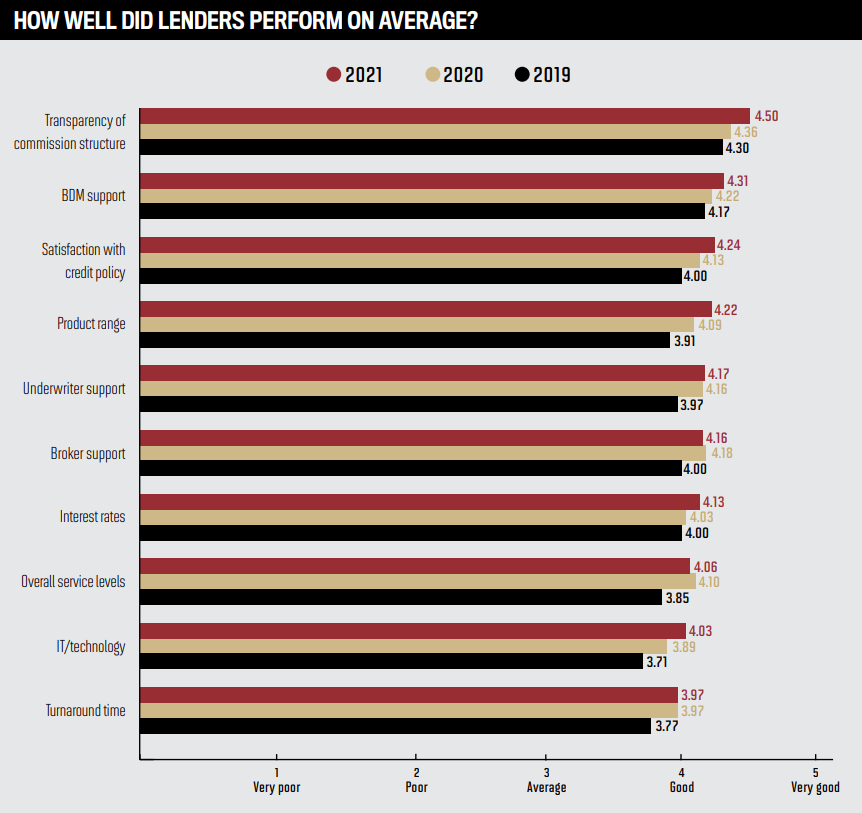

Overall, lenders increased their average score in nearly every category compared to 2020, registering particularly large increases in product range, interest rates, BDM support and transparency of commission structure. For the two categories where lenders’ average score dropped from 2020 – broker support and overall service levels – the decline was comparatively minimal.

In total, 13 lenders were awarded medals in at least one category this year – and for these top-performing lenders, the survey results are an affirmation of the organization, dedication and commitment they demonstrated to maintain exemplary service levels and broker support during a challenging and intense time for the mortgage industry.

Meeting service expectations

Given the frenzied market that’s developed over the past 18 months, it’s little surprise that the ability to fund a deal swiftly and smoothly has remained one of the top priorities for brokers when dealing with lenders. Overall, lenders managed to keep pace with their 2020 performance on turnaround time, netting an overall average score of 3.97 for the second year in a row. However, turnaround time ranked as the lowest-scoring category for lenders on this year’s survey.

Ron Swift, CEO of Radius Financial, which earned a gold medal from brokers for turnaround time, says responding quickly during periods of high demand requires a combination of strong internal processes and clear communication with mortgage brokers to make sure each party is on the same page.

“Hire the best people you can afford, or train your people so they can better manage the heavy volume workloads,” Swift advises. “Make sure your processes are as streamlined as possible; fewer steps make for fewer bottlenecks. Educate your brokers on what and when you need to eliminate last-minute rushes. Communicate – the reality is no lender can provide exceptional service 100% of the time. There are periods when there’s more volume than the lender can efficiently manage – not a bad thing. You just need to set the right expectation with your clients.”

Bruno Valko, vice-president of sales at RMG Mortgages, which earned bronze in the turnaround time category, likewise points to communication and consistency as important factors in maintaining positive broker relationships. He advises lenders to meet brokers’ expectations by “[working] on the reallocation of resources, adjusting the distribution of workloads, moving applications amongst underwriters, and enhancements to technology to help ensure rapid and efficient turnaround times.”

On the communication side, Valko says providing consistent deal and document decisions and setting clear expectations are some of the main things lenders can do to ensure there are no mixed messages.

For lenders to provide unparalleled service to their broker partners, it’s also important that they have a dedicated team of business development managers that brokers can call upon at any moment to provide clarity and support. Overall, lenders made great strides in BDM support this year, earning an average score of 4.31 – a significant improvement on 2020’s 4.22.

“It’s imperative that the BDMs understand their customers – who they are, how they like to work and what their needs are,” Swift says. “Once they understand their customers’ needs, they can then implement a plan that will deliver the service levels required to meet or exceed their customers’ expectations.”

Valko adds that strong communication between underwriters and brokers at all stages is also an integral aspect of a successful deal. Providing admin support to underwriters so they can focus on processing deals and applications can help lenders deliver that service, he says, as can “[shifting] resources from other areas to help ensure strong underwriter support.”

A longstanding expectation brokers have of their lenders is a transparent and fair commission structure – and this is an area where lenders are clearly excelling. Not only was transparency of commission structure the highest-scoring category in this year’s Brokers on Lenders survey, but lenders managed to considerably raise their overall average score, from 4.36 in 2020 to 4.50 in 2021.

Swift says it’s important for all lenders to make sure their commission structures are reasonable, clear and easily understood by the broker.

“If it’s important to your organization, and you’re going to compensate brokers for meeting or exceeding results, then it should be transparent for everyone to see,” he says. “Bottom line, whatever results you’re trying to incentivize need to be transparent, or it won’t be as effective as it should be.”

What other concerns do brokers have?

In addition to asking them to rate their lenders, CMP also pressed brokers for their thoughts on evolving commission structures, why they would submit a deal to a bank versus a monoline lender, and the challenges and successes they’ve had with lenders over the past 12 months.

While the volume of funded mortgages has risen dramatically over the past year and a half, a majority of survey respondents said they expect lender commissions and bonuses to remain largely static over the next year or two. More than 60% of brokers said they thought commissions would stay the same, while around 23% anticipated an increase and 15% thought a decrease was in the cards.

When asked why they might submit certain deals to banks rather than monoline lenders, a majority of brokers (58%) said the banks’ product offerings were the biggest consideration. Another 28% said it came down to client preference, while 18% said they were swayed by the service they received from the bank’s underwriter and/or BDM.

As for their biggest challenges with lenders over the past year, many brokers unsurprisingly brought up turnaround times. “Some lenders just don’t have adequate staff,” one broker noted, while another acknowledged that “it’s just the sheer volume, so it has created some backlogs at times.”

Communication was also a frequent sore point; many brokers said communication often takes a back seat when volume gets heavy. “Actually talking to someone on the phone can be tough,” one broker said. “Most people want to communicate via email or portals. It’s not the same as talking through a file for three to five minutes versus three to five days of emails where you can’t tell someone’s tone.” Another broker was empathetic but straightforward with their feedback: “We are all struggling with workloads, and we understand. Ignoring or just not communicating is the worst possible thing to do. Even if it is bad news, we need communication.”

Finally, many brokers were frustrated with the documentation step of the process. Several mentioned slow turnarounds on document review, while others were vexed by seemingly endless requests for documentation. “When they finally respond, there are more requirements on the checklist – even though some of the documents were previously provided, they are not acceptable,” one broker said.

It wasn’t all bad news, though – brokers had plenty of compliments for lenders as well. When asked about the best thing a lender had done for them over the past 12 months, many brokers mentioned a willingness to expedite deals and make exceptions on certain files. Above all, brokers seem to be most pleased with lenders who are willing to engage with them as a true partner. As one broker put it: “Having a great relationship with a lender is the best thing – that relationship means they pick up the phone, you send the deal and get it approved and funded.”

To uncover the best lenders in the eyes of Canada’s broker community, CMP reached out to brokers across the country, asking them to rate the lenders they work with across 10 key areas, including turnaround time, interest rates, product range, broker support, overall service levels and more. As in previous years, CMP also asked brokers to weigh in on important aspects of the broker-lender relationship, such as how commissions and bonuses might change and why they choose to send deals to the banks rather than monoline lenders.

For each category, lenders were ranked in order of merit according to an average score calculated from the ratings they received from brokers. The top three A lenders and alternative lenders in each category received a gold, silver or bronze medal. Lenders’ combined average score from all categories determined the overall gold, silver and bronze medallists.