To gauge the pulse of SME lending, MPA talks to four leading non-bank lenders. They paint a picture of steadfast resilience and shine a spotlight on brokers who bring real expertise to the table

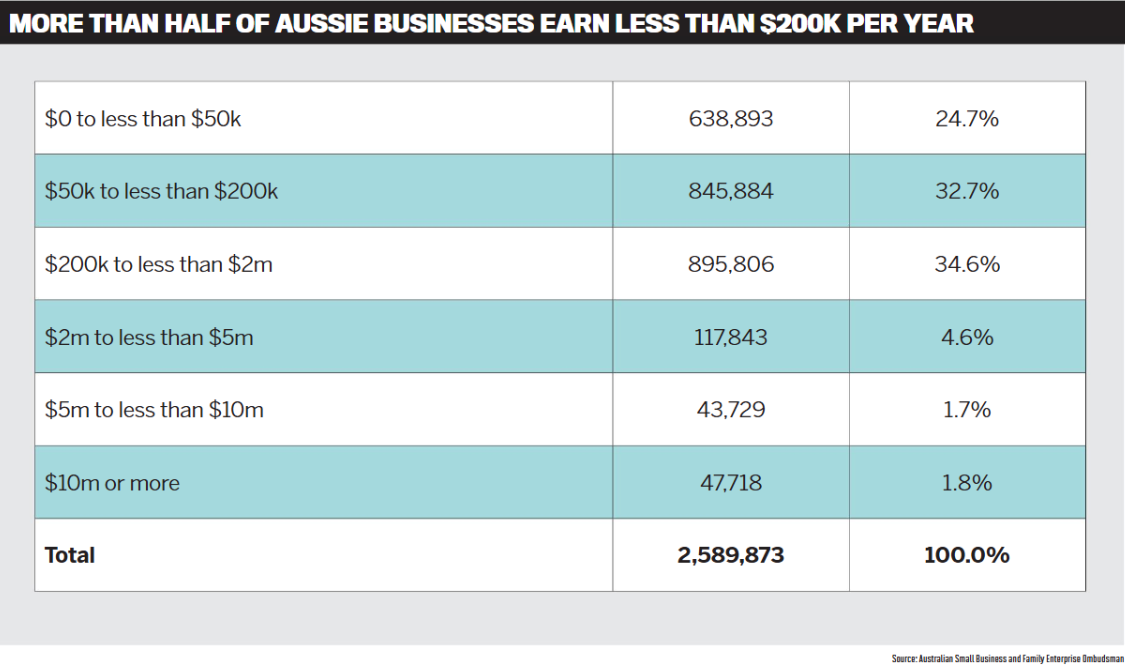

For a nation of over 2.5 million small businesses, Australia’s plumbers, decorators, bakers and retailers certainly get the short end of the stick when it comes to securing funding.

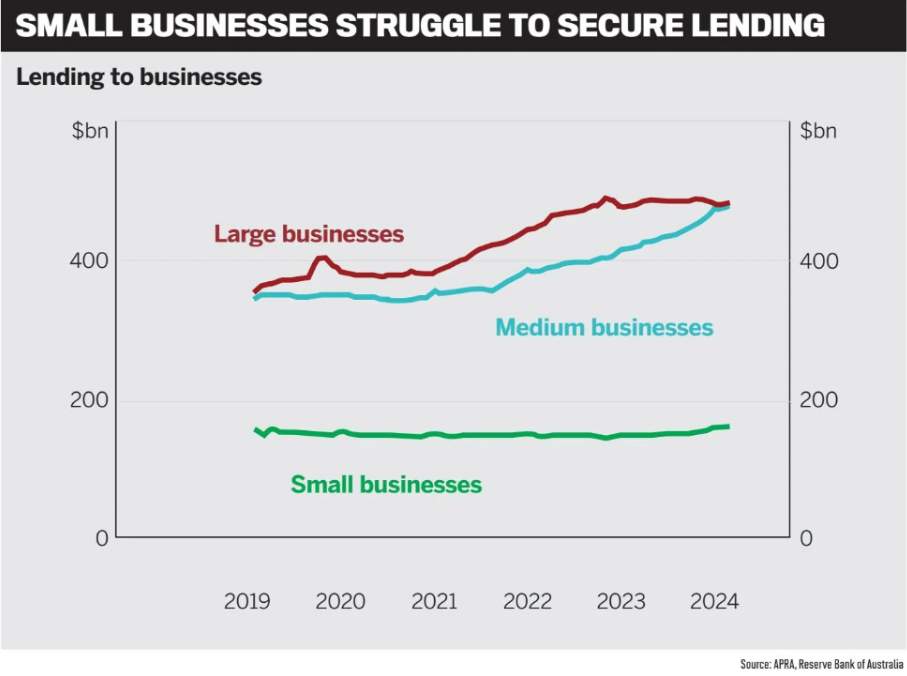

According to the Reserve Bank of Australia, lending to small businesses has been effectively flat since 2019, while larger businesses have seen their credit availability escalate.

Small business owners have expressed frustration with lenders’ increasingly strict lending criteria, which force them to either put their properties up as collateral or sell equity in their businesses.

To make matters worse for SMEs, the RBA’s latest Small Business Economic and Financial Conditions report found that soaring input costs have significantly impacted small businesses – especially in discretionary sectors such as hospitality.

“Access to finance is undeniably the most significant factor affecting SMEs today,” Paul Evans, Prospa’s national sales manager, told MPA.

“In particular, the ability to manage cash flow has never been more crucial in our current economic landscape. SMEs, as the backbone of our economy, play a vital role in how businesses choose to utilise their cash flow, largely influenced by the specific challenges they face in the market, many of which are exacerbated by soaring interest rates.”

And yet, despite the headwinds, small business insolvencies in 2025 remain thankfully below pre-COVID levels – a testament to the resilience that emerged as a recurring theme in discussions with lenders. For Evans, the resilience small businesses are showing in the current environment is nothing short of “remarkable”.

SMEs, by their nature, are also “nimble and adapt quickly to change,” said Matthew Heinnen, group manager at non-bank lender Liberty. “This intrinsic quality helps businesses create their own demand in any environment.”

Heinnen also told MPA that brokers continue to play a crucial role in helping small businesses “meet demand and fuel growth by providing access to a broad range of lenders and tailored funding.”

Evolving broker partnerships

Lenders have witnessed the broker-SME relationship become more collaborative than ever as diversification becomes more ingrained in the industry. According to Heinnen, this has resulted in an unprecedented level of knowledge of commercial finance among brokers.

“Each business is unique, so their cash flow solution should be too – that’s why professional advice is crucial,” he said. “Brokers now help small and medium businesses navigate the complex lending landscape and guide them in securing the financing that supports their growth goals.

“Liberty has long championed the broker distribution model, providing our broker partners with continuous education and support to ultimately help more businesses put their plans into action.”

Barry Saoud, general manager of mortgages and commercial at Pepper Money, is seeing brokers acting not just as intermediaries between borrower and lender but increasingly as strategic advisers to their clients. “This relationship has grown stronger, with brokers helping SMEs navigate complex financial landscapes and secure the best deals," he said.

Providing flexibility without this complexity is another quality SMEs place a lot of value on. As Saoud put it: “Small business owners want to spend their time running their business, not managing their finances.”

According to George Lyall, head of origination at Millbrook Group, brokers are also becoming more attuned to the progressive funding solutions available via the non-bank sector. “Consequently, more and more SME borrowers tend to be working with brokers to solve their financing needs,” he said.

Lyall placed a strong emphasis on educating brokers on how to properly structure a project and assess its feasibility. “It’s very important to understand all costs involved in the construction process and how they are to be funded,” he said. “This not only helps the broker but also the client throughout the construction process. This is something brokers should be looking at when placing construction loans, as these products are not set and forget.”

For Evans, brokers are essential in helping SME clients stabilise cash flow, adopt technology and protect emergency cash reserves. “With the proper guidance from brokers – backed by lenders – SMEs can transform uncertainty into opportunity, particularly with anticipated interest rate reductions. This preparation will help ensure they navigate challenges in 2025 and achieve long-term success.”

Evans added that product innovation is “a key component in how brokers deliver effective solutions for their customers efficiently.” In his view, the adoption of technology “is not just crucial, it's empowering, giving SMEs the tools they need to navigate the financial landscape.”

Non-banks to the fore

Despite global uncertainty and economic headwinds, the demand for SME finance is rising, with non-bank lenders increasingly becoming the go-to option for credit. But why?

“SMEs are turning to non-bank lenders because of their flexible and tailored lending solutions,” Heinnen said. “We recognise there is often more to a business’s story than what’s in their application. Liberty prides itself on spending time with brokers to better understand the unique circumstances of businesses and find solutions that meet their specific needs.”

Since no two businesses are the same, lending solutions often need to be out of the box and creative. In Heinnen’s view, the willingness among non-banks like Liberty to accept alternative types of income verification makes them ideal for delivering on these needs.

Saoud said that Pepper Money takes a business’s overall financial health into account, “rather than just the numbers on paper.” In his view, SMEs are increasingly turning to non-bank lenders like Pepper Money because of faster approval processes, more flexible terms and a better understanding of their unique needs. “Non-banks can often provide tailored solutions that traditional banks can't,” he said.

This gives Pepper Money the ability to offer higher loan-to-value ratios and bespoke loan terms; these are particularly helpful when SMEs are contending with ATO debts and other complex financial obligations.

“We work with SMEs to understand their situation and create solutions that give them the breathing room they need while positioning them for future growth,” Saoud said.

Simply put, non-banks are better placed to understand borrowers’ needs and therefore provide tailored solutions accordingly.

“Whether it's providing working capital, funding for business expansion, or helping businesses navigate cash flow and tax debt, our options are designed to be as dynamic as the businesses we serve,” Saoud said.

“We look at ways to deliver flexibility without the complexity. From workshopping scenarios through to application and credit lodgement, there is a process that can deliver fast outcomes for brokers and their SME clients. We are also backed by a credit team that always asks, ‘How can we help this client and get this done?’”

In Lyall’s experience, “we often hear of ‘bank risk’ borrowers seeking to avail finance from non-banks due to the inflexibility of the major banks and elongated time frames to process applications.”

Like his contemporaries, Lyall sees the demand for SME credit rising in the non-bank and private lending spaces as brokers continue to become more familiar with the products providers such as Millbrook have to offer.

While these benefits tend to come with a higher interest rate, “SMEs are happy to pay a slightly higher rate if they feel the lender is on the journey and wanting to work with them to succeed,” Lyall said.

The benefits of flexibility in the non-bank lending space are echoed by Evans. “What we are seeing at Prospa is an increase in your traditionally banking customers who are coming to Prospa seeking flexible, fast and innovative solutions to meet their ongoing business needs,” he said.

SMEs need solutions that are “fast, flexible and that work into the ecosystem of their businesses”, he said.

Like all credit providers worth their salt, non-banks also deploy teams of business development managers to keep businesses from drifting elsewhere.

“These relationships allow us to develop a deeper understanding of each business’s individual needs and therefore offer personalised solutions,” Heinnen said. “Our BDMs, credit teams and brokers will continue to work closely together to find ways for businesses to get a ‘yes’ and take the next step in their growth plans sooner.”

Lyall added that “relationships are imperative to keeping clients on board. A client’s journey of borrowing money and meeting future obligations can change over time. With the help of a skilled relationship manager, the journey can be enhanced for all parties, particularly with better knowledge of a borrower’s circumstances.”

Cases in point

Pepper Money recently approved a commercial real estate loan for a plumbing supply business owner seeking to purchase the warehouse he was renting.

His landlord offered him the opportunity to purchase the warehouse, with repayments expected to be less than his rent. Sam, the business owner, intended to buy the warehouse to store stock and run operations.

Although Sam’s business was performing well and he had a strong credit record, “traditional lenders would not accept an accountant's letter for income verification, which Sam needed due to his incomplete tax return,” Saoud said.

Pepper Money stepped in with an alternative solution, providing a near prime alt-doc loan on interest-only terms. The loan was approved at 70% LVR with a 30-year term.

The loan required income verification using a combination of a 24-month registered ABN, a 12-month registered GST, a declaration of financial position and either 12 months of business bank statements or 12 months of business activity statements.

Just like that, Sam was able to pursue his business goals.

At Millbrook, Lyall recounted the case of a recent funding facility written against a pub that had been closed for renovations. Since the pub had no trading history, the borrower was unable to go down the traditional banking route. Yet after two years with Millbrook, the client was able to refinance with a major bank. “This was rewarding as the client increased the trading and the value of the pub significantly. Also, it demonstrates the need for second-tier lenders,” Lyall said.

In another recent deal, Millbrook provided bridging finance for a borrower who owned an unencumbered asset and wanted to purchase the next-door property before selling his current property. Although the borrower was rejected by the banks, Millbrook provided a cost-effective solution within two weeks from application.

Read more: Specialised knowledge is an invaluable asset for brokers

At Prospa, Evans gave the example of a client who was seeking short-term capital to secure a new franchise licence. The client required the approval within hours, or they would have forfeited the opportunity.

“Working closely with the partner, our team of lending specialists and the customer, we were able to deliver a solution to ensure they could move forward with this new business opportunity,” Evans said. “The customer was so pleased he referred another customer to this partner.”

Going forward

“In the year ahead, we expect to see a greater focus on sustainability, as well as an increase in fintech solutions to streamline the lending process,” Heinnen said. Technology such as AI, meanwhile, “has the potential to reduce administrative tasks so we can reach financial solutions faster and easier.”

“At Liberty, our free-thinking approach to lending positions us well to embrace these trends, which we believe will create more opportunities for lenders, brokers and small to medium businesses,” Heinnen said.

Refinancing of tax debt is another trend Saoud is seeing more of in the SME space. “Brokers who understand these current economic conditions and are equipped to offer flexible, non-bank solutions will be best positioned to support their SME clients,” he said.

Read more: All eyes on prime in commercial property market

For Lyall, a few more rate cuts from the RBA will hopefully trigger an uptick in confidence, especially in the development space. He said he was also feeling a stronger sense of competition among lenders in the SME space, though he welcomes it, “as it provides many options for brokers and relationship managers when seeking finance.”

From Evans’ perspective: “Despite the ongoing challenges that businesses face, we continue to see demand rise. SMEs have navigated these challenges admirably and are now strategically investing in acquisitions. They are seizing opportunities to enter new customer markets and injecting capital to enhance their capabilities and operational efficiencies.”

As 2025 marches on, Evans expects to see more companies seeking both cash flow stability and growth opportunities.